Volatility is no longer a measure of uncertainty, according to Antoine Porcheret (pictured), senior equity & derivative strategist analyst at BNP Paribas. In financial markets dominated by the actions of central banks, Porcheret suggests that volatility convexity is now the preferred measure for uncertainty, with a rise after August likely to be sustained, if you observe this indicator.

Defined as the indicator of the price for the volatility of tails (or the price that investors are willing to pay to hedge against extreme events), volatility convexity has been grinding higher for a year, and has remained at highs this summer, despite the fall in implied volatility.

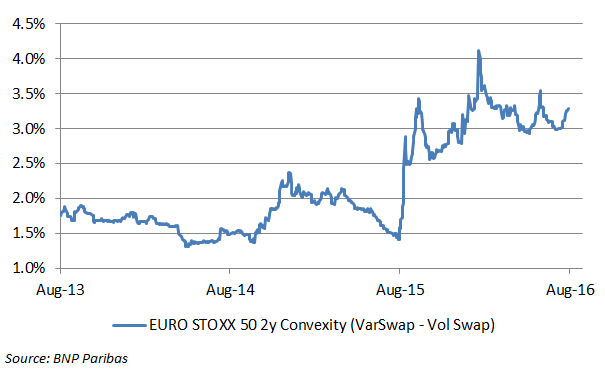

"Since August 2015, we have had a dislocation between at-the-money volatility - ie. the volatility of the body of Eurostoxx 50 returns distribution - remaining low, and the volatility of the wings - covering the tail events - exploding," said Porcheret. "This dislocation gives a sensible picture of how investors assess the 'central banks are omnipotent' narrative that has been driving capital markets since the financial crisis."

While confidence in the ability of central banks to suppress the body of risk holds true, at least for now, the same cannot be said for their ability to manage rail risk. "Until a year ago, investors' viewed monetary authorities as able to inflate assets and suppress all market risks (at-the-money plus wings, ie. body plus tails)," said Porcheret. "But the narrative evolved and switched to 'central banks will step in every time volatility spikes (think of a whack-a-mole game), but they are not really able to suppress tail risks'."

The change came with two events: the flash crash that followed a China devaluation that saw the European benchmark fall 9% and the S&P 500 by 7%, which demonstrated that, while massive injections of liquidity can control the body of your distribution, they cannot prevent crashes. A few weeks later the US Federal Reserve chose not to hike rates and Janet Yellen, chair of the board of governors at the central bank gave the impression she was not sure of what she was doing. "We experienced a negative inflection point in the way investors buy the 'central banks are omnipotent' narrative, as they realised that not only tails have not been suppressed, but they have thickened," said Porcheret. "The confidence in central banks suppressing the body is still intact (for now), but the confidence in managing the tails has vanished." And then convexity surged.

Only a major change in the way investors see the impact on financial markets of central banks - such as the one experienced last summer - could trigger a reversal in volatility complexity, according to BNP Paribas. "Since 2008 and the start of quantitative easing by the Fed, the distribution of returns has displayed a higher peak," said Porcheret.

Subdued volatility levels have affected long volatility positions, hit by adverse carry and remarking, according to the French bank. The carry for European indices deteriorated rapidly following Brexit: Eurostoxx 50 volatility in July was 17.5%, which triggered a large downward remarking in its three-month implied volatility, from 25% to 20%, noted the French bank. August was no different, with realised vol slipping to 15% and implied vol hitting a one-year low, at 17.9%. The spread between Eurostoxx 50 one-month realised and volatility and prior month three-month implied volatility now stands at minus-6%, according the bank.

Short-term implied volatilities will grind slightly higher over the next two weeks, as investors position themselves ahead of the fourth quarter of the year, according to Porcheret. The expected pick up in volatility in September has to do with both seasonality and current volatility levels. "Firstly, investors usually do not carry large long volatility positions during the summer, as they think people go on holidays and markets are quieter," said Porcheret. "Second, as volatility has reached record lows, demand for positioning should intensify as soon as next week and the week after."

The Vix and Eurostoxx Volatility Index closed respectively at 12.27 and 21.66 on August 22, while the fourth quarter holds the prospect of an Italian banking crisis that has still to be solved, US elections in November, an Italian referendum in October, an assessment of Brexit consequences to assess, and the almost inevitable unknowns.

Volatility I: Preparing for the post-summer rise

That Was The Week: When being even shorter is good

S&P 500 warrants to get traction on SGX as US volatility spikes, Macquarie

As far as European regulators are concerned volatility is the measure of risk, IDAD

Investors understand volatility, but it would be nice if they understood it more, SRP Americas