13 Feb 2025

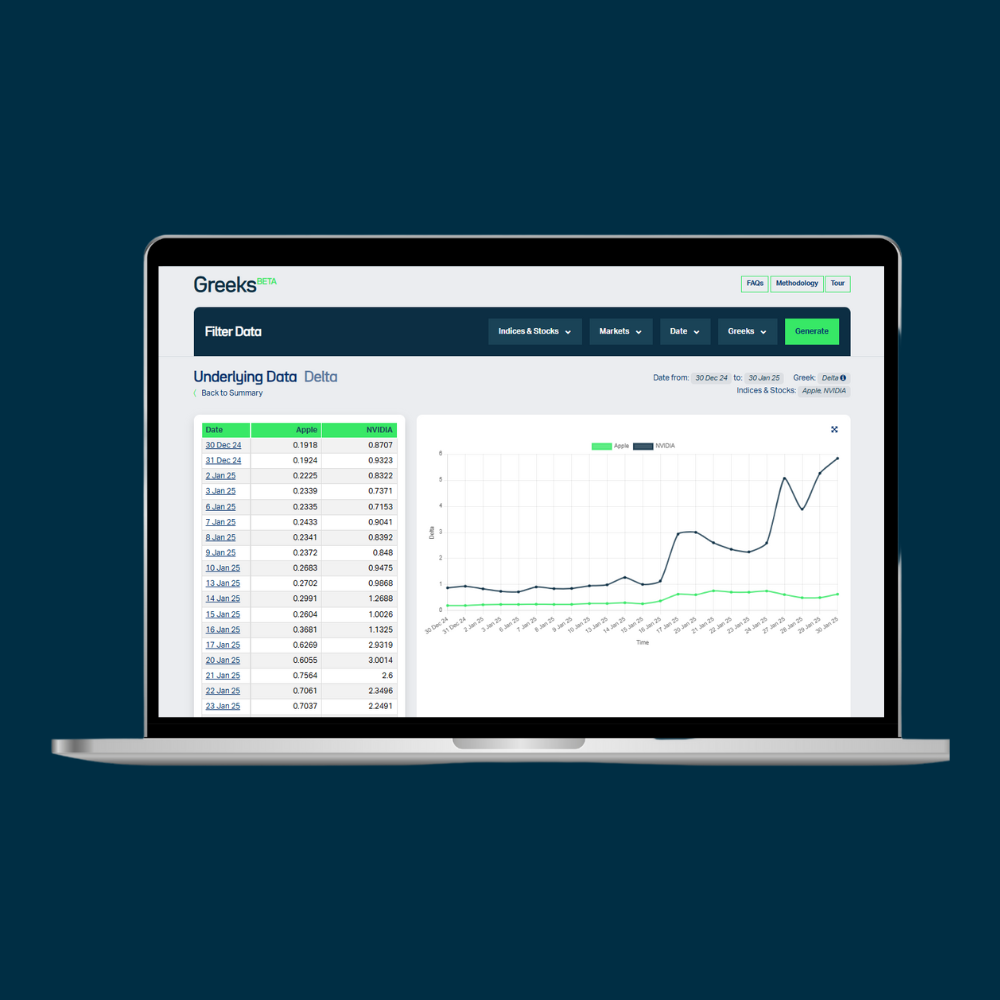

SRP Launches SRP Greeks: A New Platform for Greeks Data and Analytics

Structured Retail Products (SRP) has introduced SRP Greeks—an advanced solution for Greeks data.

25 Sep 2024

ANNOUNCEMENT: Derivia Intelligence Middle East 2024 conference – join the conversation!

Derivia Intelligence Middle East 2024 is the inaugural Derivia Intelligence conference, combining the FOW and SRP brands.

24 May 2024

SRP launches Wrapper Guide Asia Pacific 2024

The SRP Wrapper Guide Asia Pacific 2024 is out and available for download.

14 May 2024

ANNOUNCEMENT - SRP Platform Survey 2024

For over 20 years, SRP has been at the forefront of providing comprehensive data and market intelligence to the structured products industry.

25 Jan 2024

Introducing Derivia Intelligence — financial data and market insight provider

New SRP and FOW parent company Derivia Intelligence officially launched.

06 Jun 2023

SRP renews pledge for connected intelligence

SRP has got a sleek new look to reflect its values, modernise the business and distinguish its position in the market as a trusted source for structured products intelligence as it journeys into its third decade.

25 Jan 2022

SRP and FVC launch StructrPro

The new Life Cycle Management portal combines the power of SRP product data and FVC analytics and reporting.

26 Sep 2018

Is it August 2015 all over again?

For those who work in structured products and derivatives in 2015, August 3 was not a good day.

08 Jun 2018

Correlation – the new asset class for market-linked products

Common asset allocation strategies typically splits the investment portfolio into different asset classes, based on theory behind, following Harry Markowitz’s Modern Portfolio Theory stating that, because of asset correlations, portfolio risk, or standard deviation, was lower than that calculated by a weighted sum.