In the face of market volatility and growing speculation that a recession could be coming, investors in Hong Kong are fleeing stock markets – except for those funnelling cash into warrants and callable bull/bear contracts (CBBCs).

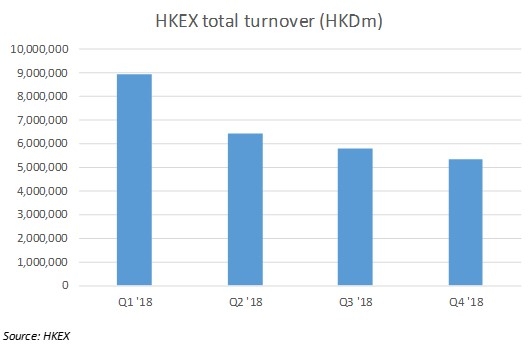

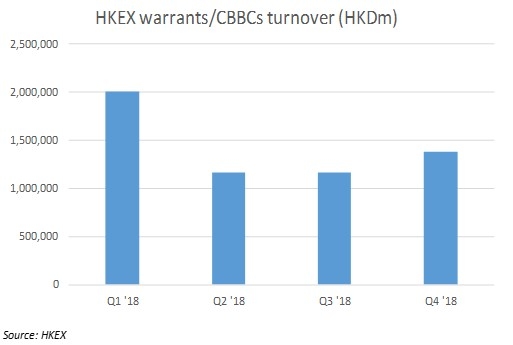

The combined turnover of warrants and CBBCs listed on the Hong Kong Exchange (HKEx) in Q4 of last year rose almost 20% from the previous quarter to roughly HKD1.4 trillion, according to data from the Hong Kong bourse. The rise came despite an 8% quarter-on-quarter drop in the exchange’s overall turnover in the last three months of 2018 to HKD5.3 trillion.

Keith Chan (pictured), head of cross asset listed distribution for Apac at Societe Generale, told SRP that it was volatility – which attracts more short-term trading – that contributed to the surge.

“In rangy markets like what we experienced in Q2 and Q3 2018, warrants and CBBCs are much less favoured and hence, the inactivity,” he said.

The increased activity among investors was driven more by CBBCs than warrants. The Q4 turnover of the callable product soared nearly 40% from Q3, while that for warrants rose only 10%.

“Last year Hang Seng Index came down to 26,000 from its 33,000 level, so demand over index and single-stock CBBCs, especially Tencent, increased,” said a banker in the equity derivatives sales team at a European bank in Hong Kong. “CBBCs kept knocking out and so, issuers had to keep on issuing new products and provide market with enough supply.”

Unlike warrants, CBBCs must be terminated early when the price of the underlying asset hits the call price. The product is also more responsive to the price movement of its underlying assets. Warrants, on the other hand, are vanilla options which pricing is affected by the implied volatility – the estimated movements of a security’s price. Implied volatility generally increases when the market is bearish.

“Given that the implied volatility [IV] is now at a relatively high level, investors are advised to remain cautious to avoid risks of long holding warrants,” said Chan. “If IV falls, both call and put option value will decline.”

The one-year at-the-money-forward implied volatility of S&P 500, for example, rose more than 20% last year given the very low base at the start of 2018, according a recent BNP Paribas report on Asia equity and derivative strategy. The S&P 500 tends to be the biggest barometer for volatility.

Bears gain momentum

The uncertain market conditions also pushed up trading volumes for bear contracts which most individual investors feel uncomfortable trading. With both warrants and CBBCs, investors can bet on either market direction.

“In Q3 and Q4, there were more activities trading bears – it’s a sign that shows investors are more mature because usually for retails – they are very good at call, bull and going long,” said Chan. “In the last few years, you will see, especially on the Hang Seng Index, that people are trading both bulls and bears. They understand more about the risk.”

Despite the inherent complexity of derivatives, warrants and CBBCs are both popular investment outlets for the so-called mom-and-pop traders in Hong Kong, partially explaining why Tencent and Hang Seng Index are the two most widely cited underlyings. Together, they represent about the half of the market activities. Retail investors in Hong Kong also generally hold short-term views on the underlying that are hours or even minutes-based.

Societe Generale expects the CBBC market in Hong Kong to remain active this year, forecasting the turnover of the listed product to hit a new high of HKD2 trillion with the number of CBBCs in circulation in the first quarter reaching 8,000.