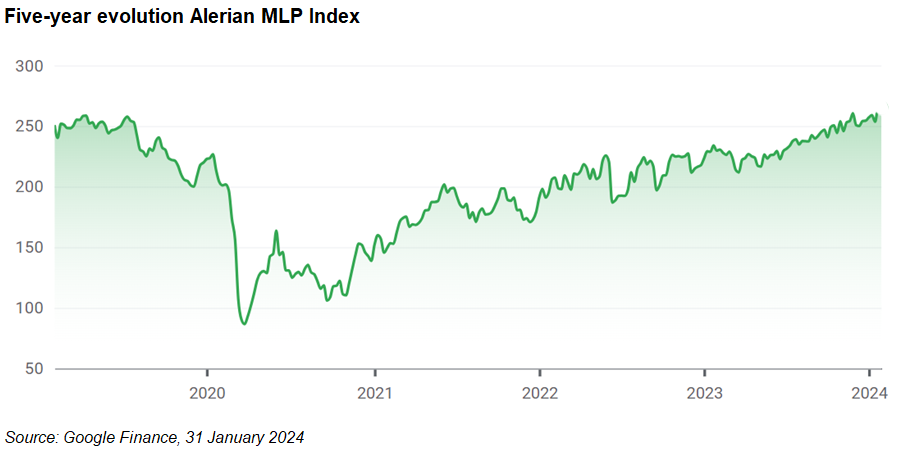

J.P. Morgan Asset Management has added an exchange traded note (ETN) to its catalogue of tracker notes aimed at investors seeking exposure to master limited partnerships (MLPs).

The asset management arm of the US investment bank has listed on the NYSE Arca the Alerian MLP Index ETN (AMJB), which matures in 2044. The new note tracks the Alerian MLP Index (AMZ), a capped, float-adjusted, cap-weighted index that serves as the leading measure of energy infrastructure MLPs.

The index measures the composite performance of energy-oriented MLPs that earn most of their cash flows from qualified activities involving energy commodities using a capped, float-adjusted, capitalization-weighted methodology.

MLPs are limited partnerships primarily engaged in the exploration, marketing, mining, processing, production, refining, storage, or transportation of any mineral or natural resource.

The index has been developed by VettaFi, as index sponsor, and is maintained and calculated by VettaFi, as index calculation agent. The Index is reported on a real-time basis under the Bloomberg ticker AMZ.

The AMJB ETN is the successor to the J.P. Morgan Alerian MLP Index ETN (AMJ), which also tracks AMZ and matures in May 2024.

Leonteq launches digital offering for insurance companies, onboards CNP Luxembourg

Leonteq has expanded its digital offering to insurance companies for the lifecycle management of investment products. CNP Luxembourg is the first insurance company to use LynQs to monitor the performance of its structured products.

With our new offering for life-insurance companies, monitoring structured products invested in by unit-linked life insurance policies becomes much more efficient - Alessandro Ricci, Leonteq

The Swiss structured products specialist provider is targeting insurance companies seeking to monitor their structured products portfolio across all issuers and keep track of related events via the LynQs dashboard which provides a broad overview of product information, including pricing, distance from the barrier and coupon payments.

‘LynQs aims to simplify the daily life of its users. With our new offering for life-insurance companies, monitoring structured products invested in by unit-linked life insurance policies becomes much more efficient,’ said Alessandro Ricci (right), head investment solutions at Leonteq.

Leonteq said the platform’s user interface can be customised in a white-labelled format and that it intends to launch additional features that will support the digitalisation of the unit-linked product segment in a second phase.

The onboarding of CNP Luxembourg follows the launch of Leonteq’s white-labelling partnership with Banque International à Luxembourg.

Hang Seng expands ESG index range with a focus on A-share market

Hang Seng Indexes Company (HSIL) has launched four new ESG Indexes focused on the A-share market, as it seeks to expand its suite of ESG indexes targeted at investors interested in sustainable investing.

With a focus on the A-share market, the new ESG index series is based on the existing Hang Seng Stock Connect China A 300 index (‘HSCA300’) which measures the overall performance of the 300 largest A-share companies eligible for Northbound trading under the Stock Connect schemes.

Anita Mo (right), chief executive officer at Hang Seng Indexes Company, said: ‘With the rising importance of sustainability, more institutional investors believe ESG factors play an integral role in identifying investment opportunities.’

The new indexes include the Hang Seng Stock Connect China A 300 ESG Index (HSCAESG); Hang Seng Stock Connect China A 300 ESG Enhanced Index (HSCAESE); Hang Seng Stock Connect China A ESG Leaders Index (HSCAESL); and Hang Seng Stock Connect China A ESG 50 Index (HSCAE50).

The new HSCAESG and HSCAESE aim to combine the existing HSCA300 with ESG initiatives while the other two new indexes, HSCAESL and HSCAE50, reflect the performance of the top 50 ESG leaders among the constituents of the HSCA300.

The new ESG index series encompasses various ESG screening and integration strategies, supported by ESG data provided by international and local ESG data providers, to accommodate investors’ diverse sustainable investing needs.

The launch of the new ESG index series brings the number of HSIL’s ESG-themed indexes to 29.

AI for Alpha rolls out tactical investment tool

Ai for Alpha, a fintech company specialized in machine learning technology for investment strategies, proudly announces the launch of its Flagships Decoding strategy.

By tactically selecting assets with the highest potential for rewards and minimizing exposure to high-risk assets, we aim to consistently outperform traditional benchmarks - Beatrice Guez, Ai for Alpha

This new strategy offers a portfolio solution aimed at portfolio managers using Ai for Alpha technology and offers access to a diversified and cost-efficient portfolio, powered by Ai for Alpha's decoding technology.

‘We are revolutionising the way investment strategies are replicated, using our proprietary machine learning technology,’ said Beatrice Guez (right), CEO of Ai for Alpha.

‘Our approach goes beyond conventional replication, enhancing the decoding of leading investment strategies. By tactically selecting assets with the highest potential for rewards and minimizing exposure to high-risk assets, we aim to consistently outperform traditional benchmarks.’

The Flagships Decoding strategy is a composite of four strategies including a 60% Enhanced Decoding of Leading USD Wealth Managers; a 20% Enhanced Decoding of Global Hedge Funds; a 10% Enhanced Risk Parity Decoding: By tracking top-tier Risk Parity strategies; and a 10% CTA Decoding Strategy.

‘Our replication portfolios have a proven track record of outperforming their benchmarks,’ Guez added.

Isda paper unveils trends in OTC equity derivatives

The International Swaps and Derivatives Association (Isda) has published a paper looking into over the counter (OTC) equity derivatives (EQDs) including a comprehensive examination of their benefits and diverse use cases.

The paper analyses the market landscape looking at fluctuations in size across geographies, product offerings and notional outstanding maturities.

The paper shows that over 2023 diverse market participants, including institutional investors, asset managers and hedge funds, leveraged OTC EQDs for a number of purposes, from hedging to market access and portfolio diversification. According to the Isda paper, ‘the customisation potential and flexibility of OTC EQDs make them particularly appealing for investment hedges’.

The OTC EQD market has retained a stable size over the past 15 years with fluctuations within the US$6.3 trillion to US$7.6 trillion range - despite this stability, OTC EQDs constitute a relatively modest fraction, representing between one and two percent of the broader OTC derivatives market.

The OTC EQD market encompasses a range of instruments, including swaps, forwards, options, contracts for difference, and other products with the growth coming from equity forwards and swaps in comparison to OTC equity options.

Geographically, the publication reveals a significant shift in the dominance of the OTC EQD market, with the United States now emerging as the central region for total notional outstanding at the expense of European countries. The paper also highlights the prevalence of short maturities in OTC EQDs, with 63% of notional outstanding having a remaining maturity of one year or less.

Click the link to read the Isda paper Overview of OTC Equity Derivatives Markets: Use Cases and Recent Developments.

Image: Metamorworks/Adobe Stock.