The US indexed annuity sales are again in record territory. Allianz, AuguStar, Lincoln blossom while Security Benefit and Symetra are in the shadow by sales.

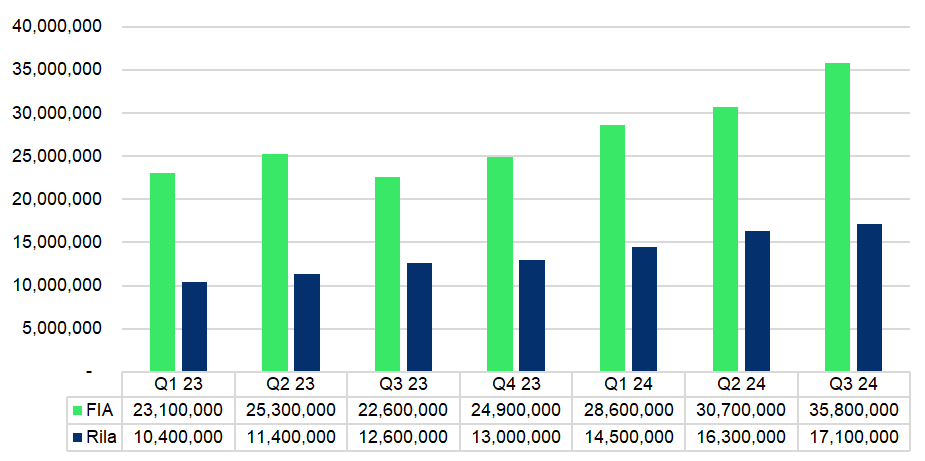

Fixed index annuity (FIA) sales have continued to rally by closing the third quarter at yet another record high at US$35.8 billion, a 16.6% climb quarter-on-quarter (QoQ) or a 58.4% surge year-on-year (YoY), according to the latest US Individual Annuity Sales Survey Limra released yesterday (25 November).

The volume leaves this market segment at US$95.1 billion in the first nine months of the year, up 33.9% YoY.

‘Strong equity market performance and a desire for principal protection continue to attract investor interest in FIA products,’ said Bryan Hodgens, senior vice president and head of research at Limra. ‘To remain competitive, carriers are refining their indices and introducing more lucrative crediting options.’

US total individual FIA, Rila sales (US$000)

Source: Limra US Individual Annuities Sales Survey

Meanwhile, registered index-linked annuities (Rilas) have retained their momentum with US$17.1 billion sales in Q3 2024 despite it displaying a slower pace.

The volume represents a five percent rise from the previous quarter, or a 35.7% leap YoY.

As a result, Rila sales increased nearly 40% to US$47.9 billion in the first nine months compared to the prior-year period, the survey shows.

Limra expects Rila sales to ‘remain strong’ through 2025.

The strong sales activities for both FIAs and Rilas, which together posted US$52.9 billion in Q3 2024, have propelled the continued expansion in the US annuity market which also houses fixed rate deferred annuity, income annuity and traditional variable annuity.

The whole market posted US$114.7 billion in Q3 2024, 30% higher YoY, and US$332 billion in the first nine months, up 23% YoY.

Carrier breakdown

In the FIA space, Allianz Life of North America, led by CEO and president Jasmine Jirele (pictured), has sticked out a mile with its more-than-doubled quarterly sales, which comes to US$5.3 billion, commanding almost 15% market share as a dominant issuer.

That compares to US$2.3 billion in Q3 2023, US$2.4 billion in Q1 2024 and US$2.3 billion in Q2 2024 for the subsidiary of Germany’s Allianz SE.

Most recently the insurance carrier introduced the Allianz Accumulation Advantage+ and the Allianz Accumulation Advantage 7 FIAs in March.

Meanwhile, Athene Annuity & Life, which took over Allianz as the largest FIA issuer in the first half of the year, saw its sales decline 3.1% to US$3.3 billion in Q3 2024 from the previous quarter.

The volume puts Athene in the third place after Sammons Financial, which increased its sales by 17.9% to US$3.5 billion QoQ.

US individual FIA sales by carrier (US$000)

|

Company |

Q2 24 |

Q3 24 |

Change |

|

Athene Annuity & Life |

3,420,743 |

3,315,776 |

-3.1% |

|

Sammons Financial Companies |

2,969,922 |

3,500,179 |

17.9% |

|

Allianz Life of North America |

2,335,443 |

5,250,201 |

124.8% |

|

Corebridge Financial |

2,314,874 |

2,333,847 |

0.8% |

|

Nationwide |

1,804,900 |

1,672,300 |

-7.3% |

|

American Equity Investment Life |

2,018,934 |

1,791,318 |

-11.3% |

|

Fidelity & Guaranty Life |

1,644,569 |

1,688,820 |

2.7% |

|

Global Atlantic Financial Group |

1,594,655 |

1,988,639 |

24.7% |

|

Massachusetts Mutual Life |

1,335,438 |

1,453,799 |

8.9% |

|

AuguStar |

542,328 |

1,156,081 |

113.2% |

|

Security Benefit Life |

1,132,031 |

572,911 |

-49.4% |

|

Prudential |

691,173 |

1,025,055 |

48.3% |

|

Pacific Life |

945,566 |

345,470 |

-63.5% |

|

Lincoln Financial Group |

527,214 |

1,355,554 |

157.1% |

|

EquiTrust Life |

746,400 |

814,531 |

9.1% |

|

Aspida |

625,793 |

552,993 |

-11.6% |

|

Delaware Life |

467,541 |

463,233 |

-0.9% |

|

National Life Group |

645,695 |

1,026,726 |

59.0% |

|

Symetra Financial |

630,708 |

513,449 |

-18.6% |

|

Bankers Life & Casualty |

383,353 |

394,501 |

2.9% |

|

Top 20 |

26,777,280 |

31,215,383 |

16.6% |

|

Total industry |

30,700,000 |

35,800,000 |

16.6% |

|

Top 20 share |

87% |

87% |

Source: Limra US Individual Annuities Sales Survey

Other carriers that have enjoyed a boost in the quarterly sales are Lincoln Financial and AuguStar.

Lincoln Financial returned to the top 10 league table with US$1.4 billion in Q3 2024 after lagging behind last year, which represented a 1.6x QoQ growth. This comes after the Pennsylvania-based insurer rolled out dual trigger feature for its FIAs in March.

At the same time, AuguStar lifted its sales by 1.1x to US$1.2 billion QoQ, forming two thirds of its combined FIA sales for the first nine months. The Cincinnati-based company last month started to offer BNP Paribas’ Night Owl Index via its OrionShield FIAs on an exclusive basis.

In addition, the Limra report also shows several insurance carriers that have seen their FIAs sales falling most in Q3 2024 compared to the previous quarter including Pacific Life (-63.5%, US$345.5m), Security Benefit Life (-49.4%, US$572.9m) and Symetra Financial (-18.6%, US$513.4m).

In the Rila segment, Equitable continues to take a safe lead with US$3.6 billion sales in Q3 2024, which is up 4.7% QoQ, making up over 20% of the total.

Allianz and Brighthouse Financial were neck-to-neck after the latter raised its Rila sales by 11.0% to US$2.3 billion in Q3 24.

Along with its FIA expansion, Lincoln Financial has capitalised on its activity in the Rila market with US$1.3 billion sales in the three months, a 36.3% increase QoQ.

US individual Rila sales by carrier (US$000)

|

Company |

Q2 24 |

Q3 24 |

Change |

|

Equitable Financial |

3,464,332 |

3,627,798 |

4.7% |

|

Allianz Life of North America |

2,354,572 |

2,316,378 |

-1.6% |

|

Brighthouse Financial |

2,027,221 |

2,250,080 |

11.0% |

|

Prudential |

2,232,949 |

1,897,389 |

-15.0% |

|

Jackson National Life |

1,256,403 |

1,392,089 |

10.8% |

|

RiverSource Life Insurance |

1,134,448 |

952,945 |

-16.0% |

|

Lincoln Financial Group |

974,617 |

1,327,922 |

36.3% |

|

New York Life |

754,610 |

641,867 |

-14.9% |

|

Nationwide |

281,600 |

339,000 |

20.4% |

|

Athene Annuity & Life Assurance Co |

277,495 |

254,700 |

-8.2% |

|

TruStage |

264,300 |

426,134 |

61.2% |

|

Transamerica |

311,900 |

239,032 |

-23.4% |

|

Massachusetts Mutual Life |

201,084 |

348,457 |

73.3% |

|

Symetra Financial |

252,573 |

187,795 |

-25.6% |

|

Principal Financial Group |

206,870 |

456,586 |

120.7% |

|

Global Atlantic Financial Group |

161,226 |

211,571 |

31.2% |

|

Sammons Financial Companies |

76,576 |

118,179 |

54.3% |

|

Fidelity & Guaranty Life |

1,892 |

31,330 |

1555.9% |

|

Guardian Life of America |

18,788 |

4,058 |

-78.4% |

|

Top 20 |

16,253,457 |

17,023,309 |

4.7% |

|

Total industry |

16,300,000 |

17,100,000 |

4.9% |

Source: Limra US Individual Annuities Sales Survey

Principal Financial Group also forged ahead with US$456.6m Rila booked, 1.2x from the previous quarter.

Fidelity & Guaranty Life is another rising star as its Rila sales jumped to US$31.3m from US$1.9m despite remaining as one of the smallest issuers.

Meanwhile, top fallers for Rilas in the quarter include Guardian Life of America (-78.4%, US$4.1m), Symetra Financial (-25.6%, US$187.8m), Transamerica (-23.4%, US$239.0m), RiverSource Life (-16.0%, US$952.9m), Prudential (-15%, US$1.9 billion) and New York Life (-14.9%, US$641.9m).

Symetra Financial in June added buffer and dual trigger crediting options to its flagship Rila, Trek Plus, as SRP reported.

Do you have a confidential story, tip, or comment you’d like to share? Write to Summer.Wang@derivia.com