A white paper released by UK distributor Tempo Structured Products is seeking to challenge advisors’ reluctance to adopt structured products for their clients.

Today, and with apologies for adding yet another acronym to the SRP lexicon, we are talking about ABC – Alpha by Contract – a TLA[i] that Chris Taylor, global head of structured products at UK provider Tempo Structured Products is hoping will stick.

Taylor (pictured) hopes, in fact, that this cornerstone of his recent white paper, ‘Structured products: USPs, evidence, need and cognitive biases’ will prove so convincing an intervention in the active versus passive management debate that it will be a catalyst, helping change professional adviser views about structured products, "slowly but surely, encouraging them to ensure that they at least consider them as portfolio options within the investment universe, as evidence-based advisers surely should'.

The active/passive debate is probably the single biggest, longest-running conversation in the investment universe - Chris Taylor, Tempo Structured Products

Those advisers who have, “metaphorically or literally pressed unsubscribe on the sector,” are the main audience for Taylor’s paper, which is part of a campaign challenging them to rethink an attitude that has often not kept pace with the transformation of the structured products industry.

The paper showcases return statistics and highlights the merits of including structured products in a diversified portfolio. It explains structured products and banking industry improvements since the financial crash, and busts persistent myths about negative events structured products were caught up in (but were not of their making and where structured product holders did not suffer) like the Keydata collapse.

The paper also tackles myths – around complexity, dividends, and fees – that can be better explained by psychological biases than by the facts.

Shining new light

These arguments are well rehearsed in our industry. The reframing of structured products in language familiar to advisers, however, is new.

“The active/passive debate is probably the single biggest, longest-running conversation in the investment universe, which will no doubt continue to run and rage forever. However, structured products are not part of the conversation – and we would suggest that this is, in part, because the structured products sector isn't talking the right language,” Taylor explains.

He continues: “Wealth managers and professional advisers are discussing 'alpha' and 'beta'… Meanwhile, the structured products sector is talking about zero coupon bonds and equity derivatives.”

Taylor believes this linguistic mismatch prevents structured product providers from splitting open a binary discussion about the advantages and shortcomings of passive versus active management to insert the contractually delivered payoffs – the unique and contractually binding relationship to the underlying asset, and resulting diversification – structured products can offer.

This is necessary, to return to that binary discussion, because future sources of alpha are difficult to reliably identify, and, in a closely related point, are rarely consistently replicable over the long term, according to Taylor.

Active manager alpha is also generally expensive to access (a particular concern in a low returns environment) and often of limited (a few percentage points) ambition. The traditional alternative, beta, is also a concern in the low returns environment many commentators expect to prevail over the short to medium (and possibly even longer) term.

Enter ‘Alpha by Contract’

The term does not imply that all structured products outperform all of the time. (1) It is a concept of two parts, an assertion that structured products can and do deliver alpha (more on which below), and that they do so based on the legal, contractual obligation on issuers to honour a particular defined payout, with “risk/return profiles that neither active nor passive funds offer or deliver” and without dependence on fund management processes and skill.

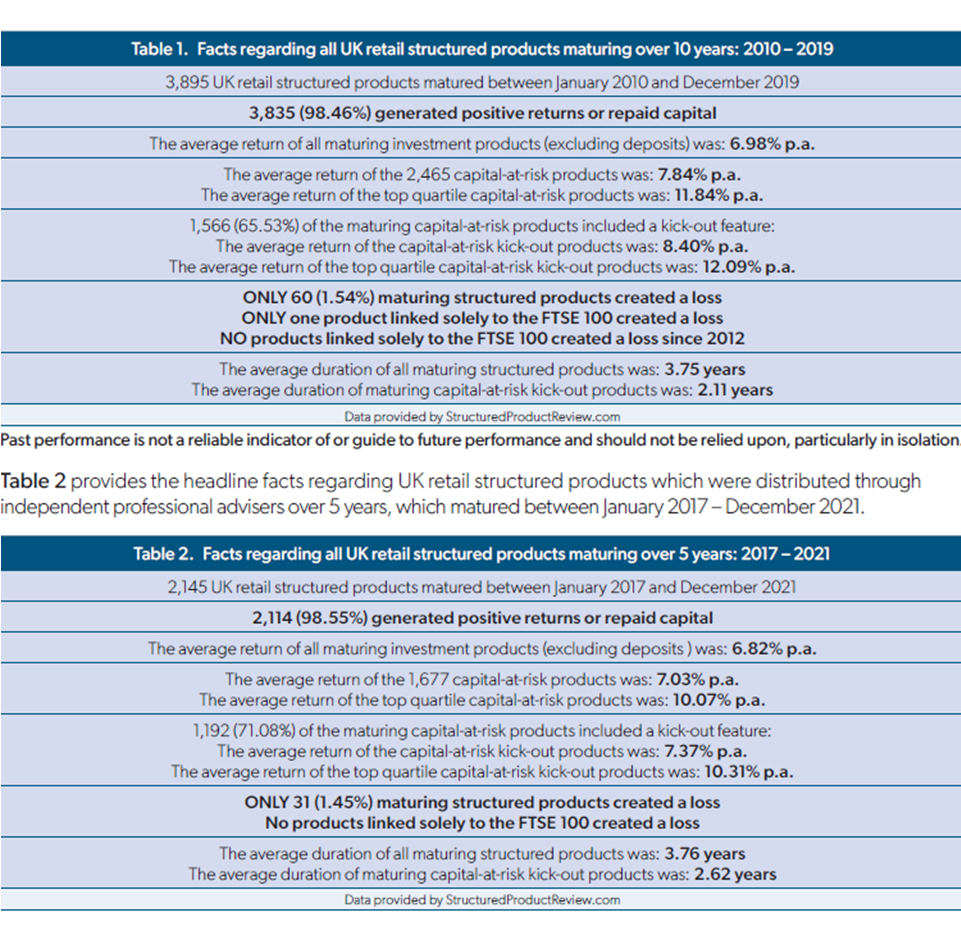

To reinforce the first half of the concept, the paper highlights the performance of around 5,000 UK IFA-distributed structured products launched and matured over the last 20 years or so, which Taylor says evidences structured products’ USPs and, “shines a light on the potential merits of including structured products in diversified portfolios.”

The data, from Structured Products Review, shows the vast majority (98.46%) of the 3,895 UK retail structured products maturing between January 2010 and December 2019 either generated positive returns or repaid capital. The average return of all maturing investment products (excluding deposits) was 6.98% pa. Only 1.54% of maturing structured products created a loss, and only one single product linked only to the FTSE 100 created a loss. A similar picture pertains for the 2,145 UK retail structured products maturing between January 2017 and December 2021.

To emphasise the point about Alpha by Contract, the paper also details the performance and risk/return profile of the first ten of Tempo's plan maturities. All ten are defensive kickout products, and all ten delivered Alpha by Contract compared with relevant price return indices (including their linked index), and with typical FTSE 100 gross dividends re-invested trackers.

“The analysis also highlights why structured products can arguably be viewed as presenting better risk/return profiles than comparable active and passive mutual funds,” Taylor says.

The paper also focuses on portfolio construction and diversification which could be facing a few challenging years ahead. “The case for structured products does not hinge only on a long-term, low-returns investment environment,” says Taylor. But he believes it could be difficult for professional advisers to identify investment options that can “reasonably be considered more likely to generate viable levels of positive returns for investors, in the region of 6-12% pa, in low return, no return and moderately falling market environments, than structured products.”

To back up the arguments in the paper, Tempo Structured Products hopes to arrange an academic study on structured products and Alpha by Contract. Given the UK market’s current emphasis on single payout kickout products, it would be useful to see excess returns analysed by payoff profile over time and in relation to underlying market changes, and to demonstrate their effect on a broader portfolio. Tempo also plans an analysis of long-term equity performance, which Taylor expects to reveal persistent periods of low returns.

‘Alpha by Contract’ continues the theme SRP has explored several times this year: how the changing nature of financial advice provision mitigates against structured products for many advisers, and the right way to attract them back to an improved industry. Is new terminology a good place to start?

Can it be enough to overcome the structural challenges of an advisory business increasingly focused on managed portfolios and fund-based products?

As ever, your own thoughts are most welcome.

Tempo Structured Products is offering ‘Live’ video webinars for professional advisers on 22 February and 26 April 2023. ‘Structured Products: USPs; Evidence; Need; & Cognitive biases!’ is a CPD-accredited white paper with three hours CPD awarded on test completion.