The Singaporean banking giant maintained its robust position in Taiwan, doubling structured notes distribution from last year.

Singapore banking giant DBS Group has reported strong earnings in the third quarter of the year, with net profit jumping 18% year-on-year (YoY) to SG$2.63 billion (US$1.97 billion), according to its latest financial report.

We achieved record income in the third quarter as net interest margin continued to expand and growth in commercial book non-interest income was sustained - Piyush Gupta

Total income rose by 16% YoY to a record high of SG$5.19 billion during the July-September quarter. Net interest margin, a key profitability gauge, ticked up for the seventh consecutive quarter to reach 2.19% by the end of September.

‘We achieved record income in the third quarter as net interest margin continued to expand and growth in commercial book non-interest income was sustained,’ Piyush Gupta (pictured), CEO of DBS, said in the statement.

Yet, treasury markets total income shrank 38% YoY to SG$166m in Q3 23 from SG$269m in Q3 22 due to the higher funding costs. The bank stated that there are offsets between net interest income and non-interest income due to ‘accounting asymmetry, for example in equity and FX swap products’.

On 12 August, DBS completed the acquisition of Citi’s consumer banking business in Taiwan, making the Singaporean bank the largest foreign bank in Taiwan by assets. The consolidation of Citi Taiwan contributed SG$ 10 billion to loans, the bank highlighted.

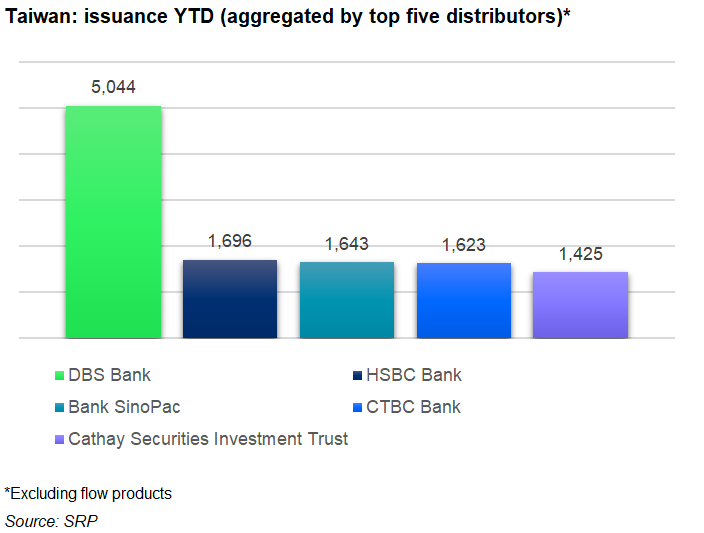

Structured products

Although the bank does not provide any structured products data from its treasury in Singapore, DBS is an active provider in several other Apac markets. SRP data shows that in Taiwan, YTD DBS Bank distributed some 5,044 structured notes worth US$12.8 billion in the estimated sales volume, topping the league table in the jurisdiction that makes up 20% of the market share.

The latest distribution figures in Taiwan doubled compared with the prior year's same time, which recorded 2,500 structured notes with an estimated sales volume of US$6.7 billion.

This year the popular underlyings remain similar trends from last year’s, such as the shares of Nvidia (1,285), Advanced Micro Devices (1,252), and Tesla (1,156).

The Singaporean bank also maintained its activity in the Chinese market, with 29 products marketed YTD. 14 of them linked to FX rates.

Meanwhile, according to the bank’s leverage ratio common disclosure, total derivative exposure measures stood at SG$52.5 billion, up eight percent quarter-on-quarter (QoQ).

The increase stemmed from higher replacement costs associated with all derivative transactions and potential future exposure associated with all derivative transactions, while written credit derivatives’ adjusted effective notional slid.

Outlook for 2024

Gross fee income in wealth management saw a 22% YoY increase to SG$393m in Q3 23 from ‘higher bancassurance and investment product sales,’ while investment bank dropped 16% to SG$21m on ‘slower capital market activities,’ Chng Sok Hui, DBS’s chief financial officer (CFO) said during the media briefing call following the earnings release.

Gupta sees the net interest margin (NIM) ‘probably peaked’ during the quarter.

‘I do not see more Fed rate hikes and therefore NIM will be unlikely to go up further from here,’ he said in the call.

‘I think rates are going to stay higher for longer, but with them where they are, a slowdown can be expected in the West,’ he continued. ‘For China, I think we could have seen the bottom. The measures since July should put a floor under the property market.’

Looking ahead to 2024, he sees the bank will get double-digit growth in fee income and overall non-interest income.

‘Overall, we could get mid-single-digit total income growth – two to three percent organically and another two to three percent from Citi Taiwan,’ he added.

Click the links to review DBS Group’s Q3 2023 trading update, CEO presentation, CFO presentation, and pillar 3 and liquidity disclosures.