Sales of structured products during the period surrounding the market crash of mid-March were down 26% compared to the same period of 2019. We look at issuance and sales volumes across markets in the immediate aftermath to assess the impact of the recent market turbulence.

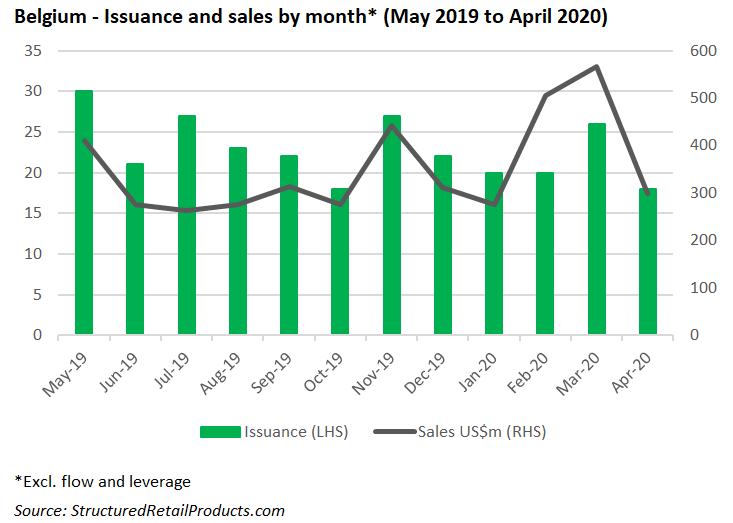

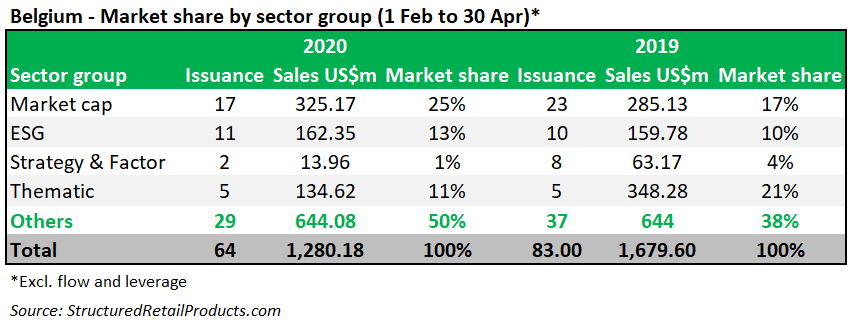

Sixty-one structured products with estimated sales of US$1.3 billion had strike dates in Belgium between 1 February and 30 April 2020, a decrease – both in issuance and sales volume – from the 83 structures worth US$1.7 billion that struck in the same period last year.

At the start of 2020, the Belgian market flourished, with sales for products striking in March, at US$543m, at their highest levels in over a year. Then the financial markets collapsed spectacularly: in April sales had almost halved to US$267m.

“What made this crisis so spectacular is the unprecedented speed at which the full society came to an emergency stop,” said Bart Abeloos, investment expert, Crelan. “As soon as the lockdown measures took effect, sectors that are built on social contact, such as catering, tourism and retail, fell completely silent. There are holes in production chains. Consumers are severely limited in their options to spend money, and for many, there is much less to spend, due to temporary unemployment or temporary closure of the business.”

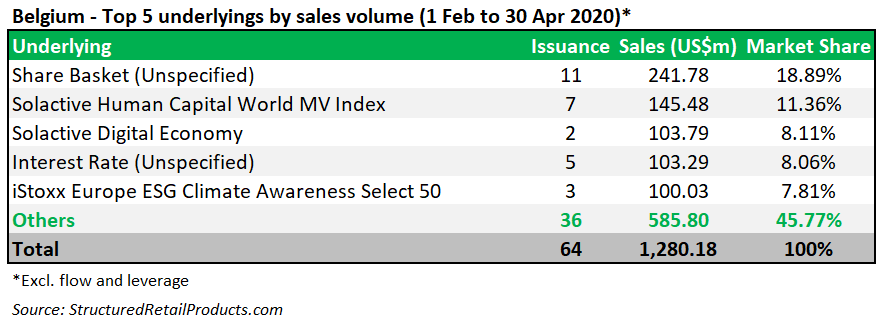

Products linked to baskets of shares ranked in first place both in terms of issuance and in terms of sales volume during the February-April 2020, mainly due to KBC’s preference to issue structured funds and life-insurance (Class 23) products linked to baskets comprising 30 stocks.

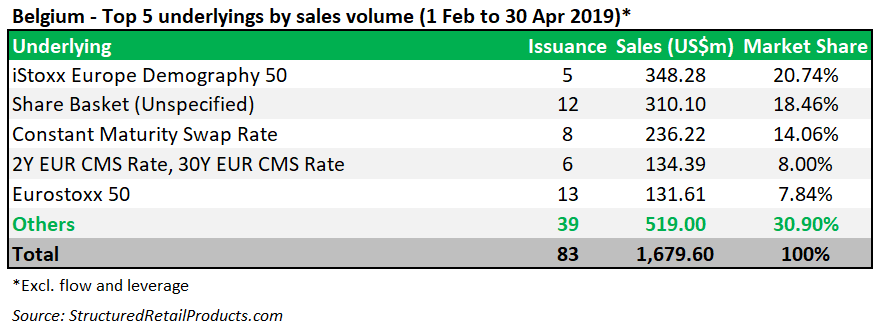

In February to -April 2019, most products by issuance were either linked to the Eurostoxx 50 (13 products) or a basket of shares (12). The highest sales volume (US$307.2m) during this period was collected from five products linked to the iStoxx Europe Demography 50 – an index derived from the Stoxx Europe 600 Index, based on a first-of-its-kind concept that focuses on seven industries that will be impacted by demographic changes, which pay high dividends and display low volatility.

‘We remain cautious about equities and opt for defensive sectors, such as food producers and companies that make a positive contribution to life in lockdown – medical technology, e-commerce, media, software, and so on,’ said Dirk Thiels, senior investment strategist at KBC Asset Management.

During the period analysed, 18 products were tied to market cap indices with a further 11 linked to indices with an ESG theme, compared to 23 and 10, respectively, in the same period last year. A new entrant in the country’s top five underlying ranking was the Solactive Human Capital World MV Index which gathered US$142.98m from seven products. The index, which did not appear in February to April 2019, is designed to track the performance of developed markets companies with a comparably high dividend yield and, at the same time, construct a portfolio which exhibits low volatility and avoids excesses sector concentration.

As a sector, Europe (US$177m from 10 products), ESG (US$176m from 11 products), megatrends (US$112m from three products), and demographics (US$71m from two products) stood out in Feb-Apr 2020 whilst in the same period in 2019, demographics (US$348m from five products) was the dominant sector.

Healthcare is logically at the centre of all attention at the moment - David Ghezal, Deutsche Bank

In the current turbulent market environment, it is more than ever necessary to be selective in your investment choices, according to David Ghezal, investment strategist at Deutsche Bank Belgium. He believes that there are two sectors that investors should be keeping an eye on: healthcare and technology.

“Healthcare is logically at the centre of all attention at the moment due to the race against time in the search for a cure and a vaccine against the coronavirus,” said Ghezal, adding that the sector also has many other catalysts that go beyond the current crisis. “In particular, the aging of the population and the structural increase in health expenditure as a result of this demographic development are an important supporting factor.”

In 2019, Société Générale collaborated with Beobank for the launch of Autocallable Solactive Silver Age 2028, which is responding to the ‘ageing’ theme by linking its return to the Solactive Silver Age Index.

“For its part, the technology sector has been able to surprise positively since 1 January 2020 due to its outperformance. The sector also emerges as one of the main beneficiaries of a recovery in economic activity in the medium and long term,” Ghezal concluded.

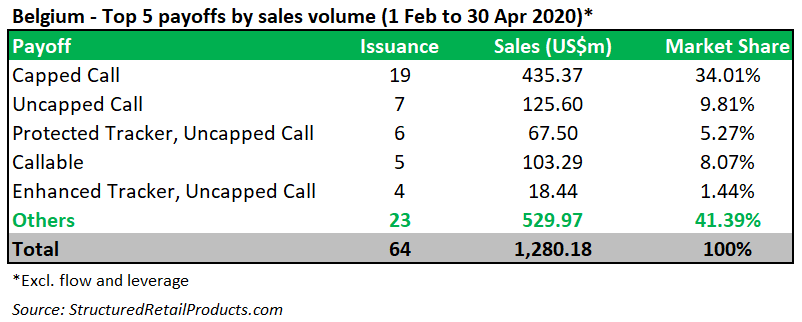

Products offering capped participation in the upside of the underlying remain the preferable choice in the Belgium market, gathering US$381.34m and another US$86.8m by products also featuring the lookback mechanism to capitalise on the recent market volatility.

Seven uncapped calls collected a combined US$111.09m. In 2019, this payoff was predominately used in combination with other features, such as callable and knock out. Products that can be autocalled do not rank among the top five in 2020.

According to SRP data, underlying sector groups have not significantly changed for Belgium since last year. Market cap takes the lead again in 2020 both in terms of issuance and sales volume. The ESG sector, which has been a popular driver of activity for some time now, has also maintained its position with issuance of eleven products in 2020 compare to ten in 2019.

The investment horizon has not been affected so far either by the recent market crash with long-term products remaining the most popular choice in 2020. Similarly, short-term product are barely issued in the Belgian market with five with sales of US$59.83 issued in 2020 and four worth US$60.12m in 2019.

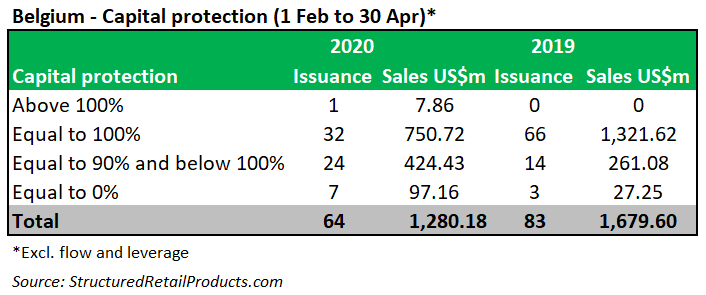

Fully capital-protected products continue to lead the way in Belgium in February to April 2020 with 30 products, which have a combined volume of US$626.66023. What has changed from the same period in 2019 is an increase in the issuance of partially protected products, which have become more popular in 2020.

GFC

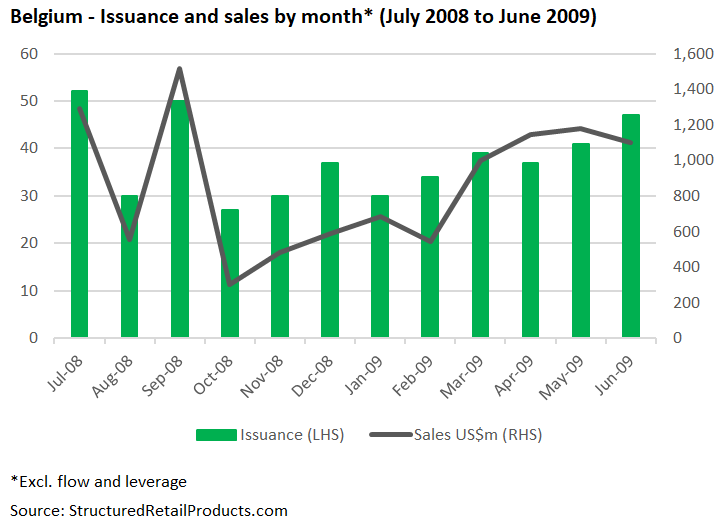

Although it is too early to compare the effect of the Covid-19 crisis on the Belgian structured products market with the impact of the Lehman collapse, and the resulting global financial crisis (GFC) in 2008, some similarities can be observed. Back then, there were 45 different distributors active in the market, which had a size of US$18.3 billion, from 584 products (for comparison, 19 distributors collected US$4.5 billion from 287 products in 2019).

However, just like today, the immediate aftermath after the Lehman collapse on 15 September 2008 (the day Lehman filed for bankruptcy) saw sales volumes drop to alarming levels – from US$1.5 billion in September to just US$299m in October 2008. Even though sales and issuance of structured products slightly increased during the following months, the market never really recovered and annual volumes soon slipped below the US$10 billion mark, not helped either by the introduction of a moratorium on complex structured products that was introduced by the Belgian Financial Services & Markets Authority (FSMA) in July 2011.

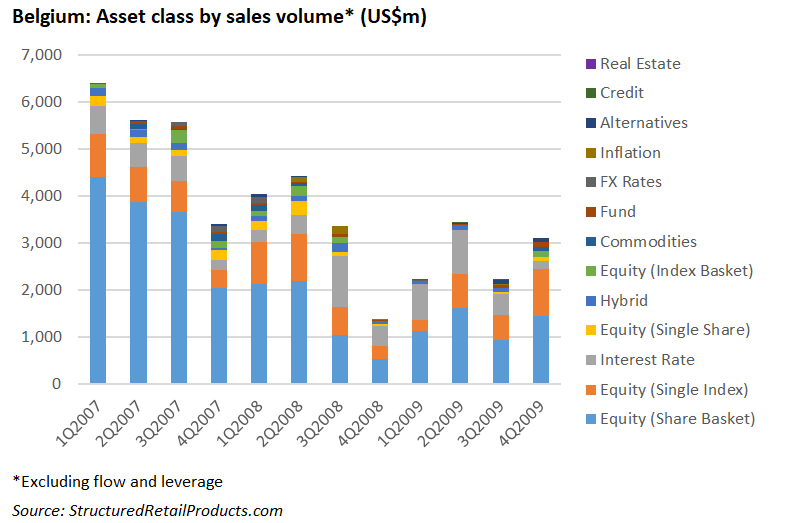

As shown by SRP data, soon after Lehman, investors appetite shifted from products linked to a basket of shares, to products on single indices, such as the Eurostoxx 50 and Stoxx Europe 600 Healthcare, while the demand for structures tied to the interest rates also increased. One such product was ING Bank’s Callable Fix Note 3.75%, which sold €75.06m (US$83.3m) at inception.

Even pre-moratorium, capital-protected products dominated proceedings, although investors were prepared to take more risk those days, with 30% of the 1,715 products that were issued between 1 January 2007 and 31 December 2009 putting full capital at risk.

The biggest difference between then and now can be seen in the tenor of products. Whereas nowadays – due to the low continuing low interest rates – the vast majority of products has a duration of more than six years, with 10-year structures certainly no exception, in 2008 the bulk of sales volumes (US$11 billion out of a total of US$18.3 billion) was collected by products with a term of between three and six years.