Only 60 very short-term products linked to Nvidia launched since November 2024 have breached their defensive barriers as a result of yesterday’s historic crash.

The 17% price drop of the Nvidia stock on Monday which sent shockwaves through the market has had a limited impact in the structured products space as only a small portion of products have seen their protection barriers breached.

The company broke the record for the biggest one-day loss in value for a public company on the US stock market on Monday 27 January. Nvidia's share price fall equated to a huge US$593 billion loss in value.

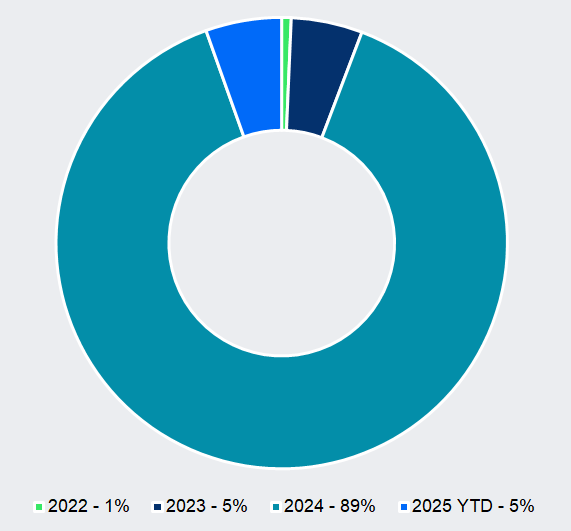

According to SRP, there are 2,958 live products (worth US$8.7 billion) linked to the Nvidia stock which feature a knock-in put and downside defensive barriers. Of those, one percent struck in 2022 with most strike dates concentrated in 2024 (89%).

Structured products linked to Nvidia by strike date

Source: SRP

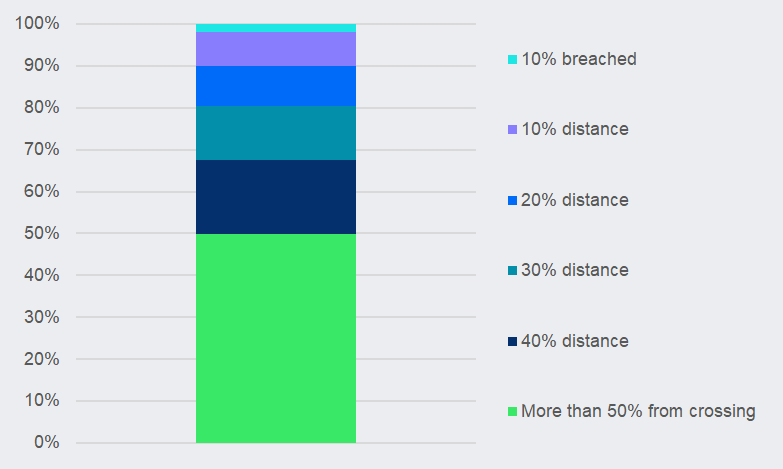

Despite the sudden fall of Nvidia’s value, SRP data shows that structured products have benefitted from their defensive features to absorb the impact as only 59 products linked solely to the Nvidia stock - 1.3% of the total - have breached their barriers since Monday (27 January) by 10% or more and 0.6% have breached their barrier by less than 10%.

In addition, there are 236 products – or 7.9% of the total products solely linked to Nvidia – within a 10% distance of breaching their barriers; 287 products (9.7% of the total) are within a 20% distance from breaching the barrier; and 381 products (12.8% of the total) are within a 30% distance of breaching their barriers.

The remaining 1,995 products, which represent 67% of the products linked to Nvidia, are 40% away or more from breaching their barriers.

Structured products linked to Nvidia - distance to barrier

Source: SRP

Testing the new SRP Greeks tool, there has been an increase in the Vega sensitivity of short put options as a result of the Nvidia price drop, and the increased implied volatility. Since for capital at risk products the majority Vega is negative – vol up, price down – the Vega value has gone further into negative territory from -2 to -4.5.

The reason for this movement is that capital-at-risk products, such as autocallables and barrier reverse convertibles have short options (e.g., short puts) which means that investors in these products are selling volatility.

The issuer hedges these options by shorting volatility so when volatility increases, the price of the product decreases, leading to negative Vega. As volatility rises, the risk of adverse price movements increases, therefore the short options become riskier, and with a larger negative Vega effect.

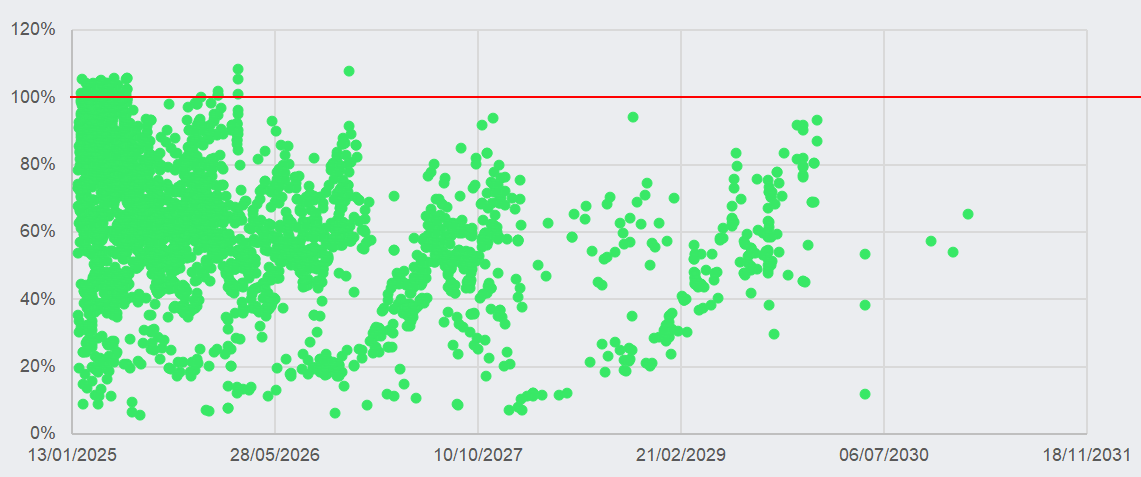

The graphic below shows the current barrier levels for individual products and maturities for knock-in products as of 28 January 2025 - the average knock-in barrier at 71.9% is below the close of the Nvidia price as of yesterday 28 January 2025.

Structured products linked to Nvidia - distance from barrier (>=100 means barrier has been breached)*

*Measured from Nvidia close price on 28 January 2025.

Source: SRP

Live products linked to Nvidia feature mostly autocallable structures, as well as reverse convertibles and barrier reverse convertibles. The knock-in defensive barriers, which normally would force investors to participate 1:1 in the fall of the underlying if they are breached during the product term or at maturity, ranges from -85% to -15% of the initial level with a -61.4% average, SRP data shows.

Switzerland (1,074 products) has the higher number of live products linked to the Nvidia stock which were sold mostly via autocall and reverse convertible structures, followed by the US market (959 products) and Hong Kong (421 products).

The most active providers of Nvidia-linked products include UBS (460 products), HSBC (424 products), Unicredit (293 products), J.P. Morgan (289 products) and Julius Baer (273 products).

Discover the power of SRP Greeks and see how our latest data solution enhances trading strategies and risk management with key Greeks calculations - Request a demo today