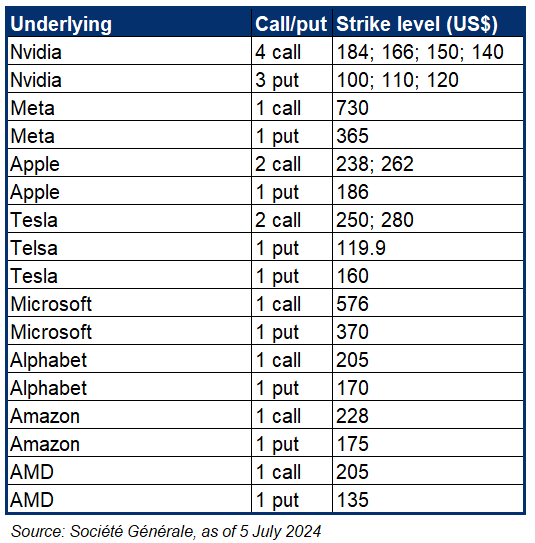

With the listing on Friday, the French bank's range includes over 20 derivative warrants tracking Magnificent Seven stocks as well as Advanced Micro Devices (AMD).

US equities can’t stop and won’t stop rallying and if they do, investors can always play the downside as Société Générale (SG) taps into single stock trends to cater to Hong Kong retail investors’ needs in the listed structured product space.

Derivative warrants on US single stocks play an important role for retail investors - Keith Chan, Société Générale

The French bank has listed 23 derivative warrants (DWs) tracking US single stocks on the Hong Kong Exchanges and Clearing (HKEX) since 25 June.

The Friday (4 July) listing consists of eight US stock underlyings: the Magnificent Seven – Apple, Amazon, Google’s parent company Alphabet, Meta, Microsoft, Nvidia, and Tesla – and the stock of chipmaker AMD.

Société Générale started preparing for the listing last year as it looked to diversify its offering which coincided with the timing of yet another US equities bull run and the troubles of Hong Kong equities, according to Keith Chan (pictured), head of cross-asset listed distribution, Asia Pacific at the French bank.

Over the past two years, more Hong Kong brokers have started offering 24-hour trading on US stocks, Chan told SRP, as there is increasing demand among Asian investors to trade US stocks during the same time zone as Asia.

“Derivative warrants on US single stocks play an important role for retail investors, including those who have already held US stocks and [want to] do some risk management to hedge or to increase the exposure via call warrants,” he said.

Hedged through each respective underlying’s direct stocks or index futures, the bank rolled out 13 call warrants.

As of 4 July, the SG-NVDA@RC2412, a call warrant tracking Nvidia with a strike price at US$166 that was listed on 25 June, is the most-traded DW among products linked to US stock, with a turnover of HK$322,800 (US$41,335), data from HKEX showed.

The bank said it will list one more put warrant tracks the shares of Tesla with the strike level at US$160 next Monday.

Hong Kong’s listed structured product market currently comprises two leveraged product types: DWs and callable bull/bear contracts (CBBCs). DWs typically have a tenor between six months and five years, and implied volatility may impact their trading price. On the other hand, CBBCs usually have a built-in knock-out mechanism, and their trading price is unresponsive to implied volatility.

With the latest listing SG becomes the second issuer of US single stock-linked DWs, alongside Goldman Sachs which listed its first batch last September and has rolled out products tracking four underlyings – Apple, Microsoft, Tesla, and Nvidia – since then, according to the HKEX data.

Tight range

Speaking about broader market trends, Chan noted that June retreated to a “tight range” after the Hong Kong listed structured product market showed recovery with positive flows since April.

“The Hang Seng Index (HSI) reached this year's high in Q2, so there's a mix between bull CBBCs and bear CBBCs [tracking the index] – quite close to 50/50,” he said. “If we look at the flows, as HSI goes up, some investors would probably want to buy a bear [CBBC]. And as soon as the index breached some important levels, they might switch to bull [CBBC] again.”

Despite around 15% to 20% increase in fund inflows into Hong Kong underlying-focused derivative warrants in the second quarter compared to the first quarter, the overall Hong Kong underlying-focused product activities remained in a low range compared to the last five years, the French bank’s executive said.

The HKEX May statistics report shows that the average daily turnover for DWs and CBBCs stood at around HK$4.5 billion and HK$5.6 billion, respectively.

While seeing the growing demand for US stock underlings, Chan also spoke about the bank’s interest in continuing to develop its daily leverage certificates (DLC) market in Singapore, which first debuted in 2017 and expanded its offering to US indices underlying in 2022. There are currently 200 DLCs issued by the French bank listed on the Singapore Exchange (SGX).

“A DLC has a very similar payoff to leveraged inverse ETFs. In the US, it’s also becoming very popular where you have these 2x or 3x daily leverage instruments like TQQQ and SQQQ,” he said. “We have these products with similar payoffs in Singapore covering US indices and Hong Kong and Singapore equities.”

The bank also partnered with SGX to launch the first-ever autocallable structured certificates in Asia 12 months ago.

With the latest listing in Hong Kong, Chan sees opportunity for creating sub-strategies that complement investors' US stock portfolios.

“For example, as the stock goes up, [investors] can buy some put warrants to do some short-term hedging,” he said. “Or if [US stock] investors wanted to take short-term profit but are still worried that stock might continue to go up because of the bull market, they can sell the stocks and then use a portion of the profit to buy a call [warrant] to capture upside while freeing up some of the capital.”

“The goal for us is to build awareness of these products,” he continued. “We don't expect a lot of [these] warrants to be traded actively – it's more about holding this product for a little longer to capture some medium-term moves.”

Do you have a confidential story, tip or comment you’d like to share? Write to jocelyn.yang@derivia.com