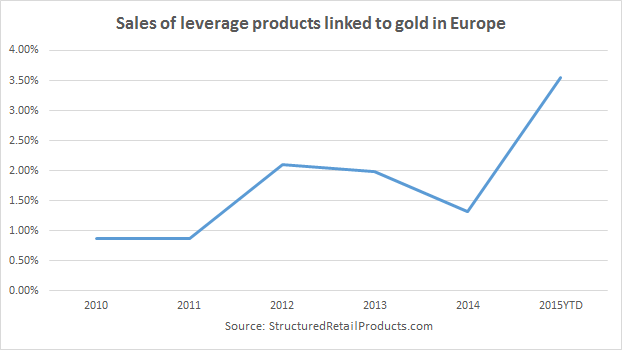

The interest in gold-linked leverage products in Europe is picking up despite the sideways fluctuation of the hard commodity over the last 12 months, with the issuance of products linked to the price of the precious metal increasing by more than 25% in the third quarter compared with the previous three months.

Sales in the retail derivatives market around gold were not very high, said Nicolai Tietze (pictured), gold expert at Deutsche Asset & Wealth Management. “Reasons are the low volatility, the lasting sideways movement of the precious metal and that many investors have turned away from gold as investment alternative,” said Tietze. “However, the interest of investors is returning with the anticipation of a break out of a downward movement of the gold, in particular knockout products.”

The number of leverage products in the third quarter of 2015 is higher in every month compared with any of the months in the second quarter, with the sales volume of issued products in the third quarter nearly 33% higher than the sales volume registered in the second, according to SRP data.

“We experience a constant flow in delta one products/certificates from customers buying the dips, but no exceptional flow,” said Michael Blumenroth, vice-president and gold expert at Deutsche Bank. “People always prefer being long on gold rather than being short, so the gold price recovery was a great boost for gold.”

The price of gold has risen by more than 4% from its five-year low in July, from $1,074 an ounce to $1,120 at the end of September. “The increase might be due to seasonal factors,” said Blumenroth. “During the summer months, demand is often slow [but] the autumn is often a good time to be long on gold, because of the wedding season in India, and the Christmas season in Europe and the US. Also, gold is considered to be a good buying opportunity by a certain type of investor following the ‘buy the dips’ strategy.”

Gold is perceived by clients as a safe haven investment, “so it might be reasonable to include it in the portfolio in the time of market turbulence,” according to Piotr Napierala, structured products manager at Bank Zachodni WBK. “Especially during the last few years, when its value remained flat or slightly negative at a time when equity markets provided quite stable positive performance,” he added. “The bank has offered two [options]: first, for [those with a view on the] stabilisation of the asset in a wider range; and, second, a purely growth strategy. Not surprisingly, as gold is now somehow in the middle of its seven years price range, the symmetrical strategy has raised higher demand than the bullish one”.

The US Federal Reserve’s suggestion that it will raise interest rates in the US has also played a role in the rally of the price of gold, according to Napierala. However, in some quarters it is believed that the Fed’s hypothetical rate increase might have quite the opposite impact on the price of gold based on historical data. “There has been a lot of noise regarding the Fed’s decision to raise interest rate, which may cause a further shift in US inflation,” said Napierala. “Gold is perceived as the inflationary hedge asset; historically, the value of gold has risen during the previous US rates increase – so, from that perspective it might also be reasonable to include it in the investment portfolio.”

Related stories:

Profile: Wisdomtree gains a boost from the short and the leveraged

Poland’s top product promises more but stalls in choppy markets

Deutsche Bank pushes leverage range in Switzerland via OTC platform

Leveraged products increase footprint in Hong Kong