The UK asset manager has unveiled some of the equity derivatives (EQD) strategies adding value to investors in the current market environment in its latest research.

The asset manager’s latest monthly EQD research report for institutional investors shows that in November, call spread collar were deployed to protect equity exposure as they provided coverage against a drop of 0% to 20% and a capped upside.

‘The retained upside potential of the call spread collar looks attractive compared to historic levels in absolute terms, particularly for FTSE 100, Nikkei 225 and Eurostoxx 50 structures,’ stated the asset manager, which traded over £190 billion (USS$241.5 billion) notional of derivatives transactions in 2023, in its report.

Notably, the upside of the Eurostoxx 50 structure is currently uncapped, meaning it is not necessary to sell an out of the money (OTM) call to achieve a net-zero cost.

According to the report authored by Fakhreddine Chaabani and Sophie Martinec (pictured) at the risk managed investments (RMI) unit, risk reversal has also been used to mitigate moderate market declines of 0% to 10% with a structure that facilitates equity growth.

Risk reversal is a multi-leg options strategy that uses both a call and a put, sometimes referred to as an options collar strategy.

The current pricing for this kind of approach remains appealing as it benefitted from the sale of the 90% put, which provided sufficient cash to purchase in-the-money (ITM) calls, according to the report.

This structure has ‘a good potential’ as an equity replacement.

The report also pointed the condor strategies have benefited from equity markets moving sideways +/- 15%. However, the number of condors that can be purchased has fallen below the historical average, suggesting that ‘it is not an optimal time’ to implement this structure.

The Nikkei 225 index has the highest condor ratio amongst the four indices deployed with the monthly pricing attributed to the limited-risk within a non-directional options trading strategy consisting of four options at four different strike prices, the research found.

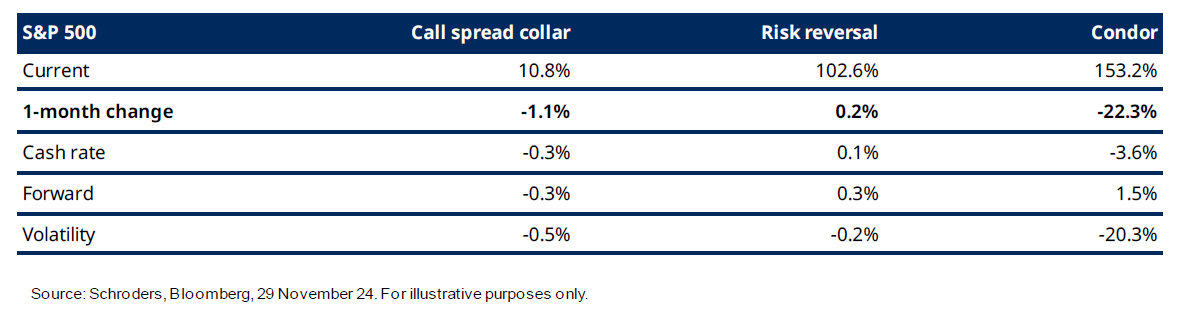

However, since the start of the month, the GBP cash rate has dropped by nine basis points, which had a negative impact on the three structures.

Trading vol

The S&P 500 forward rate increased by 24 basis points, negatively affecting the pricing for the call spread collar and risk reversal, but positively impacting the condor structure.

Additionally, there was more than a one-percent decrease in volatility, resulting in a negative impact on the call spread collar and the condor structures, whilst positively impacting the risk reversal.

Throughout November, the VIX saw a tick down, reflecting lower volatility in financial markets, and finished the month near the 25th percentile.

After spending the previous two months above its 75th percentile, the skew has now reverted to its median historical level.

‘The price differential between puts and calls is broadly in line with historical levels,’ stated the report.

Click here to read the report.

Do you have a confidential story, tip, or comment you’d like to share? Write to summer.wang@derivia.com