DBS has continued to strengthen its balance sheet despite improving macro conditions.

DBS Group has reported a drop in net profit 33% to SG$1.01 billion (US$760m) in Q4 FY20 ended in December 2020 year-on-year (YoY) due to ‘a lower net interest margin and higher total allowances’. This brings the full-year net profit to SG$4.72 billion, down 26% YoY.

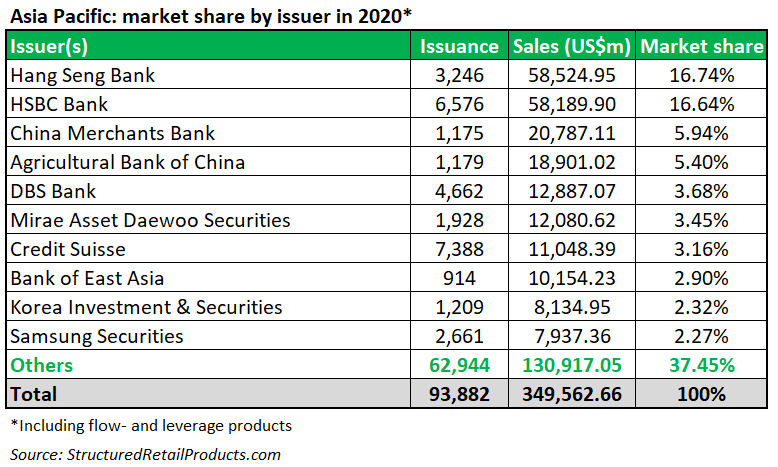

The Singaporean bank, led by DBS Group CEO Piyush Gupta (pictured), finished 2020 in the top five issuer ranking for Asia Pacific for the first time on the back of more than 4,600 products worth an estimated US$12.8 billion although most of the products were marketed in Taiwan and China. This represents a 150% increase in issuance and a 116% increase in sales year-on-year (FY2019: 1,839 products/US$5.9 billion).

DBS’ offering in 2020 was mainly focused on single stocks and baskets of shares comprising technology and transport firms such as Advanced Micro Devices (744 products/US$2 billion); Nvidia (608/US$1.6 billion); Boeing (482/US$1.3 billion); Tesla (4512/US$1.2 billion); and Amazon (390/US$1 billion).

The bank has over 4,000 live products in Taiwan worth an estimated US$9.9 billion as well as four live products in China worth an estimated US$76m, according to SRP data.

In October, DBS Private Bank relaunched a new tranche of its MSCI EM Asia ESG Leaders Outperformance Trade to capitalize on the SG$95m raised over seven tranches following the three-year call warrant debut in August 2018, SRP reported.

The private bank also relaunched dispersion strategies linked to US equities and issued call warrants tied to a bespoke index after its Global Income Note raised over SG$1 billion in three months since January 2019, Rohit Jaisingh, head of capital markets products at DBS Private Bank, told SRP last August when DBS won the Best Private Bank, South and Southeast Asia and the Best Distributor, Taiwan accolades at SRP Apac Awards 2020.

Business lines

Despite the decline, business momentum in Q4 was ‘healthy with broad-based loan growth and resilient fee income,' stated the largest Singaporean bank by assets in its quarterly report. A bright spot was seen in wealth management, which recorded an increase of 21% in fee income YoY ‘from buoyant sentiment in low-rate environment’.

However, pre-tax profit at wealth management/consumer banking fell by 34.8% to SG$852m in 2H FY20 YoY as the growth of net fee and commission income at SG$976m was offset by a 28.1% decline of net interest income, which reached SG$1.4 billion.

In the meantime, treasury markets delivered a more positive performance as their pre-tax profit soared by 2.3x to SG$410m YoY driven by net interest income, which towered by 3.4x to SG$479m.

Institutional banking remained the largest contributor among the three main divisions by deriving pre-tax net profit of SG$1.2 billion in 2H FY20 despite a 33.2% decline YoY.

At the bank level, net interest income was down six percent to SG$9.1 billion in 2020 YoY as ‘as a 27bps fall in net interest margin was partially offset by constant currency loan growth of 4%’. Net fee income was little changed at SG$3.06 billion and other non-interest income grew by 32% to SG$2.06 billion. These translated to stable total income at SG$14.6 billion.

In addition, expenses were 2% lower at SG$6.16billion in 2020 YoY, 25.6% of which was booked in Q4 FY20.

On-balance sheet, derivative assets were 80.5% higher to SG$31.1 billion while derivative liabilities were 87.9% higher to SG$32.9 billion as of the end of 2020 compared with a year ago. Off-balance sheet, financial derivatives were little changed at SG$2.1 billion.

Click in the link to read DBS Group’s Q4 FY20 report.