Hong Kong multi-issuer platform Contineo has onboarded a HK heavy weight, its first new client since it launched on the cloud in late 2020.

Contineo has announced the onboarding of the Bank of East Asia (BEA) as a new client of the new cloud-based platform released on October 2020.

The Hong Kong bank was the third biggest issuer in Hong Kong SAR in 2020 with a 4.95% market share across 625 products worth an estimated US$6 billion, and the fifth manufacturer in China with a 5.5% market share across 289 products worth US$4 billion.

The bank has over 180 live products in Hong Kong SAR including not flow and leverage, and 107 live structures in China.

The MIP led by Antoine de Charnacé (pictured), which celebrated its fifth anniversary last year, ‘facilitated’ over nine million prices across 16 different issuers for pricing and execution of 10 equity payoffs in 2020. The platform also offers market intelligence and post-trade services.

Nomura partners with FTSE Russell to launch climate index series

Nomura Securities, a subsidiary of Nomura Holdings, has partnered with FTSE Russell to launch the FTSE Nomura Climate CaRD (Carry and Roll Down) World Government Bond Index series.

The Japanese bank plans to develop financial products linked to the new index which benchmarks the FTSE Climate Risk-Adjusted WGBI (World Government Bond Index), an index tracking the performance of global government bonds (currently 22 countries) in the FTSE WGBI Index while reducing exposure to climate change risk.

The index matches the duration and market value weight of each country to the benchmark and invests in government bond portfolios that offer the highest carry and roll down. Portfolios are constructed monthly to maximise both government bond carry (yield) and roll-down returns (returns that arise from shortening bond maturity and rolling down the positive yield curve).

The index has been designed to mitigate against climate risk and deliver enhanced returns while meeting the objectives of the ESG benchmark.

ESG investing in bonds is primarily focused on the corporate bond market, which accounts for only about 15% of the global bond market. By allowing for ESG investment in the government bond market, which makes up more than half of the global bond market, the index offers higher expected returns and a potential new solution for ESG investment.

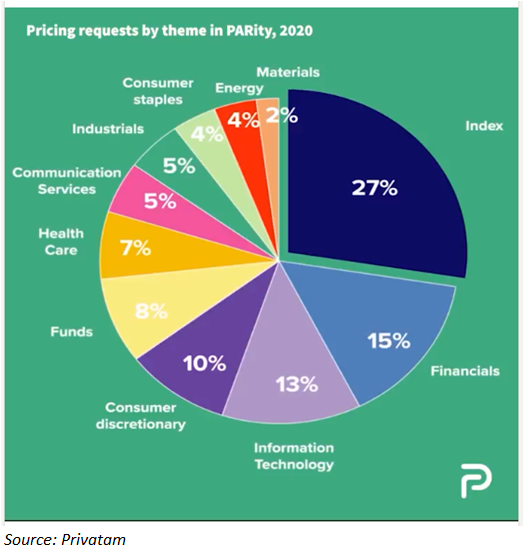

Privatam’s Parity unveils most popular trades in 2020

Monaco-based wealthtech provider Privatam has unveiled the three most popular themes priced in its Parity platform in 2020. According to the firm 27% of the pricing requests related to indices followed by financial stocks with 15% of the pricing requests, and technology shares with 13% of the requests for quote.

Privatam updated its platform in late 2020 to offer wealth managers new functionalities such as a coupon barometer that notifies when target sectors and stocks are warming up; a consolidated portfolio providing visibility to portfolio cashflow and exposure analysis; and document generation for wealth managers to download reporting PDFs.

The firm also announced a partnership with Seba Bank which becomes the preferred partner to extend their product offering on digital assets. The Swiss digital bank launched in mid-2020 the yield enhancement product issued by SEBA Bank, the first dual currency certificate on BTC/USD that sells put options on BTC/USD.

Delta Capita deploys legal AI technology as Libor switch looms

Technology consultant and managed services provider Delta Capita has adopted AI technology from Luminance, an artificial intelligence platform for the legal profession, to assist them with Libor, Ibor and Euribor transition projects.

Delta Capital will deploy Luminance’s machine learning technology to ‘better understand risk exposure across their contracts and thus mitigate the impact of the transition’.

Luminance uses supervised and unsupervised machine learning to read and form an understanding of legal data, to instantly identify key datapoints, clauses and anomalies in contracts.

Libor, which is estimated to be embedded in up to $340 trillion worth of financial contracts worldwide, is the most widely used benchmark for short-term interest rates. However, its impending demise has generated calls to action across the global banking and finance industry as institutions are faced with the complex and arduous task of reviewing and remediating contracts tied to the Libor rate.

The SRP database lists more than 1,450 live products linked to Ibors (across 25 different jurisdictions). However, as recently reported, implementing the fallbacks might not be straightforward for all of them.

S&P DJI expands global ESG suite

S&P Dow Jones Indices (S&P DJI) has expanded its S&P ESG Index family with two new additions - the S&P MidCap 400 ESG Index and the S&P SmallCap 600 ESG Index.

The new indices have been designed to replicate the risk and return profile of their underlying benchmarks, the S&P MidCap 400 and the S&P SmallCap 600, while providing a significant boost in ESG score performance. Together with the existing S&P 500 ESG Index, S&P DJI now offers ESG versions of its three headline US equity indices that combine to form the S&P 1500 Composite covering 90% of US market capitalization.

The new ESG benchmarks come as investor interest in ESG products continues to soar, according to S&P DJI.

In 2020, assets under management (AUMs) tied to ESG ETFs nearly tripled from just under US$60 billion to more than US$170 billion, with flows of US$81 billion according to data compiled by S&P DJI. Mid-cap and small-cap ESG ETFs grew even faster with AUMs increasing by more than 260 percent in 2020.

There are 41 live structured products linked to the S&P 500 ESG with an estimated value of US$34m, whilst the S&P MidCap 400 Index is featured across 162 live structures worth an estimated US$515m, according to SRP data.