Canada's structured products market has recorded another positive month in July, with the volume of concurrent live products as of July 31 standing at 9,318, carrying notional of C$53.4 billion (US$41 billion), and marking the 44th straight month of growth.

Despite the increase to yet another all-time high, sales last month were well on the downside on a monthly basis, with just 222 new products entering the market, compared with 323 in June, and carrying a notional of C$540m - the lowest monthly figure since mid-2016.

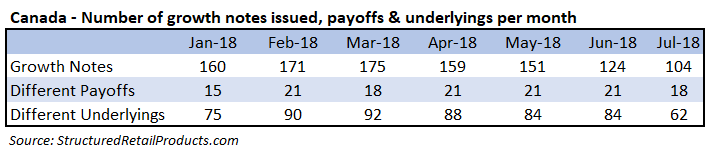

While the slowdown was quite significant, it appeared to originate mostly from fewer growth products. Excluding the more cyclical guaranteed investment certificates (GICs), 104 growth notes launched in July, down from an average of 152.6 for the previous 12 months. Historically, issuance of growth products has been more volatile than that of income products, with a coefficient of variance 0.22, as compared with 0.14 for income products, but issuance of growth products has now declined for the fourth month straight - the largest downward stretch since late 2014.

Notably, growth products appear to have become the main source of diversity in terms of underlyings on the market in Canada in recent months, with a positive correlation of 0.78, SRP data shows. This is reflected in the number of different underlyings utilized on the market, with that figure dropping in each of the past four months, from 92 in March to 62 in July. Furthermore, initial figures for issuance in August suggest that issuance of growth products could continue dropping, with the expected issuance over the first third of this month at 24, down from 35 for the first third of July.

In contrast, payoff diversity is much more resilient to the issuance of growth products, with a very low correlation of 0.16, and a steady stream of around 20 different structures entering the market in recent months. The first third of August already has 10 different structures lined up for issue, the same as the comparable period for July, despite there being nearly half as many growth products issued, and some 34% less overall.

Higher diversity, however, does not always translate into a better overall proposition to the end investor by itself, according to Abid Chaudry (pictured), managing director, head of global structured products, BMO Capital Markets.

Instead, the focus should be on "educating the client on the type of products and keeping the products simple," Chaudry said during the leading manufacturers' forum at the 7th SRP Americas Conference on May 24 in Chicago.

"We came up with all these great structures. We wanted to be funky, we wanted to show how innovative we were, but the problem was the end client didn't understand," said Chaudry. "Now we have simple products for clients that can really understand them. We want to keep it like that."

While quite low, there is a negative correlation, of -0.11, between the number of payoffs maturing and the average sales-weighted performance in recent years, SRP data shows. Significantly, a growing number of different structures will come to maturity in the coming year, with the average number of structures per month at 42, up from 28 for the past year.

A more significant correlation, however, appears between maturing and striking volumes, at a positive 0.67 for the past 12 months. Notably, as much as C$1.88 billion worth of products could mature or knock out next month, as compared with an estimated C$0.54 billion in July, SRP data shows. Furthermore, the average expected knock out coupon for the products that do have an autocall observation in August stands at 8.54%, the highest in five months and half a percentage point above the average for the past 12 months.

You can find the full Canada Market Review for July here.

Related stories:

SRP Feature (Part 2): How to define best interests, or not

US market continues to grow in the first half of 2018

Canadian regulator targets market developments and product innovations

Canada Market Review - June 2018