The Canadian bank has reeled back on its structured product issuance in the first quarter of 2021.

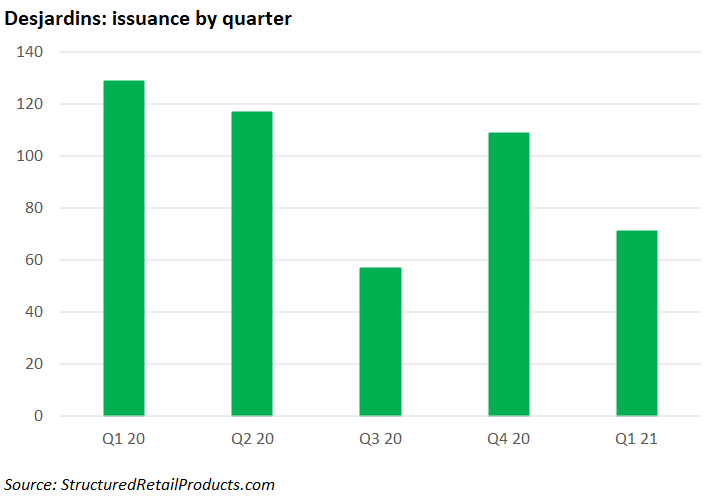

Canada’s Desjardins has seen its issuance of structured products decrease during the first half of 2021 - with 71 products compared to 109 in the previous quarter and 129 in the same period a year prior.

The bank’s issuance followed an erratic pattern during 2020 with product totals crashing to 117 and 57 in the second and third quarter, respectively.

The bank’s issuance spread among underlying sectors has also diminished in Q1 21 with fewer structured products being tied to the pharmaceuticals and biotechnology sectors than in previous quarters. Volumes tied to sectors such as telecommunications, oil and gas, banks, food and beverage, as well as utilities have also shrunk during this period, compared with the final quarter of 2020.

The majority of the bank’s products are tied to share basket asset classes with the most recently issued structure - the Desjardins Global Equity Principal Protected Notes, Series 67, F-Class - featuring a seven-year term with a strike date of 26 February 2021.

This growth product is wrapped as a note with an uncapped call payoff type and tracks the performance of an equity basket that includes BCE, Nippon Telegraph & Telephone, Swisscom, Woolworths, Nestle and Toronto Dominion Bank.

SRP data shows that Bank of Montreal issued the highest number of products (363) during the first quarter of 2021 in the Canadian structured products year to date, followed by CIBC with 313 products, National Bank of Canada with 296 products, Scotiabank with 126 products, Toronto Dominion with 92 products, and RBC with 81 products.

Earnings

The bank led by president and chief executive officer Guy Cormier (pictured) reported a net interest income of CAD1.4 billion (US$1.16 billion)) in the first quarter, compared with CAD1.45 billion in Q4 20 and CAD1.35 billion in Q1 20.

Investment income for the year was CAD276m, up CAD217m from fiscal 2019, because of higher trading income from Desjardins Securities.

The increase was also the result of higher gains on the disposal of securities and a favourable fluctuation in the fair value of derivative financial instruments, in part due to lower interest rates.

The provision for credit losses was CAD867m, an increase of CAD499m from fiscal 2019, primarily due to the deterioration in the economic outlook as a result of the Covid-19 pandemic, as well as the increase in the allowance for impaired loans in the business loan portfolios.

Non-interest expenses were CAD4.9 billion, a jump of CAD118m or 2.4% compared to fiscal 2019, mainly due to business growth, as well as an increase in investments, especially in the digital shift and information security.

Click here to view the bank’s earnings release.