UK investors in structured products have been hit by the market volatility triggered by the Covid pandemic and financial turmoil of 2020.

Structured products maturing in 2020 have delivered probably one of the worst performances and returns since the aftermath of the financial crash of 2008/9, according to a report by Lowes Financial Management (LFM).

The Structured Products Annual Performance Review 2021 released by the UK financial adviser shows that market turmoil resulted in 16 among 235 structured product maturities in 2020 realising a capital loss. This represents six percent of all maturing products in the UK, and compares to four loss-making maturities among 334 maturities in 2019.

Almost 70% of all products maturing last year generated positive returns for investors

“The UK stock market has been in turmoil throughout the year and few investments have been immune to the dramatic turbulence,” Lowes managing director Ian Lowes (pictured), said. “2020 still represented another successful year for retail structured products. Almost 70% of all products maturing last year generated positive returns for investors.”

Average annualised returns for all products maturing in 2020, including structured deposits were 3.52% against 5.73% in 2019 and 6.37% in 2018.

Sector annualised returns may have dropped on recent years and against the 6.27% average of the last decade (Jan 2010 – Dec 2019) but they remained inflation-beating. While there were some products that resulted in a capital loss, this still represented less than seven percent of the overall market.

All the products maturing at a loss were inherently riskier share or commodities linked plans, many of which were already forecast to make losses even before the pandemic struck, according to Lowes.

Despite the loss of capital incurred by some of the products maturing in 2020, there were 11 plans that matured realising an annual return greater than 10%. More than half the rest beat inflation after delivering an average annualised return of more than four percent.

"Given that autocalls are now the dominant product shape and given that the coupons snowball, the market correction has simply served to defer many maturities until a later date when they have a significant potential to outperform markets that simply recover – provided the markets do recover before the final maturity date," Lowes told SRP. "With the maximum durations of many autocalls being extended beyond the traditional five and six years, there is hopefully plenty of time for recovery, for most plans."

SRP data also shows that over 200 products with maturity dates in 2021 have already expired including 128 products linked to single indices worth an estimated US$1.4 billion; 91 linked to baskets of indices worth US$690m; and seven linked to baskets of shares worth an estimated US$48.7m.

Of those 212 products are linked to the FTSE100, 66 linked to the Eurostoxx50 and 31 linked to the S&P500.

Best and worst performers

Half of all the products maturing in 2020 were linked solely to the FTSE 100 Index. Structured deposit and capital protected structures returned an average annualised return of 1.82% over an average duration of 5.35 years and the capital at risk plans returned an average of 5.68% over an average duration of 4.24 years.

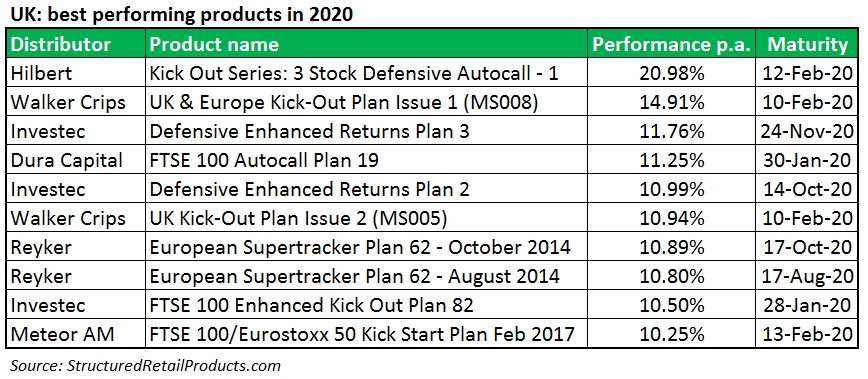

According to the LFM performance analysis high-risk plans delivered the best and worst performance. The Hilbert Investment Solutions Kick Out Series: 3 Stock Defensive Autocall Issue 1, which matured returning investors’ original capital in addition to a gain of more than 10% (20.98% pa according to SRP data) after just six months.

This growth structure combining a knockout, reverse convertible, worst of option payoff types was hedged by Citi and offered exposure to a basket of shares (Barclays, Aviva, Vodafone).

The worst performing plan was Meteor’s Crude Oil Kick Out Supertracker Plan March 2015. This plan matured at the end of five years with an annual capital loss of 74.89%, making an annualised loss of 24.12%.

This product hedged by Morgan Stanley was linked to the S&P GSCI Oil ER index and had a knockout, capped call payoff profile.

Click in the link to read a copy of the LFM Annual Performance Review.