HSBC is the latest international bank to blame Covid-19 and global economic uncertainty for the large-scale drops in its latest results.

The UK-headquartered bank reported that its first half of 2020 performance was impacted by the ‘Covid-19 pandemic, falling interest rates, increased geopolitical risk and heightened levels of market volatility’.

As such, profit after tax down was down over two-thirds (69%) on the first half of 2019, to $3.1 billion because of higher expected credit losses and other credit impairment charges (‘ECL’) and lower revenue, primarily outside of its Asia business – similar to what other banks have reported in recent weeks. It expects total provisions against loan losses between $8 billion and $13 billion in 2020, a wider range that expected in previously announced quarterly earnings.

Revenues were down nine percent to $26.7 billion, reflecting the impact of interest rate reductions, as well as adverse market impacts in life insurance manufacturing and adverse valuation adjustments.

Its common equity tier 1 ratio at 30 June 2020 was 15%, up from 14.7% at 31 December 2019. This increase included the impact of the cancellation of 4Q19 dividend and the current suspension of dividends on ordinary shares. These increases were offset by an increase in risk-weighted assets.

Figures in its newly-formed Wealth and Private Banking business were also down on the back of a decline in revenue from the fall in global equity prices and lower interest rates. Adjusted profit before tax of $1.7bn in 1H20 was 65% lower than in 1H19. Retail banking revenue was also lower (-13%), at $11.3 billion, though was mitigated by deposit balance growth in Hong Kong and the UK particularly. In Wealth Management, revenue of $3.6 billion was down $0.9 billion or 20%.

For its Global Banking and Markets business, increased adjusted revenue of $4.2 billion more than offset the impact of falling interest rates and adverse movements in credit and funding valuation adjustments. Some 50% of the bank’s revenue was generated in Asia Pacific. In Global Markets, revenue grew 38%, as client activity increased due to higher volatility levels supporting an improved FICC performance across foreign exchange, rates and credit though this was offset by lower equities revenue. Global Banking revenue increased by 3% from higher capital markets revenue. Adjusted profit before tax of $2.5bn was $0.2bn lower than in the first six of months of 2019.

HSBC has a share of just under 10% of the distribution market with 3,266 products issues in the first half of 2020, worth just under $25 billion, making it the second most active globally behind Hang Seng Bank.

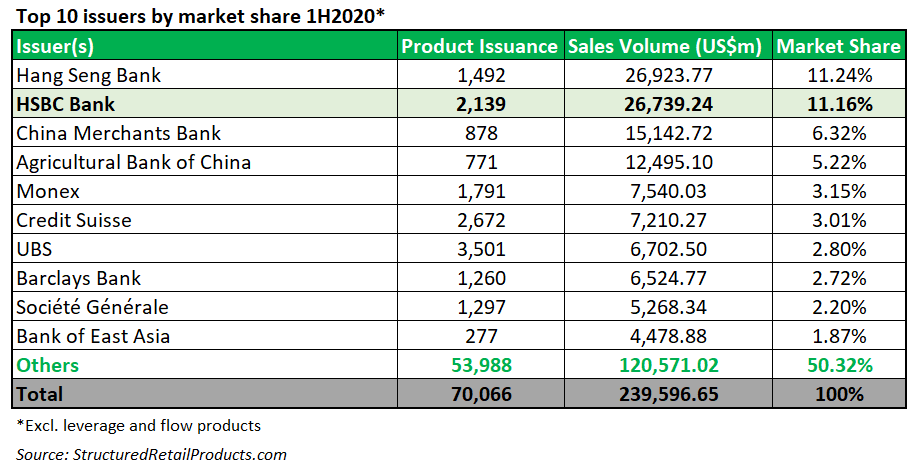

It was the second most active issuer globally (after Hang Seng Bank) during the first half of the year, with an 11.16% share of the market, spread out over 2,139 products worth just under $27 billion.

It has boosted its position compared to the first six months of 2019, when it issued 1,646 products globally, for a total sales volume of $19.7 billion. Its market share then was around half of what it had been in the year to 30 June 2020, at 5.1%.

The bank typically chooses market capitalisation indices as underlyings for its products, with the S&P 500 and the Eurostoxx 50 being the most popular. Product choices also reflect this, with typical products being equity single index/single share choices.

Click the link to read the HSBC results, presentation and interim report.