SRP research analyst Filip Dyankov performed a Monte Carlo simulation of the top 10 most sold structured products, and the top 10 products with the highest sales volume maturing in the US market during May and June to predict prospective capital returns and annualised performances.

By multiplying the squared logarithmic changes by 252 (a rough estimate of workdays in a calendar year) we get an annualised variance, which is subject to a square root, to compute the annualised standard deviation.

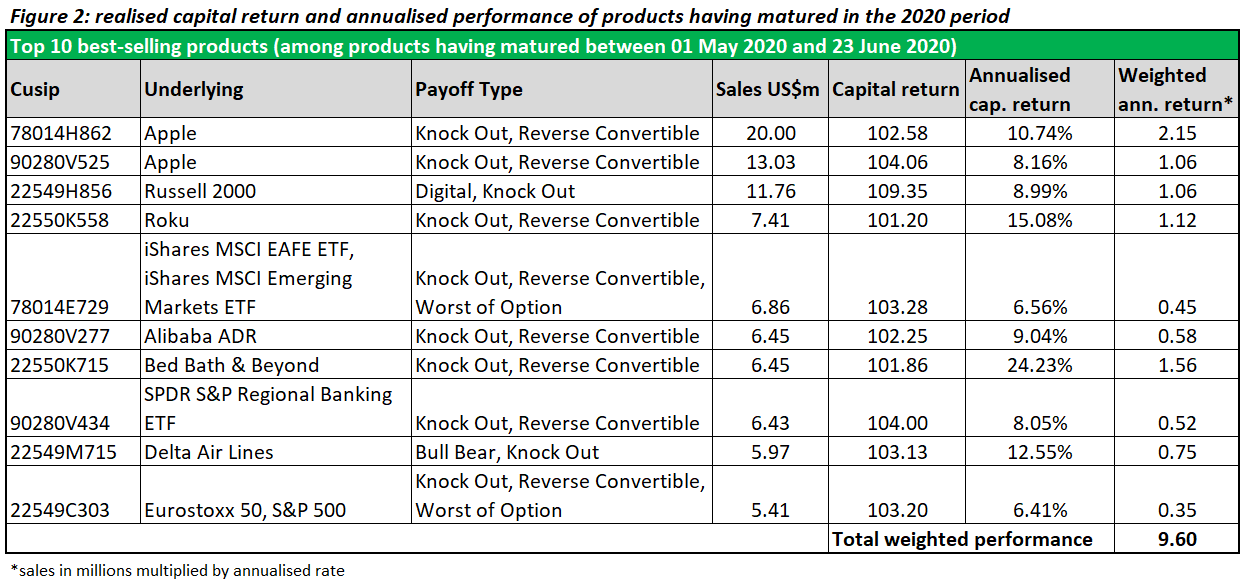

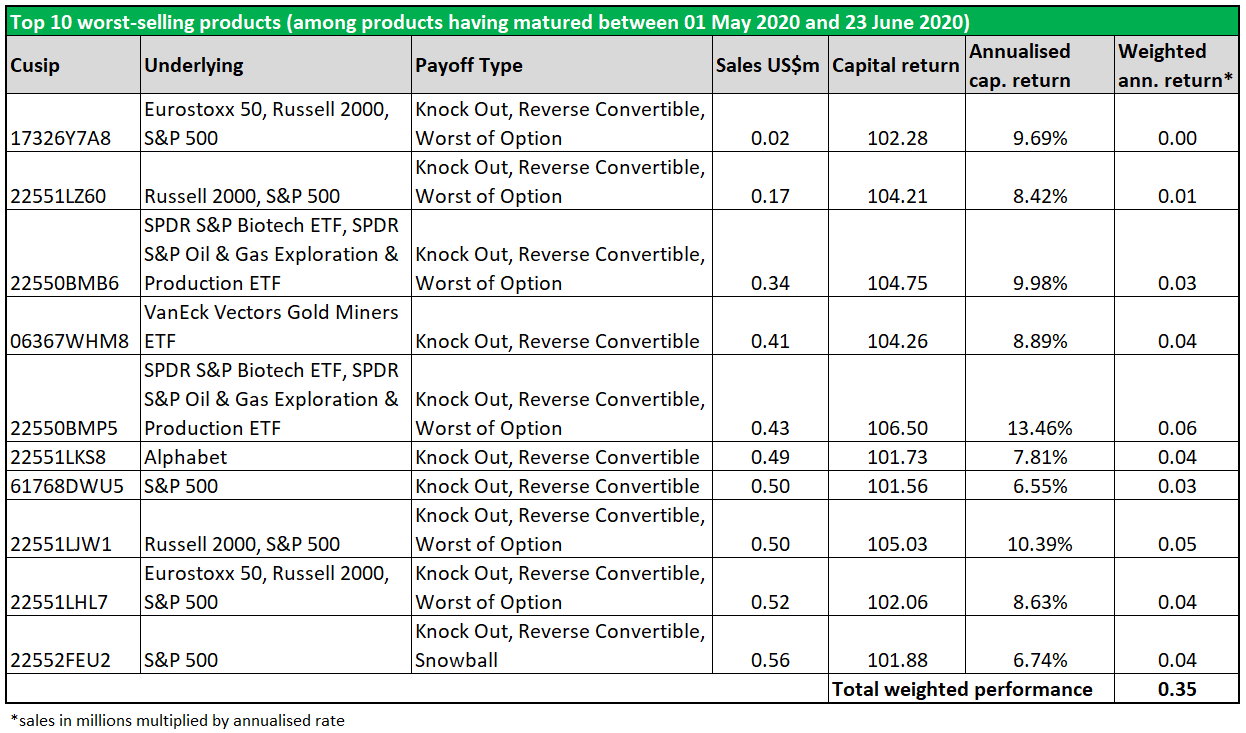

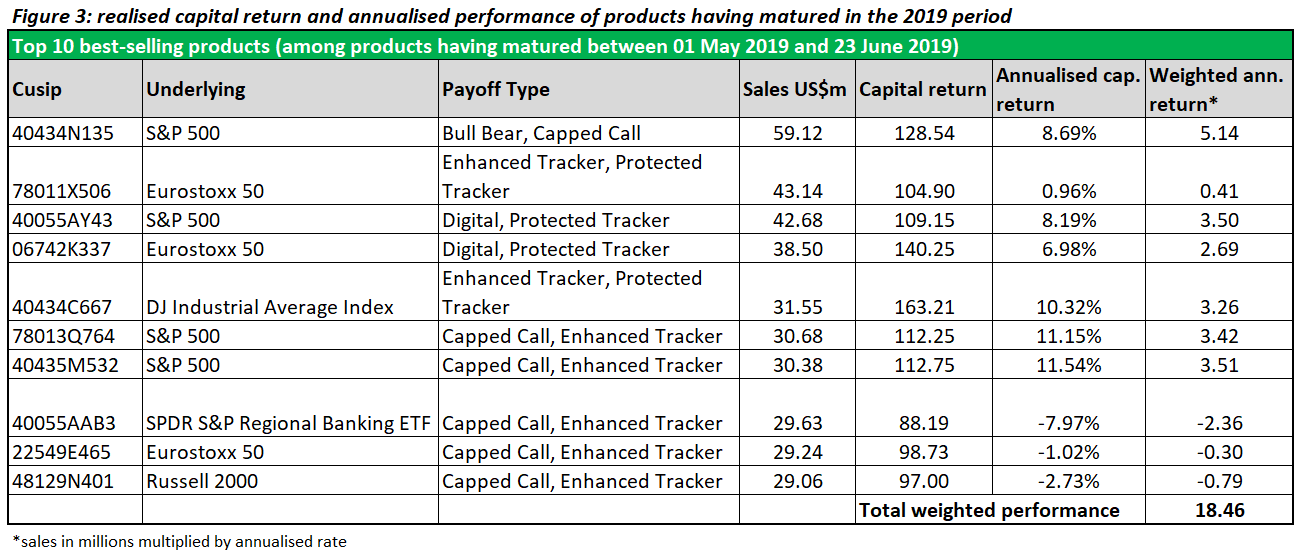

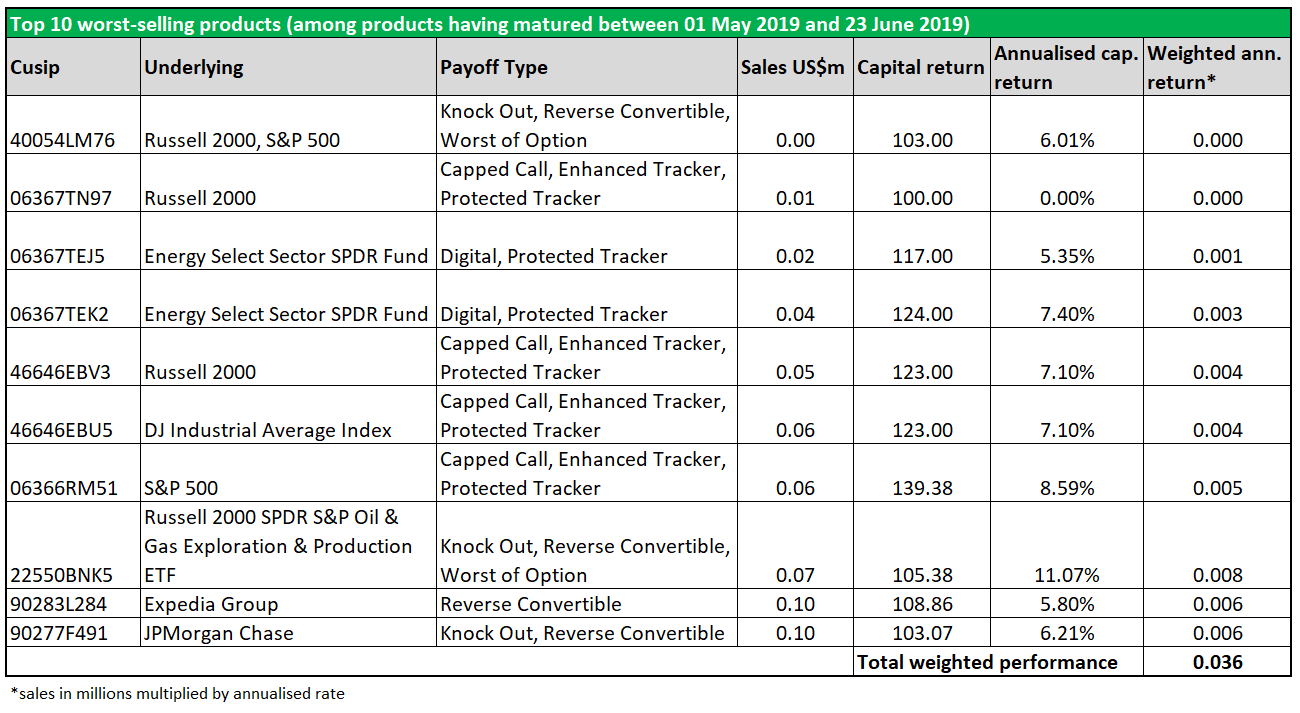

To conclude, beside the random variable from an inverse normal distribution the daily logarithmic changes of the underlying’s closing prices and its respective annualised standard deviation were extracted. The goal was to juxtapose projected performance of products that struck between 1 May 2020 and 23 June 2020 with the actual registered performance on products matured in the same period of 2020, as well as with maturing periods in the timeframe 1 May 2019 to 23 May 2019.

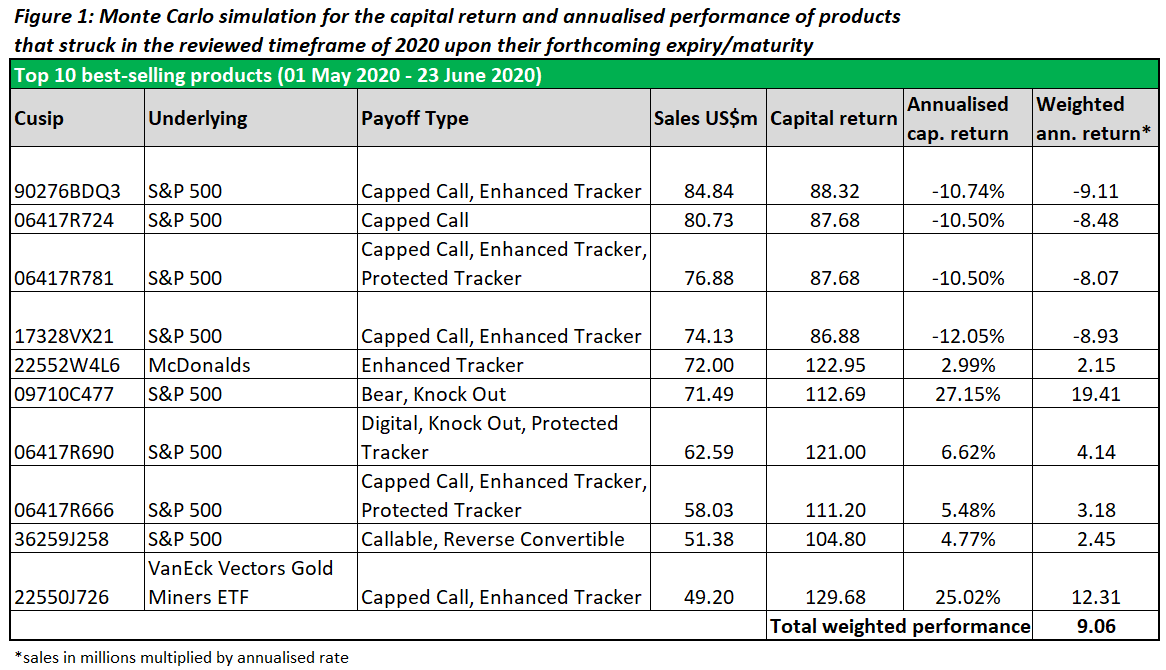

Composite weighted scores were computed by scaling recorded sales volumes in USDm by annualised performance.

One key finding is that weighted performance is expected to dwindle at the time of maturity on the most successful products striking between 1 May 2020 and 23 June 2020 despite sales volumes being significantly higher than for the other two checkpoints.

Several of the most widely sold products in the relevant 2020 period are likely to record adverse annualised performance of beyond -10% including a capped call, enhanced tracker product issued by UBS and distributed via the private banking channel which tracks the price fluctuations of the S&P 500 (CUSIP: 90276BDQ3), and a capped call, enhanced tracker, protected tracker rival product issued by BofA Securities also tracking the S&P 500 (CUSIP: 06417R781).

Some more optimistic scenarios for investors were identified where annualised performance rises above 25%. This was the case for a bear, knock out product which will expire early if the price of the S&P 500 closes at or below its strike price on the respective observation dates (CUSIP: 09710C477), or a BofA Securities product tracking the VanEck Vectors Gold ETF which offers 300% upside on the performance of the underlying, up to a maximum return of 45% (CUSIP: 22550J726).

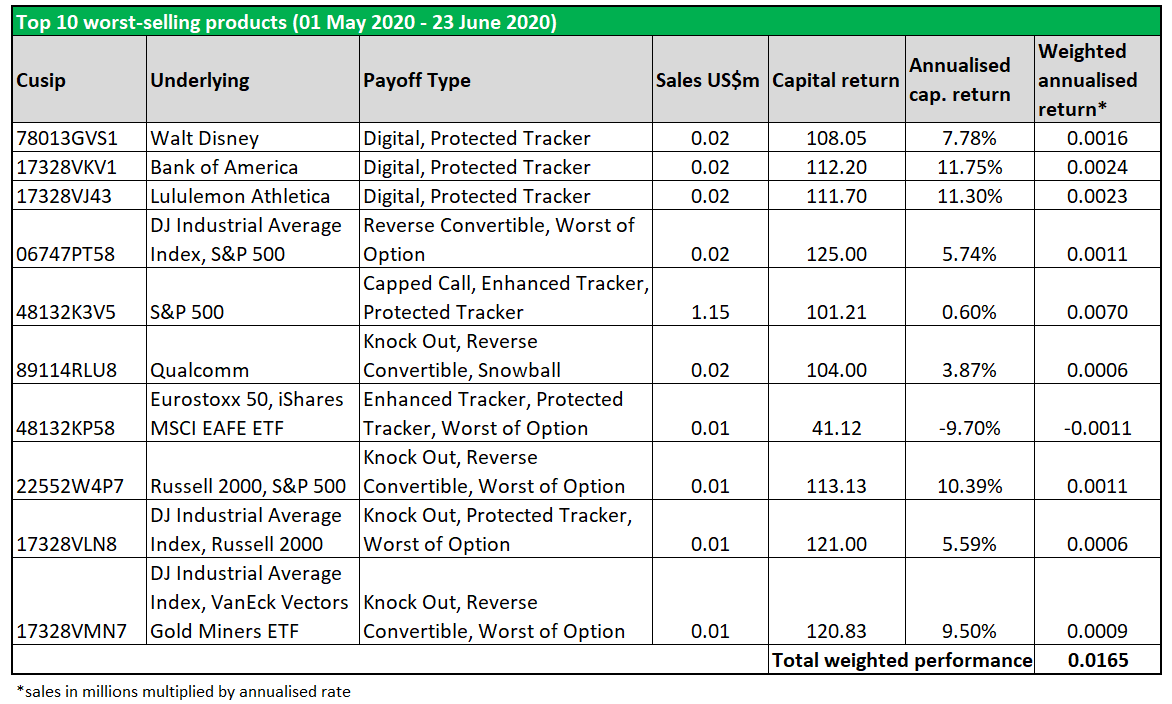

Out of the highest-selling products only one of them is expected to deliver negative annualised performance: a capped call, enhanced tracker, protected tracker product launched by JP Morgan Chase Financial with performance linked to the iShares Emerging Markets ETF (EEM) and the Eurostoxx 50.

Whilst the Eurostoxx 50 closing level is extrapolated to be down by 7.34% on its maturity date of 27 May 2025, the iShares Emerging Markets ETF is projected to fall by 58.88% of its initial value by then, breaching the 20% protection barrier provided by the protected tracker (CUSIP: 48132KP58).

Despite being seemingly shunned by investors, two products linked to Bank of America and Lululemon Athletica (CUSIPs: 17328VKV1, 17328VJ43) worth US$20,000 each are on track to deliver a sound annualised performance, based on our projections as they will capitalise on their digital, protected tracker payoff profile.

The product linked to Bank of America will deliver a fixed return of 12.2%, as long as the underlying price stays above 80% of its initial value upon maturity while the product linked to the Lululemon Athletica stock promises to deliver 11.7% if its closing price falls by no more than 20% at maturity.

While the Lululemon Athletica stock is expected to rise sharply by 43.77% from its initial valuation date set on 21 May 2020 to the average of its five valuation days (from 27 May 2021 to 3 June 2021 inclusive) and the downside barrier beyond which the digital return will fail to deliver, our simulation presents a far less spectacular outlook for the Bank of America stock, with its value shrinking by 18.29% from 5 May 2020 to the five-day averaging period prior to maturity (12 May 2021-18 May 2020). However, the buffer manages to absorb these losses and investors will recover their initial investment.