“Need for Speed” – Sometimes too good can be true

The original risk control mechanism was developed in Europe over two decades ago. In its simplest form, it is an overlay on a risky asset (such as a benchmark index) which, when the volatility goes over a pre-determined volatility level (or risk target), this triggers a de-allocation from the risky asset in favor of a “safer” asset – most commonly cash – to stabilize the index.

Intraday risk control indices are much more responsive to market movements than their traditional counterparts, therefore making the indices significantly more reactive to any changes in volatility

This stabilization feature helped risk control indices gain popularity around the world, particularly in annuities and structured products, as they buffer returns and help avoid drawdowns. Crucially, they provide cheaper and more consistent option pricing, which made them appealing in the era of low interest rates after the Great Financial Crisis.

The original risk control mechanism is still in use today. It typically measures the volatility of an index once per day, using closing levels of the index observed over one or more look-back periods, usually of one-three months. Using this volatility measurement, the reallocation between assets is made with a lag of one or even two days. A bank trading the index in a structured product therefore has plenty of time to reallocate its hedges.

However, there is a new kid on the block: intraday risk control, made possible by advanced trading systems that not only enable traders to measure volatility throughout the day, but also facilitate hedging transactions multiple times during a single trading day.

By applying this new mechanism, intraday risk control indices are much more responsive to market movements than their traditional counterparts, therefore making the indices significantly more reactive to any changes in volatility. Think of intraday risk control as like having a high-powered car with responsive ABS brakes that make your driving safer compared to a conventional car.

You may ask: can more frequent changes really make an index more stable and perform better? Is this too good to be true? We recently conducted a review of intraday risk control indices to find out.

The Index Standard monitors and rates new indices and in 2021 we saw a few new indices using the intraday risk control mechanism and this gathered pace in 2022 and 2023. Today, specialist IP firms, indexing companies and investment banks offer several variations on risk control indices.

Index developers have different techniques to implement intraday risk control. Some indices measure volatility during the day and reallocate at the end of the day, while others not only measure volatility but may also reallocate multiple times during the day. The frequency at which the underlying index is observed during the day also varies between indices. For simplicity in the interest of our review, we classified all these techniques as intraday.

We compared the live performance of intraday risk control indices with that of traditional risk control indices which measured volatility over longer periods. We used the return/risk ratio to determine index performance in the most recent 12 months. We decided against a longer period as the results would include backtests and we were more interested in live performance. The higher the return/risk ratio, the better the index performance.

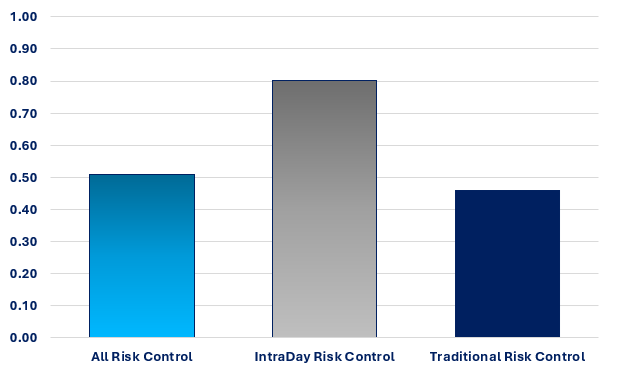

Our analysis shows that intraday risk control indices have an average return/risk ratio of 0.8, versus 0.46 for traditional risk control indices, indicating that the intraday risk control mechanism is more effective.

Average one-year return/risk ratio of intraday risk control indices vs traditional risk control indices

Source: The Index Standard, 2024. Past performance is not indicative of future performance.

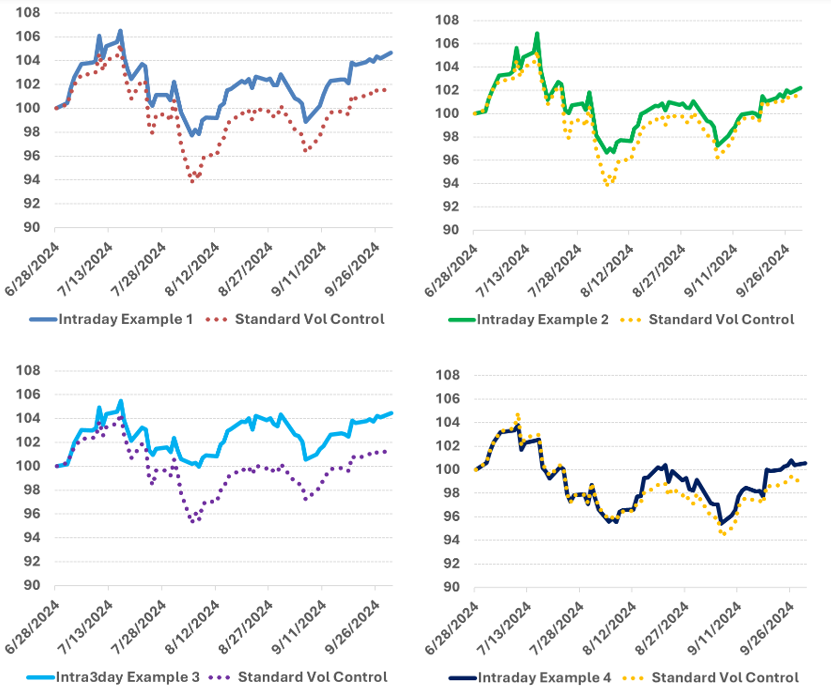

To further determine if the intraday mechanism is effective, the recent market gyrations between July and September 2024 provided an ideal opportunity to put it under a microscope in a real-life stress test.

In the four graphs below, we show the live performance of both intraday and traditional risk control indices based on the same benchmark and the same risk control level from July to September 2024. In each graph, you can see that the more reactive intraday mechanism is more effective in avoiding drawdowns than the traditional risk control mechanism.

Examples of intraday indices in action (Intraday is in bold and traditional is dashed)

Source: The Index Standard, 2024. Past performance is not indicative of future performance.

While we think more research is warranted, our initial conclusion is that the intraday mechanism is more responsive than traditional risk control methods. Under live stressed market dislocations, having an intraday mechanism seems to protect an index from volatility swings and provide better buffers.

Diversification and stability are both prized features in annuities and structured products, and users of these products should appreciate the added benefit the responsive intraday risk control approach.

Image: Supatman/Adobe Stock.

Do you have a confidential story, tip or comment you’d like to share? Contact Us | SRP (structuredretailproducts.com)