Trading income at Korea Investment & Securities (KIS) dipped over three-quarters (77.9%) to KRW99.1 billion (US$89.2m) in FY20 ended in December 2020 due to ‘massive ELS hedge trading loss’ at KRW114.5 billion in Q1.

This led to net operating revenue falling to KRW1.47 trillion, down 4% year-on-year (YoY).

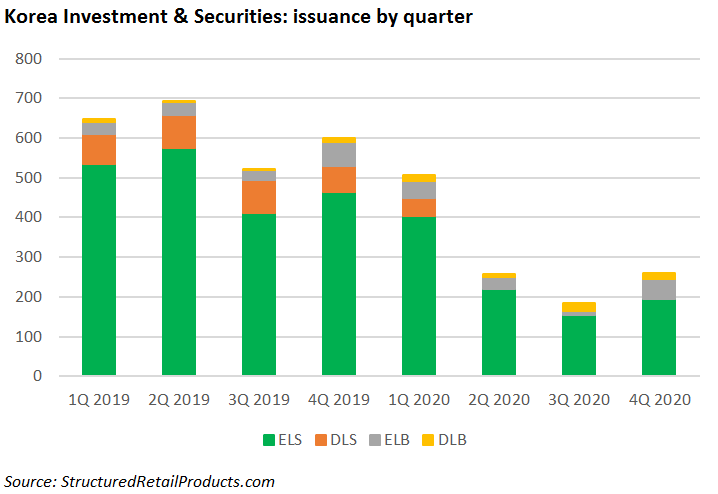

The South Korean investment bank's issuance volume of equity-linked securities (ELS) and derivative-linked securities (DLS) plunged by 62.7% to KRW3.48 trillion in 2020 YoY owing to ‘sluggish demand for ELS/DLS products and conservative risk management,’ according to the company’s FY20 earnings report.

In contrast, the issuance of equity-linked bonds (ELB) and derivative-linked bonds (DLB), which are principal-protected, remained stable at KRW5.96 trillion. And the sum of ELS, DLS, ELB and DLB was down by 36.2% YoY to KRW9.45 trillion.

As of the end of 2020, the issuance balance of ELS and DLS decreased by 36.2% and 28.3% to KRW3.56 trillion and KRW330 billion, respectively, as the market recovery from Q2 accelerated early redemption.

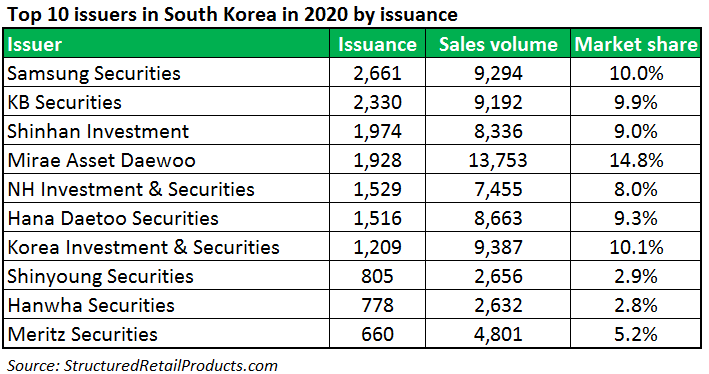

SRP data shows that in 2020 the issuance of structured products at KIS, headed by CEO Il Mun Jung (pictured) has plunged by 50.9% YoY to 1,209 with no DLS issued since 12 March 2020.

Asset management income also fell by 21.6% to KRW264 billion as ELS and DLS sales fees and fund sales fees decreased by 21.1% and 9.4% to KRW165.6 billion and KRW79.1 billion YoY, respectively. Financial product sales fees income dropped by 12.6% YoY due to ‘the decrease of ELS/DLS early redemption and private equity funds’.

As of the end of 2020, ELS and DLS delivered the lowest year-end balance of KRW840 billion after hitting KRW1.64 trillion in 2016, which represented a drop of KRW100 billion from the end of 2019. They made up 2.8% of the total financial product balance.

In addition, KIS reported that brokerage commission, brokerage-related interests and investment banking saw their income rising by 109.8%, 16.9% and 33.7% to KRW381.9 billion, KRW209.4 billion and KRW516.9 billion YoY, respectively.

Total net operating revenue at the subsidiary of Korea Investment Holdings accounted for 68.1% of that at the parent's consolidated balance sheet. The group posted a net profit of KRW859.9 billion, up 1.5% YoY.

KIS has slipped to the seventh position in the country’s issuer ranking by issuance amid the overall cutback seen in South Korea in 2020. The company’s structured products were distributed in-house and comprised 971 ELS, 136 ELB, 47 DLS and 55 DLB, SRP data shows.

By underlying, the S&P 500 index took over Eurostoxx as the most featured underlying for ELS and DLS. The US index was tied to 841 products while the latter replaced Hang Seng China Enterprises Index as the runner-up. The top three underlyings by issuance were followed by the Kospi 200 and Nikkei 225.

KIS also introduced the S&P 500 Quanto USD/KRW Currency Adjusted Index and Eurostoxx 50 Quanto EUR/KRW Adjusted Index as new underlyings within its offering in 2020 – they were linked to 33 and 25 ELS, respectively.

The South Korean issuer also stopped marketing products linked to the shares of POSCO, a South Korean steel-making company, which was linked to 23 ELS in 2019. Meanwhile, the Eurostoxx Banks Index was first seen in 2020 and featured in five ELS.

The most favoured underlyings within ELB and DLB was the Samsung Electronics shares, which took the crown from Kospi 200 by linking to 78 ELB in 2020. The number of DLB tied to USD/KRW dropped to one from five in 2019.

SRP data also shows that the 10Y/30Y/5Y/2Y USD Constant Maturity Swap Rate (CMSR) and the 10Y/2Y KRW CMSR remained popular although the firm turned its attention to the 5Y KRW CMSR and 3Y EUR CMSR which were also introduced in 2020, via DLB structures, SRP data shows.

Click in the link to view Korea Investment & Securities’ FY20 earnings report.