The Korean issuer is expanding its warrant business to Indonesia.

Korea Investment and Sekuritas Indonesia (KIS Indonesia) has listed 19 call warrants on the Indonesia Stock Exchange for retail investors to trade after its product debut in the market on 2 July.

Structured warrants were technically the first type of active derivative product in the Indonesian market - Jangwon Seo

The 19 single-stock call warrants issued by the Indonesian entity of one of the largest Korean securities houses track a total of 18 underlying stocks with a focus on the banking, mining, and oil & gas sectors including local integrated energy company Barito Pacific (two products), coal mining company Adaro Energy, and Bank Negara Indonesia (one product each).

The Korean house submitted the issuer licence in September 2023 and gained approval from the exchange in June, Jangwon Seo (pictured), head of global derivatives at Korea Investment & Securities Asia, told SRP.

Structured warrants first appeared on the Indonesia Stock Exchange in September 2022. Their overall average daily turnover to the cash market has remained nascent two years into the market, accounting for only 0.03%, Seo said, compared to a more mature market like Hong Kong SAR with over two decades of such operation where the figure stands at 10%.

Our strategy right now is to focus on growing the pie bigger to expand the structured warrant’s market size - Jangwon Seo

“Structured warrants were technically the first type of active derivative product in the Indonesian market, and it might lead further on to open up the listed option market, the single stock futures market, or other type of derivatives markets,” he said. “Our strategy right now is to focus on growing the pie bigger to expand the structured warrant’s market size,” he said.

There are currently three traders and one marketer working on warrants at KIS Indonesia, according to Seo. Indonesian structured warrants’ average daily turnover amounts to around US$200,000, he noted, and these products are hedged through the respective underlying stocks.

With the new listing, KIS Indonesia becomes one of five active issuers in Indonesia’s structured warrant market. Its entrance came after RHB Sekuritas Indonesia, a subsidiary of Malaysia’s RHB Bank, listed the first batch of structured warrants in the market in September 2022, followed by Maybank in February 2023, CGS International this February, and KGI this past July. As of 22 August, there are 150 live call warrants in the market.

“Comprehensive experience” is the Korean issuer’s edge in the competitive market against the other four issuers, Seo described.

Its foray into Indonesia comes after it successfully listed structured warrants in several markets, including its home market, Vietnam, in 2019, and Hong Kong SAR, which listed its first batch last December.

According to Seo, in Q1 2024, KIS Korea captured nearly 93% of the market share for equity-linked warrants (ELW) – equivalent to derivative warrants in Hong Kong SAR – in its domestic market, while KIS Vietnam, the offshore entity, was one of the top two issuers of covered warrants listed in the local market.

In Hong Kong’s derivative warrant markets, the Korean issuer's average daily turnover reached HK$108.5m (US$13.9m) as of 14 August, up 89% compared to the first quarter (HK$57.4m) and an increase of seven percent compared to the second quarter (HK$101.6m). The latest average daily turnover figure translated into 2.6% of the market share.

Compared to Hong Kong SAR’s three trading day product listing cycle following the launch, Seo said the listing cycle in Indonesia is longer. It currently takes on average around two weeks to be available for trading following the launch. However, issuers have the flexibility to adjust the warrants’ final strike level before the listing.

In addition to this latest warrant listing, Seo said KIS Indonesia is also looking to bring in some diversification to the market by listing some longer-tenor products of nearly 10 months and some with over one-year tenors in mid-September compared to four-month tenor products in the existing market pool. The new listing will comprise 30 new products.

Despite the nascent market size at this current stage, Seo remains hopeful about the Indonesian market’s potential, considering the country’s large population and the fact that “its cash market is twice as big as Vietnam’s cash market”.

Steady growth in Hong Kong

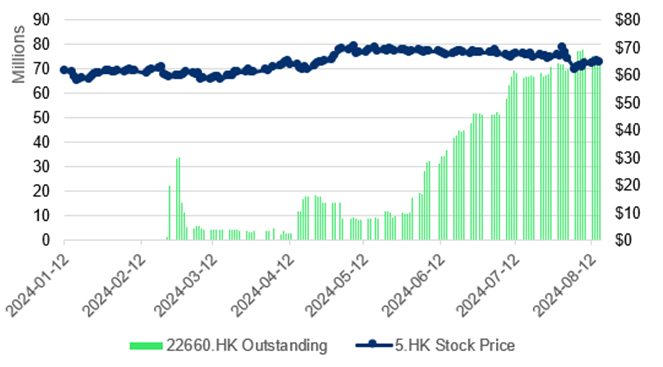

In Hong Kong SAR, some 83 KIS Asia-issued derivative warrants across 34 underlyings have been listed on the HKEX as of 22 August. Out of 83 products, eight of these have a tenor of nearly five years with an expiration date of 2028, tracking popular underlying like HSBC, China Mobile, and Tencent.

“Our five-year HSBC call warrant drew significant investor interest, becoming a top seller and driving a trend among other issuers to offer similar long-dated warrants,” he said.

KIS Asia: outstanding of HSBC-linked 2028 expiry call derivative warrants*

*Data as of 16 August

Source: Korea Investment & Securities Asia

Speaking of the broader trends, Seo noted that as of 15 August, the month has been quiet with no significant flows from those warrants tracking big corporate names such as Alibaba and Tencent despite the earnings season.

“On the contrary, we noticed some flows on second-tier names such as Anhui Conch Cement, China Tourism Group Duty Free, and underperforming names such as Galaxy Entertainment,” he said.

When asked about its plan to list CBBCs, Seo said the issuer is taking a “cautious approach” to product issuance given the current weak market sentiment.

“We are preparing index warrants first before entering the CBBC market. However, CBBCs will be a key part of our strategy if we see a positive shift in the overall market,” he added.

Do you have a confidential story, tip or comment you’d like to share? Write to jocelyn.yang@derivia.com