There are over 8,500 live products worth an estimated US$25 billion issued on Credit Suisse’s paper across markets – some will transfer overtime to UBS.

The acquisition of Credit Suisse by UBS is reminiscent of J.P. Morgan’s takeover of Bear Stearns in 2008 for a discounted price of US$240m. The troubled US bank had once been valued at US$140 billion. This time UBS is paying US$3 billion when Credit Suisse was valued at US$8 billion (17 March) before the deal was brokered.

Credit Suisse will continue to operate ‘in the ordinary course of business’ and collaborate with UBS as the restructuring and integration goes ahead.

[It] is attractive for UBS shareholders but, let us be clear, as far as Credit Suisse is concerned, this is an emergency rescue - Colm Kelleher, UBS

With the announcement Credit Suisse joins the historic failures of banking giants which in the past have signalled the beginning of market crises and recession.

As with previous cases seen in the structured products market – albeit involving smaller transactions – with the integrations of RBS's Structured Retail Investor Products and Equity Derivatives (IP&ED) and Commerzbank’s equity markets & commodities (EMC) businesses by BNP Paribas and Société Générale, there will be no changes for existing investment products and flow products issued by Credit Suisse for the time being.

Issuance will continue with a transfer over time of the issuer to UBS, and the existing product range will be maintained and updated by Credit Suisse until further notice.

“It’s business as usual for now,” a CS spokesperson told SRP.

UBS said in a statement today (20 March) that UBS Investment Bank ‘will reinforce its global competitive position with institutional, corporate and wealth management clients through the acceleration of strategic goals’ in global banking while managing down the rest of Credit Suisse’s investment bank.

The combined investment banking businesses account for approximately 25% of UBS’ risk weighted assets (RWA).

UBS chairman Colm Kelleher (pictured) set the tone of the acquisition: ‘[It] is attractive for UBS shareholders but, let us be clear, as far as Credit Suisse is concerned, this is an emergency rescue. We have structured a transaction which will preserve the value left in the business while limiting our downside exposure.’

“The acquisition has been forced upon UBS somehow. The price they are paying reflects the concerns around this transaction,” a market source told SRP.

UBS reported last week lower revenues in its equity derivatives business in its Q4 22 earnings report - the underperformance of the derivatives & solutions unit saw the bank’s global markets revenues dropping 11% to US$1.35 billion year-on-year, while revenues at the markets division fell 13% to US$541m year-on-year (YoY).

Not alone

Credit Suisse has been on the radar of distributors of structured products for some time as CDS levels increased and questions around the bank’s credit quality as a derivatives counterparty arisen, but no issues have been reported so far.

Clive Moore (right), managing director, at UK structured products specialist distributor Idad, said: “We’ve had them on watch for a while, but no issues with liquidity on the live trades we have, and prices aren’t reflecting the CDS levels at all on any sell backs,” he said.

“The bank, like others, clearly has some issues with asset/liability matching but I’m comfortable there will be support for senior debt if needed (where we are) and likely all the way down.”

According to Moore, the general banking model is coming under scrutiny at the moment – not all depositors and bondholders can have their money back at once ever – but he thinks this will pass.

“There’s a lot of speculation in the CDS market which is pushing up the levels over those periods where the market is more speculative, less so over periods that are actually used to protect portfolios, which suggests this is less of a concern than it may appear to headline writers and speculative traders,” said Moore.

“We’re certainly being careful regarding any exposure clients have.”

Expanded footprint

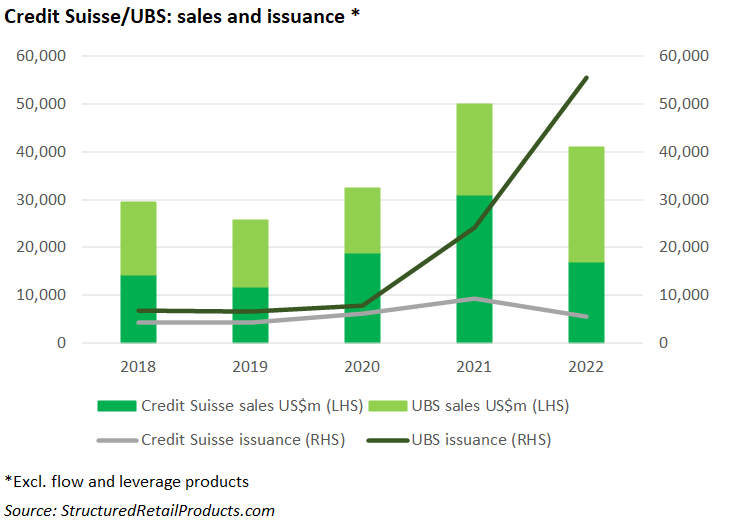

In the global structured products market both banks have been traditionally in the top 10 issuer ranking - the combined issuance and sales would put UBS as the third biggest issuer in the market globally.

Most recently, UBS saw its activity in the US plunge with its sales volume of retail structured products hitting a record low in Q4 22. The Swiss bank issued 574 retail structured products worth US$1 billion in the US market in Q4 22, half of the sales volume compared to the same quarter in 2021, and a 21.6% decline compared with Q3 22.

All in all, UBS sold 3,795 products at US$6.6 billion in 2022, becoming the fifth largest issuer and the first foreign provider in the US with a seven percent market share after J.P. Morgan, Citi, Goldman Sachs and Morgan Stanley. Compared with 2021, its sales volume decreased by 22.7%.

UBS also faced a US$25m fine in Q3 22 to settle investor fraud charges related to its UBS Yield Enhancement Strategy (YES). In Europe, UBS issued 11,366 structured products and in Apac, it was the issuer of 1,911 structured products across Taiwan (474) and Hong Kong SAR (1,437), including listed products.

Leading franchise

Credit Suisse, on the other hand, remains a top player in the global retail structured products market although it has seen its footprint reduced over the last 12 months – the bank issued over 9,000 products worth US$17.9 billion in 2022 compared to almost 15,000 products worth an estimated US$31 billion in 2021.

According to SRP data, there are almost 8,500 live products worth an estimated US$25 billion issued on Credit Suisse’s paper across markets.

In its annual results published on 14 March, Credit Suisse reported liabilities of CHF66m (US$71.3m) relating to medium-term notes and CHF1.1 billion in negative replacement values of derivative financial instruments.

“UBS will also have to continue to make available the indices developed by Credit Suisse – in the event that an index is discontinued, or its calculation is changed substantially UBS will be required to substitute it with a comparable index as per the product terms,” a market source told SRP.

There are more than 31 Credit Suisse-branded proprietary indices used in more than 400 live products sold across eight markets retail markets.

The Credit Suisse RavenPack AIS Balanced 5% ER Index is one of the most recent additions to the Credit Suisse index suite - the traded notional of derivatives linked to this index only exceeded US$1 billion as of the end of 2021, as reported by SRP.

Last but not least, UBS may also have to make provisions to deal with upcoming class-action claims in a case alleging that Credit Suisse engineered a complex fraud in 2018 to sink an exchange traded note linked to the “fear index,” and profit from losses by investors.

The lawsuit claims investors lost US$1.8 billion in the 5 Feb 2018, collapse of the market for VelocityShares Daily Inverse VIX Short Term Exchange Traded Notes, known as “XIV Notes.

US District Judge Analisa Torres ruled Thursday that investors who sued can bring class-action claims to be heard by the court. The Swiss bank has defeated several lawsuits over products linked to the CBOE Volatility Index in the US market following the volatility swings of early 2018 which hit short/inverse VIX investors.