Warrants and callable cull-bear contracts (CBBCs) on the Hong Kong Exchange (HKEx), a market which SRP recently started covering, saw a largely quiet month, with warrants turnover climbing 2% month-on-month to HK$179bn (US$23bn), while CBBCs trade was down 27% to HK$78bn.

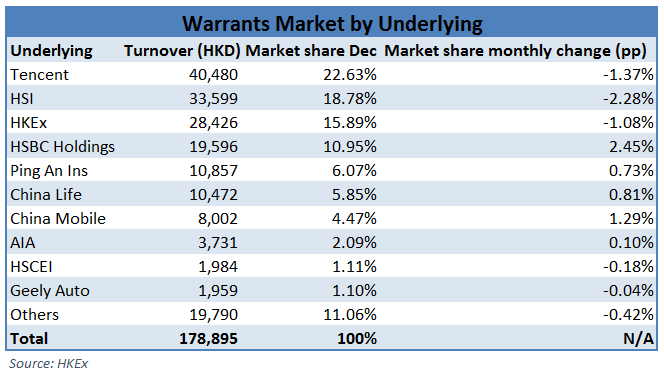

Investor preferences remained broadly unchanged from last month, with Tencent, HSI, HKEx and a number of other household HK-listed names driving the majority of warrants trading activity.

HSI took up 22% of overall warrants net notional flow of 2016, up from the average of 17% in the previous three years according to Cedric Cheung (pictured), executive director, head of listed structured products sales, Asia at JP Morgan. "A similar trend is seen in CBBCs (HSI traditionally takes up around 95% of the net notional flow) where the flow in single stocks declined from 5.3% in 2014 and 4.3% in 2015 to 3.7% in 2016, said Cheung. "It is likely an indication that the retail investors have been hesitating in stock picking."

The expectation of Trump's policy has triggered sector rotation to reflation beneficiary stocks in the past two months, Cheung said. "Together with the possibilities of increase in southbound flow on Hong Kong small caps [in the context of the recently launched Shenzhen-Hong Kong stock connect], warrants demand may shift from index to stocks underlyings," he said.

Notably, the strength of the US dollar in the aftermath of Trump's victory and its impact on Japan equities, whose performance is strongly inversely correlated to the moves in USD/JPY, presents an opportunity for Hong Kong investors, according to Cheung. "Most of the Hong Kong investors, when investing on equities, are insensitive to the move in currencies since HKD is pegged to USD," said Cheung. "However, the significant increase in the directional movement of USD/JPY presents an opportunity for Hong Kong investors to capture through Nikkei 225 Warrants listed in Hong Kong," he said.

"While markets are expecting an increased level of geopolitical risk and increased policy-related uncertainty in 2017, market volatility remains contained," said Cheung, noting that the divergence between market volatility (as measured by VIX) and political uncertainty (as measured by EPU index) has reached record levels.

"The VHSI (Hong Kong volatility index) is trending down to a 21-month low," Cheung said. "Is the market too complacent to prepare for the uncertainty in 2017? If the implied volatility picks up from the current low level, warrants buyers will benefit."

According to market data collated by JPMorgan, the ratio of net inflow on HSI CBBCs vs. HSI Warrants has increased in the past 3 years: 3.1 in 2014, 3.5 in 2015 and 4.8 in 2016. It indicates that investors may prefer the delta-close-to-one HSI CBBCs over HSI Warrants amid the downward trend of implied volatility. "In face of greater geopolitical risk and policy risk in the coming months in 2017, together with a less likelihood of further monetary expansionary policy, the implied volatility may pick up and we will see more opportunities in HSI Warrants again," said Cheung.

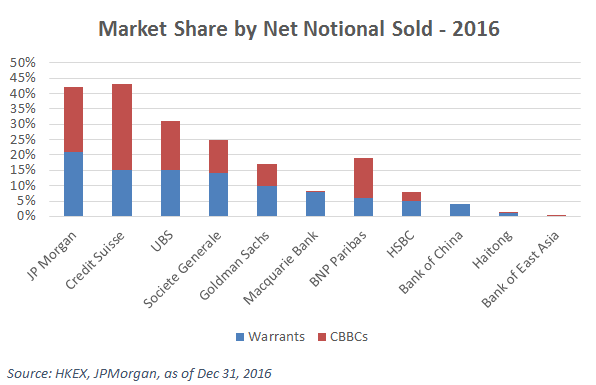

In terms of issuers, turnover remained largely unchanged, with UBS, JP Morgan and Credit Suisse accounting for 73% of CBBCs trade, and 73% of warrants trade. The three banks were also in the lead in terms of notional sold for last year.

Meanwhile, structured warrants turnover on the Singapore Exchange (SGX) surged in December, with traded volume more than doubling month-on-month to over S$1.2bn (US$0.83bn), an average daily figure of nearly $60m.

Amundi launches first-of-kind protected fund in Hong Kong

HKEx expands L&I products' pool of eligible underlyings, rolls-out 2017 roadmap