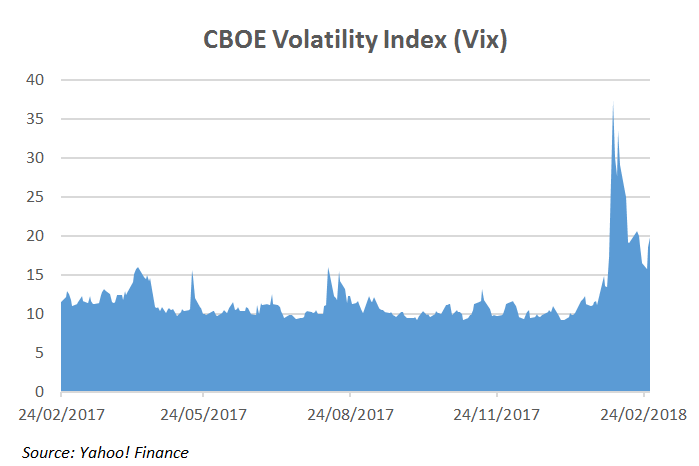

Volatility, the statistical measure of the dispersion of returns for a security or market index, reached its highest level in 2.5-years at the beginning of February, with the CBOE Volatility Index (Vix) closing at 37.32 points on February 5, after having traded at historical low levels for months. SRP asked Tom Karlsson (pictured), head of European options sales, at Susquehanna International Group - a market maker on listed equity options - about the impact of volatility on structured products.

Susquehanna provides liquidity, often to pension funds, hedge funds or asset managers who want to buy call or put options, and connects with the structured products market by working with the distributors that hedge their structured products, according to Karlsson. "We price all the European listed single stock options and also the index options, about 800 different underlyings in Europe. We are also able to provide access to US listed markets and liquidity there," said Karlsson.

Structured products exposure is traditionally hedged in two ways, said Karlsson. "Distributors have often done an over-the-counter (OTC) agreement, so not via the exchange, with the same pay-out profile defined in the agreement as what they sell forward to the end clients," said Karlsson, adding that this is usually done with the global investments banks and gives an exact hedge

"The other way, and what we have seen lately, is distributors breaking the risk down and actively managing the position. Rather than doing an exact hedge in the OTC market they now use listed options to hedge their volatility exposure."

When buying or selling an option, market participants are taking a view on volatility, according to Karlsson. "There are different ways to hedge that volatility and one way is the listed market," he said. "So rather than structuring our own products we trade both with the distributors and investment banks hedging their own structured product positions."

The reason distributors started trading in the listed market is to capture the volatility spread and keep more profits in house, according to Karlsson. "Their hedge is also cheaper this way because they are essentially being paid to manage the risk."

Where Karlsson sees the volatility affecting structured products is in the hedging activity as when volatility spikes, liked it did on February 5 and 6, we have witnessed distributors come in and sell the volatility which they are long from the client positions.

"Historically clients have been selling volatility in structured products, likely to get a pick-up in yield, he said. "When the end-client sells and the distributor buys, the distributor is long volatility and they need to hedge that position when volatility goes higher. That's when they are selling volatility via listed options to us."

According to Karlsson, distributors "don't want to, or sometimes can't keep a big open volatility position with their risk limits so when the volatility spikes we see more activity from distributors coming and selling that volatility to us".

"When volatility picks up, the distribution of new products appears attractive," said Karlsson. "Because that yield pick-up for the end client is potentially higher and the payoff may look more attractive compared to when volatility is at lower levels. When investors buy an option, they pay a premium which gives them a long volatility position and they benefit if the market is more volatile than what was implied by the level they paid."

When investors sell an option they receive a premium and benefit if the market is less volatile than what was implied by the level that was sold, according to Karlsson.

"Hedging structured products volatility position is possible in the listed options," said Karlsson. "We have seen these structured products flows, especially in Swiss, German and French single stock options. Outside that there is scope to grow the hedging flow in Spanish, Italian, UK and Nordic markets where there is much more liquidity that can be seen on the screens."

There are volatility products now which are linked to Vix and VStoxx, the US and European volatility indices, through which the investor gets a direct position in implied volatility "although delta hedged options are still the most common way to hedge this risk", according to Karlsson. "The volatility indices got a lot of bad press after highly leveraged reverse Vix products like Xiv lost most of its value and was unwound. It might take a while before these products gain traction again," said Karlsson.

It remains to be seen whether volatility will remain at a low level or will spike again in the months ahead, according to Karlsson. "We won't give trade advice or write client facing research but what I have heard from clients is that there seems to be some a consensus that we could be moving from low volatility to a higher volatility environment, mainly due to the central banks taking out their support," said Karlsson. "At the same time there is a chance that we could see some inflation and this could also bring volatility back to the market. It seems to indicate that because of a combination of those two, people do expect more volatile markets," he said. "As a market maker we are taking the volatility as fair where-ever it trades and provide two way market to the clients. We are not taking a view on specific volatility levels, just trying to manage the flow the best we can."

According to Karlsson, volatility is interesting as it is inherently mean reverting. "We will never see volatility go to zero because that would mean that nothing is trading," Karlsson said, noting that, at the same time, volatility cannot go up indefinitely "as stocks can in theory".

"As we saw in February 5 and 6 when Vix moved from 17 to 50, volatility can move up very quickly," said Karlsson. "Previously we have witnessed that when the underlying equity market sells off, the downward moves are more aggressive and this has been the opposite in the volatility. It will be an interesting year ahead," Karlsson concluded.

Related stories:

How does volatility affect structured products? It is very complex

How does volatility affect structured products? Clock patterns, fat tails and cones

How does volatility affect structured products? Premiums, curves and pricing