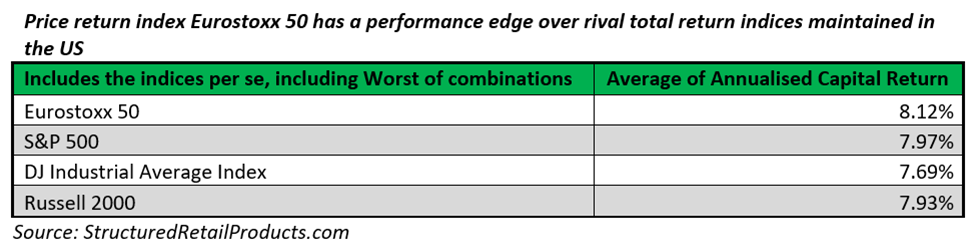

The Eurostoxx 50 index constructed as a price return index offers a higher dividend yield than US total return indices at the expense of lower upside participation rates embedded in structured products.

In this analysis, we shift the focus towards the three most featured indices as underlyings of US structured products – the S&P 500, DJ Industrial Average Index and Russell 2000. Since the three indices analysed are total return indices, we compare their income potential to a price return index, the Eurostoxx 50, where dividends are distributed rather than reinvested.

The S&P 500 is the best 2020 proposition with a five-year growth of dividends per share amounting to 133.47% upwards, whilst the DJ Industrial Average Index dividends grew more frugally - 101.18%.

On the other hand, a small fraction of the S&P 500 earnings per share represented reinvested dividends (only 1.41%), while Russell 2000 dividends account for 74.09% of its earnings. Moreover, the Russell 2000’s dividend yield set at 1.58% was considerably higher than the DJ Industrial Average Index (0.14%) and the S&P 500 (0.09%).

Overall, the Russell 2000 was the most income oriented underlying in the trio although the S&P 500 has the highest growth potential to exponentially increase its income.

With a dividend yield of 6.08%, the Eurostoxx 50 income is superior to the dividend yield of the Russell 2000, S&P 500 and DJ Industrial Average Index. In accordance with what we have already argued, value oriented underlyings characterised by lower P/B ratios convey a higher dividend yield.

Hence, the Eurostoxx 50 and Russell 2000 P/B ratios (1.50 and 1.86) compensate with higher dividend yields, whereas the S&P 500 and DJ Industrial Average tend to fall slightly more into the overvalued territory. The latter’s dividend yields are inferior to the preceding two indices.

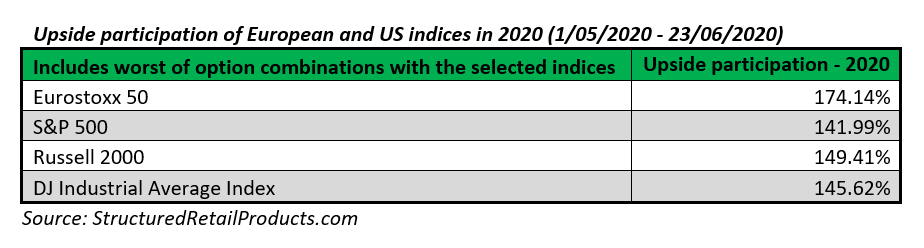

The consensus among structured product theorists and practitioners is that price return indices underlying structured products sustain higher participation rates not only because their dividends are not reinvested but also because the call option constructing products linked to total return indices tends to be more expensive. We can illustrate this by comparing the Eurostoxx 50 (price index) versus three US total return indices.

We find that structured products linked to the Eutostoxx 50 have ensured on average a 174.14% upside participation, while the participation rate of products linked to the S&P 500, Russell 2000, and DJ Industrial Average Index show an average of 141.99%, 149.41%, and 145.62% upward potential, respectively.

Yet, despite their higher participation rate, products linked to price return indices generally fail to outperform products linked to total return indices as the closing price of the total return index upon maturity will reflect the final dividends reinvested and will be higher than the price return index reading by a margin equal to these dividends.

Overall, the lower the dividend yield, the better the price return index will perform, and vice versa.

SRP data shows that products linked solely to the Eurostoxx 50 outperform the US index trio (considered on their own), which indicates that dividend yields of the US total return indices have not been sufficient to justify the total return structure of the indices over their European benchmark rival.

In scenarios when the dividend yield is higher and the index growth rate is lower than the respective inputs built in the structured product pricing model, total return indices will gratify investors with greater returns. However, if dividends yield are lower than estimates and index growth surpasses estimates, price return indices outperform their total return counterparts.

Income focus

An ideal timing to invest in income structured products is when markets go sideways as blue-chip companies still offer hefty dividends but are ensued by dividend cuts (as it happened in the aftermath of the coronavirus pandemic outbreak).

Effectively purchasing an income product is tantamount to selling puts – in this case, the investor hopes that the price of the underlying will go upwards, whereas investors in products buying options may have granted the right to sell the underlying and hope that prices tumble. If a structured product is purchased when dividends are high on its pricing date, but the company is coerced to curb its dividends, then we can expect that stock prices may rise – as dividends deduct from the stock closing price on their corresponding ex-dates.

Meanwhile, income structured products offer either a guaranteed fixed coupon or provide some buffer which absorbs moderate losses. If the underlying price increases, the probability of breaching the coupon barrier is further minimised.

This is why the number of reverse convertibles structures increased during the period 1 May – 23 June 2020 as slashing dividends to sustain solvency emerged at least in some companies’ agendas. SRP data shows that the sales volume of products with a reverse convertible payoff (or merged with other payoff types) have skyrocketed by 142.34% since the end of the first quarter of 2020.