Bank of Montreal and Royal Bank of Canada have seen their structured product issuance during the third quarter of 2020 falling.

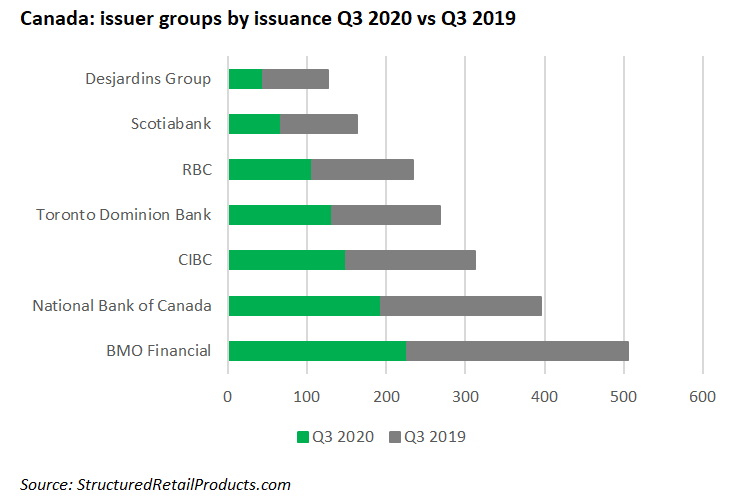

BMO Financial continues to dominate the Canadian structured products market in the third quarter of 2020 with an issuance of 226 products, according to SRP data. This represents a an 18% decrease from 2019’s figure of 279 products.

The bank, led by chief executive Darryl White (pictured), reported a net income of US$1,58 billion during its fourth quarter (third calendar quarter), representing a 33% jump from the same period a year ago and an adjusted net income of US$1,61 billion, up US$3m from 2019.

The bank’s capital markets segment reported a net income of US$379m, reflecting a 40% increase to US$108m from the prior year, while the wealth management arm boosted its net income by 20%.

Risk-weighted assets (RWAs) stand at CAD336 billion (US$259 billion), an increase from the same period of 2019 though a slight drop from the previous quarter’s figure of CAD337.4 billion.

BMO has 3,372 live products in the SRP database that are domestically listed and wrapped as capital-at-risk notes (2,912/US$3.1 billion), GICs (317/US$1.6 billion), and PPNs (143/US$235.8m). The bank’s favoured underlyings are stocks including CIBC, Bank of Nova Scotia, Enbridge, Manulife Financial, and Power Corporation of Canada, with index-linked structures using indices such as the Eurostoxx 50 are marginal.

Royal Bank of Canada has suffered an 11% plummet in reported net income totalling CAD11.4 billion in the current quarter, and has slid from fourth to fifth place in 2020 from a year prior with 106 products, signifying a 23% tumble.

The bank has 23 live institutionally listed structured products, according to SRP data. The investments are wrapped as notes (13/CAD457.9m), and warrants (10/CAD3.7m) while some underlyings are 2Y USD Constant Maturity Swap Rate, Eurostoxx 50, and 30Y USD Constant Maturity Swap Rate.

The bank reported a higher PCL of CAD 2.5 billion from the prior year, driven by reserves following the challenges brought on by the Covid-19 pandemic as well as the impact of lower interest rates.

RBC also faced setbacks in personal & commercial banking (-21% in earnings) and wealth management (-15%) which were partially offset by robust earnings in capital markets (four percent), as well as higher results in investor & treasury services and insurance (13%).

National Bank of Canada has remained firm as second most prolific issuer group with 194 products compared with 202 in 2019. CIBC has risen to occupy the third ranking on the league tables with 149 products representing a 16% increase from 2019.

Toronto Dominion Bank sits in fourth place after decreasing its issuance to 131 products in 2020 from 163 a year prior.