The UK bank has reported net profit of US$3.9 billion in Q2 21 ended in June, up 21.9% year-on-year (YoY).

Revenue dropped four percent to US$12.6 billion mainly due to ‘lower revenue in markets and securities services (MSS) and the impact of lower interest rates’.

On an interim basis, the revenue decreased by four percent to US$25.6 billion, leading to a net profit of US$8.4 billion, up 58.5% YoY, according to the bank’s latest results.

At the end of June, HSBC, which is led by group chief executive Noel Quinn (pictured), had derivative assets of US$209.5 billion and derivative liabilities of US$200.2 billion, down 31.9% and 33.9% from six months ago, respectively.

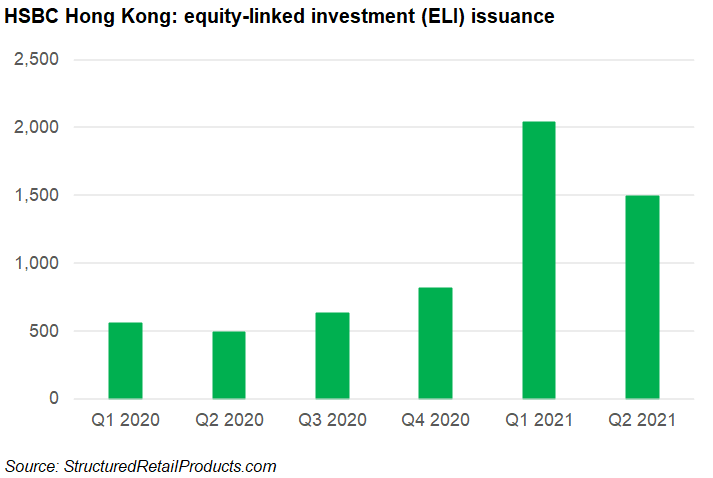

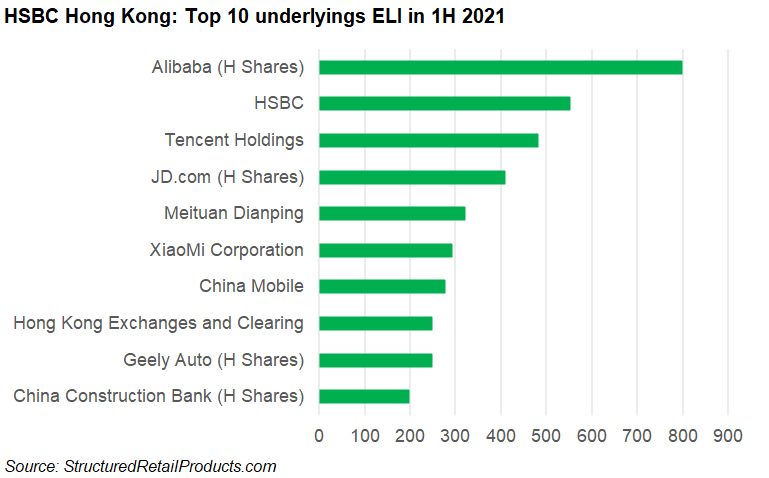

From January to June, the UK bank marketed 22,917 structured products worldwide, SRP data shows. Other than the 17,803 flow notes in Germany, Hong Kong SAR has become the largest retail hub featuring equity-linked investments, structured warrants and callable bull/bear certificates.

In the US, HSBC saw its issuance decreasing to 435 in H1 21 from 578 a year ago, but the sales volume remained stable at US$1.65 billion. The most popular underlyings in this period were the S&P 500, Russel 2000, DJIA Index, Nasdaq 100 and Eurostoxx 50.

Wealth and Personal Banking (WPB)

The largest segment by revenue saw its pre-tax profit doubling to US$2 billion in Q2 21 YoY, though its revenue fell four percent to US$5.7 billion driven by lower interest rates and lower markets treasury revenue.

Despite the fall in revenues the bank saw a 26% hike of Asia wealth revenue in the quarter, which was attributed to the benefit of US$359m of insurance market impacts and the acceleration of ‘pinnacle’ initiative in China.

As the UK bank pivots its core focus to the Asian market, wealth balances in the region grew 18% to US$810 billion in H1 21 led by client assets and funds under management YoY. The region represented 46% of the total wealth balances, followed by Europe at 30% - lower than the 32% in H1 20.

By division, the total wealth management balance of US$1.7 trillion in Q2 21 comprised premier and Jade deposits (28.1%), retail wealth balance (27.4%), global private banking client assets (25.5%) and asset management third-party distribution (19%).

The bank also reported a 13% drop in WPB net fees, which is part of non-net interest income, to US$1.4 billion in Q2 21 quarter-on-quarter (QoQ) as equities performance in Q1 21 was stronger leading to higher wealth sales.

During the first half of 2021, the wealth management business increased its headcount with 600 full-time employees as part of its five-year expansion plan, while the number of high-net-worth clients increased seven percent to 1.7m YoY.

Global Banking and Markets (GBM)

The second largest segment by revenues took the hardest hit in Q2 21 - down 23% at US$3.6 billion YoY. Its pre-tax income fell 19% to US$1.4 billion as the non-net interest income decreased 26% to US$2.5 billion ‘primarily in markets from reduced volatility and client activity’ compared with Q2 20.

On an interim basis, GBM recorded a revenue of US$7.9 billion in H1 21, down 8.1% YoY. Around 55.7% of the revenue was generated by the MSS where its decrease ‘more than offset favorable movements in credit and funding valuation adjustments of US$0.4bn and a strong performance in structured derivatives in equities, reflecting strong client activity in wealth, particularly in Asia’.

The MSS unit appointed Thibaut de Rocquigny (right) as global head of equity structuring based in Hong Kong SAR after Marc Lemmel left the bank early this year.

As of 30 June 2021, GBM had structured notes liabilities designated at fair value of US$7.2 billion, up 36.5% from 2020-end.

By underlying asset class, equity accounted for US$6.1 billion with a volatility between 5% and 124% while FX brought US$634m with volatility of between 3% and 36%. Also based on option model, the equity correlation ranged from 7% to 98%.

In addition, the third pillar by revenue, Commercial Banking, posted a pre-tax profit of US$1.6 billion in Q2 21, a rebound from a loss of US$600m YoY, as its revenue declined four percent to US$3.3 billion ‘reflecting the impact of lower interest rate environment in global liquidity and cash management (GLCM) and other products’.

Click the links to view the Q2 21 presentation and interim report.