The L&S ETP specialist has signed Goldman Sachs as a prime broker to address collateral issues and bolster growth.

ETP provider Leverage Shares has been ranked on the 2023 Inc. 5000 list of the fastest-growing private companies in the US.

We’re seeing more and more asset managers come to us with more active strategies they want to put in the ETP wrapper – Oktay Kavrak

Over the last few months, Leverage Shares has “increased the number of products that the company has on the market and its revenues” as well grown its work force “internally with new hires”, according to Oktay Kavrak (pictured), head of product strategy, Leverage Shares.

“We’re seeing more and more asset managers come to us with more active strategies they want to put in the ETP wrapper – mainly due to access to retail and institutional clients across Europe and the UK,” said Kavrak. “That is one of the biggest challenges existing wrappers have, whether it's a mutual fund, a hedge fund, or another type of structure.”

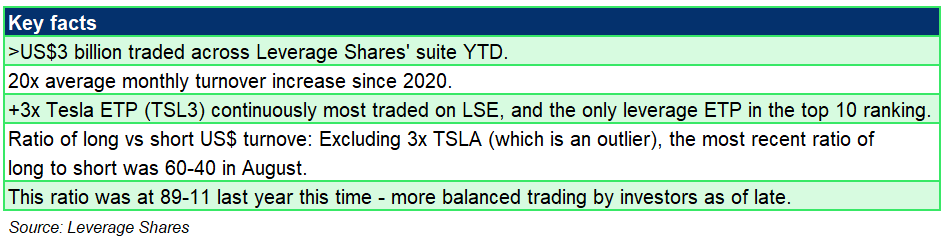

The Inc. 5000 ranking shows that Leverage Shares is 1,456 out of the 5,000 fastest-growing private companies in the US, a growth that has been supported by the company’s activity in Europe’s exchanges and its white-label service launched at the end of 2024 - the company has seen over US$3 billion worth traded across its products, which collectively make up nearly 10% of all ETPs listed on the London Stock Exchange.

“We are on the verge of signing our fourth white-label client and potentially a fifth one in Q4 2023,” said Kavrak. “With regards to trading on our own products, this year so far, in terms of average monthly turnover, we have seen a 20x increase since 2020.

“Compared to the first half of last year, we have had a 50% year-over-year growth. We’re seeing increasing appetite and pickup in these products.”

Margin loan

Back in July, the short and leveraged (S&L) specialist ETP provider acknowledged investors did not receive the full advertised amplified returns on its +3x Tesla ETP for six days as Europe’s largest US$315m S&L ETP experienced ‘significant tracking error’ due to ‘technical issues with the margin loan provider’.

This saw the degree of leverage applied to the underlying exposure drop to 2.8x during sessions where Tesla stock rallied 6.6% in total.

However, the company stands “firm in the belief in the superiority of the physically backed ETP structure over swap-based solutions”, a conviction validated by the sustained success of the 3x Tesla ETP which is the most traded ETP on the London Stock Exchange.

“Pretty much all physical ETFs experience tracking error at some point or another and to varying degrees,” said Kavrak.

“Given the unprecedented interest in our ETPs, we’ve now added Goldman Sachs as an additional prime broker to bolster the growth of our ETP platform.

“This is a key step to minimise similar risks and build for expected future growth. With plans on introducing more disruptive products in Q4 of 2023, we are preparing our firm for the next tier of our expansion.”

What is driving the company’s growth strategy at this stage?

Oktay Kavrak: Marketing is a big part of the puzzle. It is important to have a wide offering to ensure traders have a wide array from which to choose when certain things happen in the market. While we can’t dictate investor preferences – like making Airbus more popular than Tesla – there's going to be times around key market events like earnings releases that's going to have traders interested in underlyings outside just the ‘FAANGs’.

Until now, we focused mainly on single stock underlyings, but moving forward, we’re working on a pipeline of more differentiated strategies focused on non-leveraged trackers and more on the active side.

What kind of investors are using Leverage Shares’ ETPs? Do you have a breakdown in terms of institutional versus retail?

Oktay Kavrak: Unfortunately, that's one of the biggest black boxes when you're an ETP issuer. We can only gauge the landscape somewhat via client outreach – which suggests a fairly balanced split.

A lot of ETF/ETP trading is still done OTC in Europe. One of the interesting things about our products is that they trade a lot on-exchange. Most of the turnover happens on-exchange and the trade size is probably at a fraction of what they are for traditional ETFs - indicating a more dynamic trading strategy employed by our investors.

It shows that people are getting in and out of these products quite quickly. On a normal day, we can see anywhere from 25 to 50% of the ETPs’ AUM being turned over. That shows us that these are sophisticated investors who understand the products and are using them tactically rather than to buy and hold.

How do leveraged/inverse ETPs compare to pure tracker ETFs in terms of trading activity?

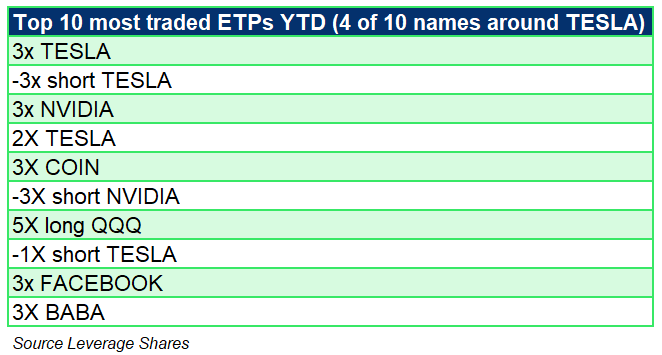

Oktay Kavrak: A recent newsletter from the London Stock Exchange for July 2023 shows that among the top 10 most traded ETPs, nine of the 10 were traditional ETFs – and all from iShares. The only leveraged ETP and the only non-iShares product that made the list was 3x Tesla (ticker TSL3).

3x Tesla remains our flagship product and continues to drive a lot of trading activity. The company’s polarising CEO and investors’ insatiable appetite for trading the stock in both directions remains strong. But in general, 3x Tesla, 3x Nvidia, 5x QQQ and 3x Coinbase are the most popular products of our range.

What is your take on the use of ETPs linked to an ETF? What are you adding on top of the ETF for investors to choose the ETP as opposed to the ETF?

Oktay Kavrak: If you already have an ETF as underlying, there's just going to be an added layer of fees. If a client has access to buy the ETF directly, it probably makes more sense to do that.

However, our ETPs come into play effectively when there are specific needs that necessitate such a structure. In terms of client access, as you know, non-professional European investors can't buy US-domiciled ETFs. Our White Label ETPs are a fantastic solution to that problem – and we’ve already done it for one of our white label clients in the US, by wrapping their existing US ETF into a Priips-compliant and Ucits eligible ETP.

This provided them with distribution capabilities across Europe and the UK. The white labelled ETP literally just holds their ETF as underlying. So, while we handle all the regulatory documents, trading and reporting for them, they can focus on their main strengths – running their strategy and growing AuM.

Given the uncertainty regarding market direction, is investor appetite changing towards shorting the market?

Oktay Kavrak: Despite market turmoil throughout 2022, around 75% - 80% of trades are still on the long side and most of the action is still around ‘Big Tech. That’s not to say the others don’t get their day in the sun, but this usually happens after substantial moves on the stock(s) they track (i.e. when the underlying crashes). Investors often believe the market has overreacted, so they want to get – in some cases three or two times more exposure - in anticipation of a strong rebound.

In the European ETF space - actively managed ETFs will become increasingly popular as the industry matures. Most investors already have broad index exposure as their core, so they're going to seek alternatives in the satellite portion of their portfolios – whether it’s active, short/leveraged or thematic.

How would you rate the marketing environment in relation to demand for ETPs? what’s your assessment of 2023 so far, and what’s your expectation and outlook for the rest of the year?

Oktay Kavrak: I'm pessimistic because of all the optimism lately. What I think is going to be interesting to watch is the average consumer as excess savings from Covid are basically depleted - so consumption is being financed with personal debt. However, they’re soon going to have to pay that debt back at much higher rates. That’s when we’ll get a better indication of how strong the consumer really is.

I’m leaning towards a soft or ‘no landing’, but let’s not forget that recessions usually begin when unemployment is at record lows, not the other way around. So, I think people should still be cautious and look out for what the Fed does at the next few meetings.

My personal view is that investors might want to consider an equal-weighted ETF for broad market exposure. I would not want that concentration on the top seven names anymore although we know they've been a key driver of the performance year-to-date. If I had to choose, I would say that the old economy sectors like energy and manufacturing [are] probably going to outperform for the next three to six months.