When dual currency deposits became extremely popular during the 1990s, it was easy to find them at every single retail branch in Asia, with advertising boards offering a higher yield than traditional deposits

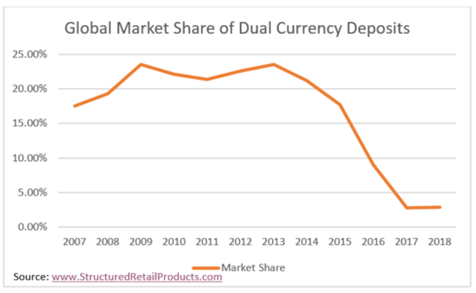

Nowadays, the story is completely different. Since 2013, the market share of dual currency deposits has fallen dramatically, from 23% to only 5% of the total volume sold in 2017, according to SRP data.

A dual currency deposit (DCD) is a deposit linked to a foreign-exchange rate, in which capital is returned at maturity after being converted into an alternative currency at a pre-defined rate. The returns are higher than plain fixed deposits, as clients receive the premium of an embedded option in the DCD. To simplify, the investor is guaranteed a higher coupon and, at maturity, will receive capital back in addition to a coupon, as long as the FX rate does not fall below a barrier level. If the FX rate is equal or below the barrier level, the investor will receive the capital and coupon in the other currency, making for a capital loss on the initial investment.

Investors tend to use DCDs for two reasons: to enhance return with a short-term product; or to hedge FX risk, as the other currency can be used to fulfil a specific debt or make a payment in that currency, pre-defining the worst-scenario FX rate.

The reality is that currencies are extremely volatile and their behaviour hard to predict. And, even if you are on the correct side of the play, a DCDs nature is such that you only need one currency to fail to perform in the desired way for all previous gains to be wiped out, leaving investors with a potential net loss.

According to an analysis of 14,256 products in the SRP database issued over the last 15 years, DCDs have offered an average annualised return of 8.44%. Nevertheless, the political events, such as Brexit, the trade war between US and the world and the interest rate movements globally led to, over the last two years, unexpected currency movements providing negative returns on many DCDs.

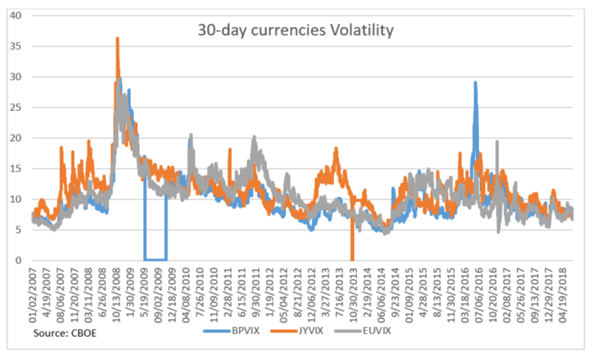

The other driving forces behind the decrease demand included the low volatility in the most popular currencies, such as the US dollar and Japanese yen, which has cut the premium received from out-of-the money options.

Although DCDs remain the most popular products in Mexico and Japan, the volume sold has reduced when compared with the increase in equity-linked products, such as autocallables and reverse convertibles, which raises the question of whether these products will ever recover their market share.

With the low implied volatility on FX rates, the premium these products can provide is not attractive, particularly when viewed alongside the downside risk of an intensified trade war between the US and the rest of the world.

While volatility has crept lower and lower over the last 11 years, and now stands at its lowest since summer 2014, the future for DCDs depends on an increase in short-term volatility or a potential sale of US Treasuries by China.