In the second part of our analysis, we compare the performance of structured products matured in France between October 2020 and October 2021 with other popular passive index-based strategies held over the same period.

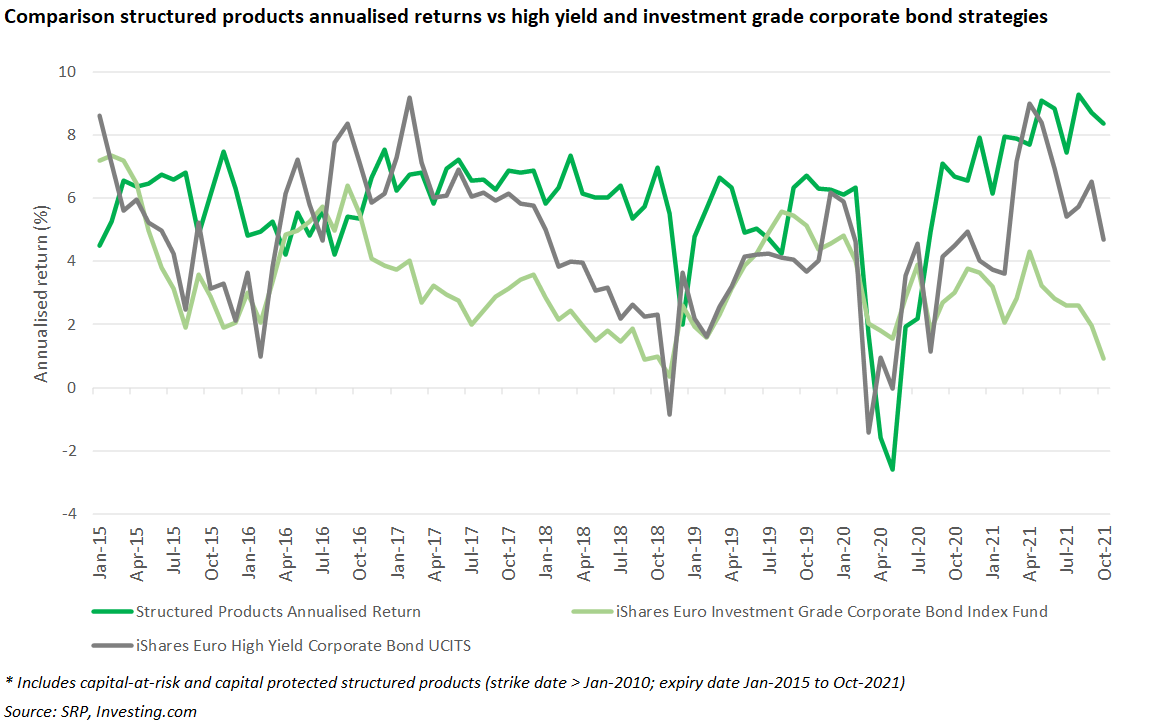

The analysis compares the average annualised returns of structured products over a period of six years with an investment in fixed-income - two bond exchange-traded funds (ETFs), one investment grade, one high yield - and an investment in the equity market via ETFs which represent direct equity holdings. All the ETFs reinvest dividends.

The recovery in 2021 has come with some inflationary pressure and since the summer, we saw a change in the inflation dynamics - Nikolay Nikolov

“For each of the two funds, we calculated the return for the investor (based on the price of the ETF) if these ETFs were held over the same period as structured products. This allowed us to benchmark the annualised return of every structured product to the simulated performance of the ETFs point-to-point” said Nikolay Nikolov, product manager at Euromoney Derivatives.

As the chart shows, over the past six years structured products have delivered more stable and broadly higher returns compared to an investment in a fixed income ETF with the same duration.

In March 2020, the market crash slashed returns across all asset classes which had a direct impact on autocall structures as the lower market position meant that many potential maturities were deferred until later observation dates. Since Q4 2020, however, structured products maturing in France outperformed consistently and by far the iShares Euro Investment Grade Corporate Bond Index Fund and the iShares Euro High Yield Corporate Bonds Ucits until the end of the period observed.

The market rally of 2021, particularly in the second half of the year, triggered the early maturity features of many autocall products which expired with a higher gain that they would have realised in 2020.

In the second half of 2020, corporate bonds valuations soared from their lows due to central bank purchases especially in the high yield segment - as a result of the monetary stimulus yields plummeted and pushed up bond prices.

“The recovery in 2021 has come with some inflationary pressure and since the summer, we saw a change in the inflation dynamics,” said Nikolov. “For fixed income investors, the primary concern regarding rising inflation is the potential for interest rates to rise. And of course, rising interest rates, or when the market anticipates an increase in interest rate has put pressure on fixed-income investments.”

As the chart shows, this resulted in the fall of prices of existing bonds since the summer as the credit market anticipated tighter monetary policy from central banks.

In contrast structured products maturing in France during the period observed delivered steadily rising annualised returns. In August, structured products maturities recovered their pre-Covid level of six to seven percent annualised, and in the following months the average yield continued to increase to reach 8.3% in 2021.

“These returns were realised in the context of an impressive equity markets rally over the period and were supported by a massive wave of products autocalling as well as by bullish products that were structured to tap into the market recovery,” said Nikolov.

Versus equity ETFs

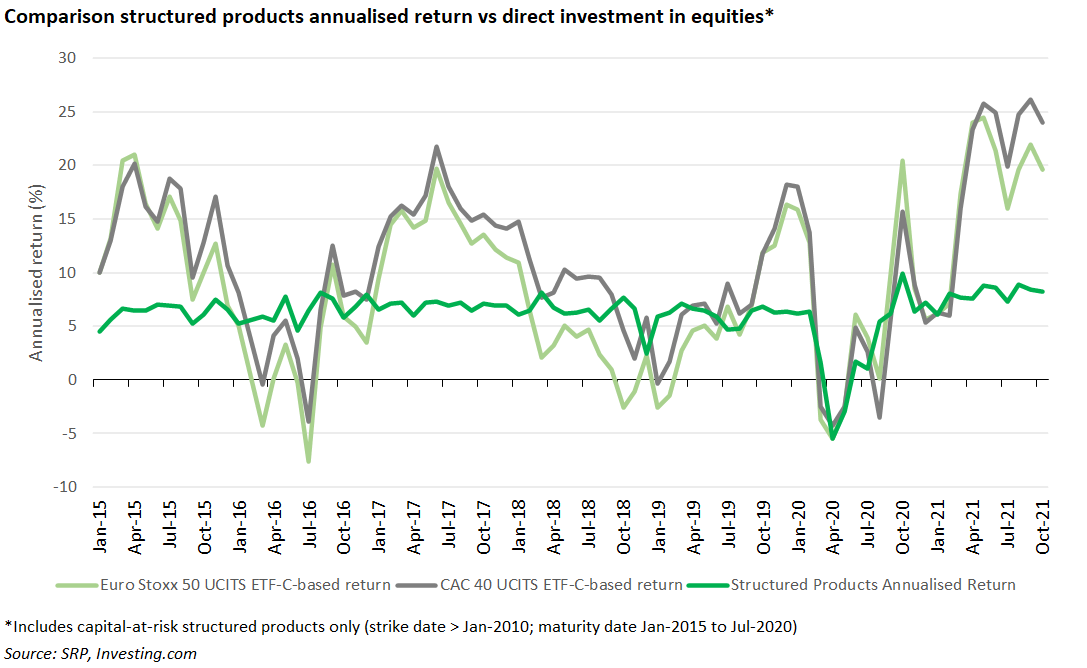

The comparison of the performance between structured products and a direct investment in equities looks at the annualised returns of structured products matured in France over the last six years versus the performance of a Cac 40-linked ETF and a Eurostoxx 50-linked ETF – both ETFs are considered with reinvested dividends.

As with the previous comparison, each of the two ETFs was benchmarked point-to-point to every structured product over their full investment term, going from the strike date to maturity.

As the chart shows, structured products have delivered very stable returns over the past six years. In April and May last year, the return plummeted in parallel with the stock market correction. The fall in returns was exacerbated by a number of risky single-stock-linked structures that weighed the average return.

“However, during this period there was no maturing product linked to an index that breached the conditional protection over the period,” said Nikolov.

Since the lows of 2020, structured products returned to and beyond their pre-crash levels, with monthly annualised return of between 6 and 9%.

“In 2021, structured products could not match the performance of direct equity investments, but this is because generally structured products do not aim to outperform the equity market but rather to moderate investors’ exposure to market fluctuations," Nikolov added.

As the chart shows, during the market fluctuations at end of 2015, beginning of 2016, end of 2018 and beginning 2019 and 2020, structured products minimised the losses which would have been more acute for investors in equity ETFs.

“Structured products have effectively delivered regular yield in many different market conditions,” said Nikolov. “The ability to adapt and deliver in virtually any market context is possibly the ultimate added-value of structured products.”

All in all, several structured products have also been able to capture bullish trends with a number of structures paying out two-digit annualised coupons of up to 40% to 60%.

In conclusion, structured products have delivered stable returns over the past six years with yields of between 6 and 9% in 2021 and have generated higher returns than fixed income passive strategies during the same period.

The comparison with direct equity investments must be done in the context of structured products being designed to offer a controlled exposure to the equity market.

“Structured products don’t offer the full upside, but they have proven their value as an extremely flexible tool to generate performance in all market conditions,” concludes Nikolov.

Other findings

Structures products maturing in 2021 had different structures from those maturing in any of the previous five years - different underlyings – more optimised/bespoke indices, more single stocks and Worst of Option structures, as well as more bullish autocalls, and autocalls with bonus coupons.

Increase in the number of defensive structures which will allow early redemption even in falling markets, because of high valuations in the equity market.

Introduction of new structures which focus on paying a coupon in falling markets rather than prioritising the early redemption.

Delayed early redemptions set to take place in two or three years since the strike - no longer after the standard one year, and autocall conditions set to be triggered even in falling markets (-10, -15%) after the third anniversary of the product, for instance.

Blending regular income and memory coupon structures to remunerate investors regularly in falling markets and enable them to capitalise on the long-term holding if the underlying is stable over time, with a larger memory coupon.

Click the link to access the France Structured Products Performance report 2020-2021.

SRP is the leading source of data intelligence on structured products globally, enabling you to plan for the future, gain market insights and compete strategically. Contact us to try a free a demo.