The certificate industry in Austria is confident about the months ahead with luxury goods, utilities and pharma all sectors to look out for.

More interest rates hikes are expected in the first quarter of 2023, according to four experts who took part in the fifth virtual certificate round table organised by the Austrian certificate association (Zertifikate Forum Austria or ZFA) on 19 January 2023.

However, rate hikes are likely to be moderate and during the year, or for 2024, the first cuts are already forecasted, said Philipp Arnold, head of certificates sales & marketing at Raiffeisen Bank International (RBI).

‘This could temporarily trigger higher volatility in the stock markets due to the tendency to falling inflation and resolution of supply chain issues, however, we believe in a positive development of the stock markets,’ he said.

Raiffeisen currently favours growth over value and expects tech and pharmaceutical stocks to make a clear recovery from the middle of the year.

The European stock exchanges are proving to be very robust - Frank Weingarts, Unicredit

Uwe Kolar, head of retail and sparkassen (savings) sales at Erste Group Bank, also sees interest rates rising in 2023, which is reflected in the selection of investment products by customers. Kolar initially expects some turmoil in the markets for 2023, ‘but certificates are a good way to build bridges,’ he said.

For Kolar, stocks in the tech sector are on the rise, while luxury stocks like LVMH or utilities such as EVN and pharmaceutical companies like Lilly are ‘interesting shares with charm’.

‘Given the increased interest rates I would now increasingly recommend mixed equity-bond portfolios,’ said Kolar.

According to Frank Weingarts (pictured), head of private investor products for Central & Eastern Europe at Unicredit Onemarkets, and chairman of the ZFA, the year got off to a ‘brilliant start’, but there is still a lot of uncertainty ahead. ‘Unicredit sees 2023 as a year of transition with a positive end,’ said Weingarts.

High energy prices will continue to have a negative impact and although they are declining again, lagging effects are becoming noticeable: ‘Some products and services, for example in the construction industry, are only now becoming more expensive […] the inflation will therefore accompany us for a while,’ said Weingarts who admitted that overall, the supply chain problem is decreasing, which is having a positive effect on the stock exchanges.

‘The European stock exchanges are proving to be very robust. The Stoxx Europe 600 has stabilised and has regained the price levels of February 2022 just before the conflict in Ukraine.

‘We therefore believe in equities and equity-based products,’ said Weingarts, adding that a higher year-to-date growth is within the realm of possibility—especially for companies that pass the higher prices on to consumers.

‘Furthermore, cyclicals are likely again become more attractive,’ he said.

David Hartmann, Vontobel’s product manager flow products distribution, said consumer behaviour is changing after the high inflation caused real wages to fall, especially since growth in China has stalled.

‘The affluent middle class there is no longer growing as quickly as in the past and companies are therefore selling less in China, which is fuelling the recession,’ he said.

Hartmann ruled out a renewed increase in inflation in the euro area. He believes food and energy prices will be ‘stable’ in 2023 with further increases ‘inconceivable’.

On the investment side, the Vontobel expert recommended multi-reverse convertible bonds.

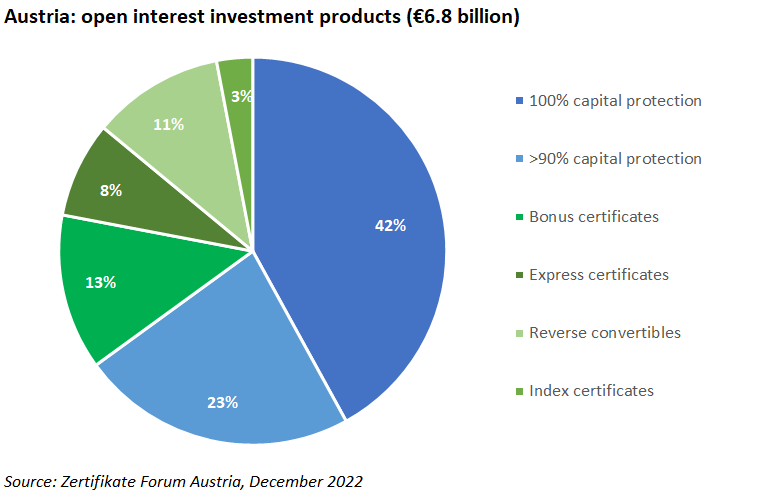

According to the ZFA market report for December 2022, €6.8 billion was invested in structured products at the end of last year. The bulk of the volumes, at €4.4 billion, was invested in products offering full or partial capital protection with a further €0.9 billion invested in bonus certificates.

Turnover of structured products stood at €201.5m in December – down 20.6% month-on-month (MoM). Products offering 100% capital protection registered the highest turnover (€88.4m), despite selling -25.4% less compared to November while turnover for reverse convertibles, at €59.9m, increased by 17.8% MoM.

The outstanding volume of investment products fell by 2.1% compared to November. Price-adjusted net cash inflows of €2.6m were registered during the month. The total market structured products market (including leverage products) grew by 0.80% to €13.7 billion.

Click the link to read the ZFA market report for December 2022.