The US bank has significantly decreased its US issuance in Q1 23 - revenues dropped mainly due to a slowdown in its global banking & markets activity.

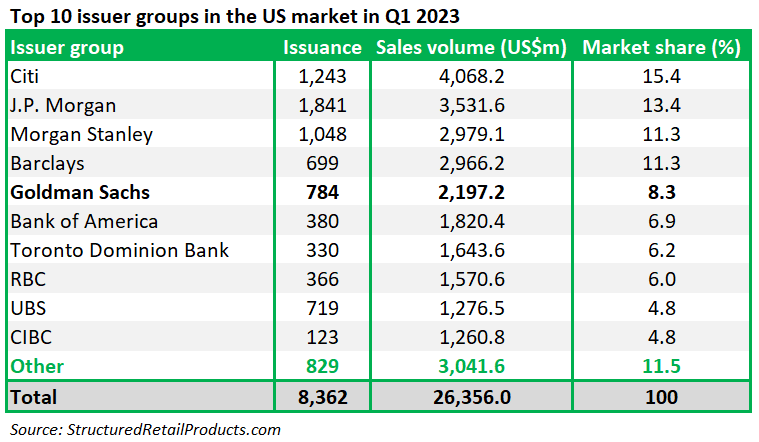

Goldman Sachs has conceded the crown to Citigroup in the US issuer league table for the retail market in Q1 23. The bank has slipped in fifth place after J.P. Morgan, Morgan Stanley and Barclays by issuance, SRP data shows.

During the quarter, the US bank cut its issuance amount by 56.9% to US$2.2 billion across 784 structured notes - its market share shrank to 8.4% from 17.9%.

New issuance was driven by stocks or equity indices but also by hybrid assets, interest rates and exchange-traded funds (ETFs) and commodities including 58, 27, 23 and two products, respectively.

There were 15 ETFs used as the underlying of 27 products led by VanEck Vectors Gold Miners ETF (US$7.8m), Technology Select Sector SPDR ETF (US$3.5m) and iShares Silver Trust (US$4.4m).

In listed structured product market, the bank launched 36,455 leverage wrapped certificate products in Germany and Austria as well as 129 derivative warrants and 114 callable bull/bear contracts (CBBCs) in Hong Kong SAR in Q1 23.

In Taiwan, there were 50 structured notes launched by the US bank in Q1 23, an increase from 35 products compared with the prior-year period.

The bank's issuance in France dropped to 41 from 55 at the same time. The bank’s issuance in France included a product tracking a mutual fund - Trimestriel Europe Février 2023 - which featured a 12-year tenor with DS Investment Solutions acting as the distributor. The reference asset is the Federal Optimal Select DV EUR.

Earnings

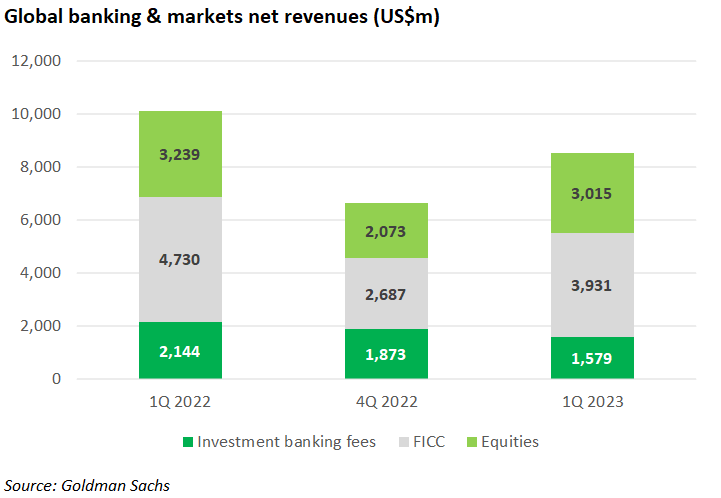

Global banking & markets (GBM) posted a net revenue decline of 16% to US$8.4 billion in Q1 23 year-on-year (YoY) - equities net revenues dropped seven percent to US$3.02 billion YoY.

Specifically, equities intermediation contributed to 57.7%, or US$1.7 billion, which was down 20% from the prior-year period, reflecting 'significantly lower net revenues across both derivatives and cash products,' according to GS' Q1 23 earnings results.

Equity financing accounted for the remaining, or US$1.3 billion, primarily reflecting increased spreads.

Earlier this month, Goldman announced several changes to the senior management team in its equity trading division following the retirement of Joe Montesano, head of equity trading for the Americas. Dimitrios Nikolakopoulos has been named as global head of equity structured products.

The bank also reported a drop in FICC intermediation net revenues by 20% to US$3.3 billion YoY, which was driven by 'lower net revenues in currencies and commodities, partially offset by significantly higher net revenues in interest rate products and higher net revenues in mortgages and credit products'.

FICC financing was three percent higher at US$651m compared with Q1 22 – as a result, the unit posted net revenues of US$3.9 billion, down 17% YoY.

Investment banking fees fell 26% to US$1.6 billion as advisory, equity underwriting and debt underwriting net revenues were down 27%, eight percent and 32%, respectively.

'Advisory reflected a significant decline in industry-wide completed mergers and acquisitions transactions,' stated the bank. 'Debt underwriting reflected a decline in industry-wide volumes'.

On a quarterly basis, investment banking fees dropped 16% while equities and FICC net revenues advanced 46% and 45%, respectively.

For asset & wealth management (AWM), net revenues were up 24% at US$3.2 billion YoY led by debt investments, translating to a 10% decline QoQ.

'Equity investments reflected mark-to-market net gains from investments in public equities compared with significant mark-to-market net losses in 1Q22, partially offset by significantly lower net gains from investments in private equities,' stated the results.

Operating expenses were six percent lower at US$3.2 billion, leading to pre-tax earnings of US$613m.

In addition, the third division - Platform Solutions - posted net revenues of US$564m, which were up 110% YoY, or up 10% QoQ, driven by consumer platforms.

'We are operating from a position of strength and remain focused on executing our strategy to further grow our leading GBM and AWM franchises,' said David Solomon (pictured).

Groupwide, net revenues fell five percent to US$12.2 billion while operating expenses climbed nine percent to US$8.4 billion YoY. Net earnings dropped 18% to US$3.2 billion YoY.

The bank’s assets under supervision (AuS) increased 11.6% to a 'record' US$2.7 trillion from a year ago. By asset class, fixed income, liquidity products, equity and alternative investments accounted for 39%, 29%, 22% and 10%, respectively.

In terms of client channel, third party distribution, institutions and wealth management made up of 37%, 35% and 28%, respectively. By region, approximately 71% of the AuS came from Americas, followed by Emea (22%) and Asia (seven percent).