The recovery of the peso against the US dollar has been hugely instrumental in reviving a Mexico market that remains in decline following the election of President Donald Trump in the US, with maturities outpacing sales for the second year running, driving the outstanding volumes significantly lower. With the shock dissipating and continuous hurdles faced by the new US administration, however, the peso has recovered and now stands at levels not seen since early 2016.

The US election saw the peso plunge against the dollar late last year, causing a significant shock to the country's structured products market, according to Luis Guido, director of derivative operations and structuring at Monex Group. The consequence was unprecedented volatility, especially in the short term, which means that extreme care must be taken in the listing and closing of the dual [currency] bonds, according to Guido, speaking at the time of the vote.

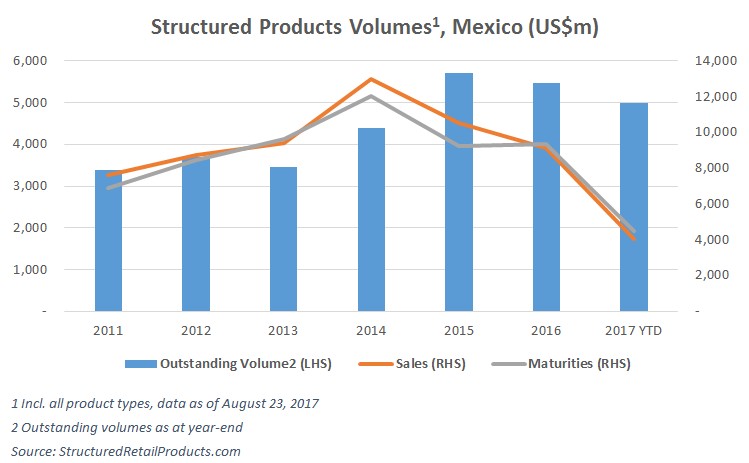

With less than 5% of tranches featuring terms of over one year, the outstanding volume at any one annual point is broadly on par or lower than the respective sales or maturities volumes.

Sales in the 2017 year-to-date as of August 23 are 36% lower on an annual basis at US$4bn. While maturities are also on the down, at $4.5bn or 27% lower on the year, the outstanding volume on the market as of August 23 stood at $5bn, 13% lower on an annual basis. Sales last month totalled $493m, down from $509m in June and $692m in July 2016, according to the SRP database. As compared with the most recent peak in 2014, sales in 2016 were down 30% to $9.1bn.

In comparison, as of August 23, the outstanding notional for the whole of North America was $528bn, up some 3% as compared with the end of 2016, and more than 11% higher from 2013.

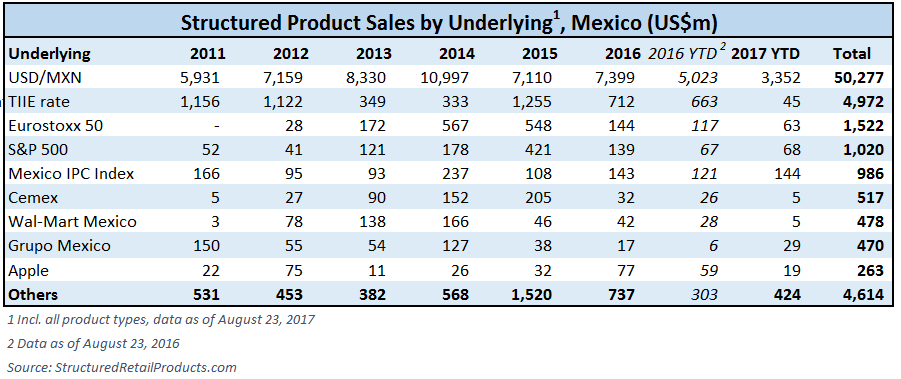

Broken down by asset class, foreign exchange, and the dollar/peso in particular, still reigns in the Mexican market, consistently attracting some 80% of sales. Notably, the Tasa de Interés Interbancaria de Equilibrio (TIIE), Mexico's interbank benchmark rate, has generated far lower sales in 2017 as compared with previous years, at just $45m as of August 23, down 93% on an annual basis.

A more significant shift has taken place in how products are wrapped, with structured bonds attracting 59% of sales so far in 2017, which compares with 87% in 2016, according to the SRP database. This has been driven by a resurgent market for certificates of deposit, which have generated sales of $1.2bn in 2017, up almost three-fold on an annual basis: CDs now account for 30% of the market, up from just under 7% in 2016. Warrants have made up most of the remaining market in recent years.

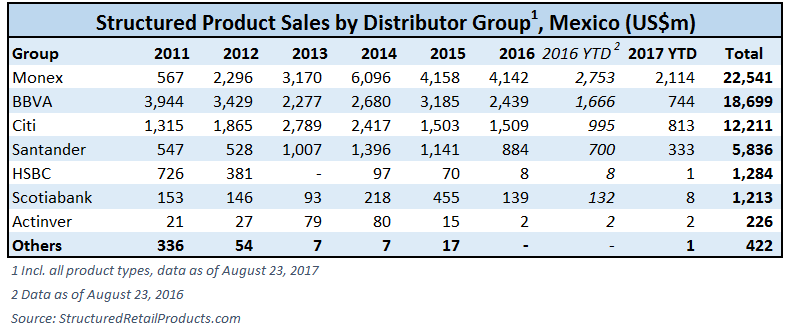

In terms of distribution networks, Monex remains firmly on top with some $2.1bn in sales so far this year, 53% of the total. This compares with 44% for the same period of 2016, going down to 26% in 2012 and just 7% in 2011. In contrast, BBVA has seen its share plummet to 19% YTD, down from 27% in 2016 YTD, and 50% in 2011. Besides the seven groups in the below table, only Banorte has sold any products in the past three years, namely the CD Range - TIIE 28 days, which launched in late June this year.

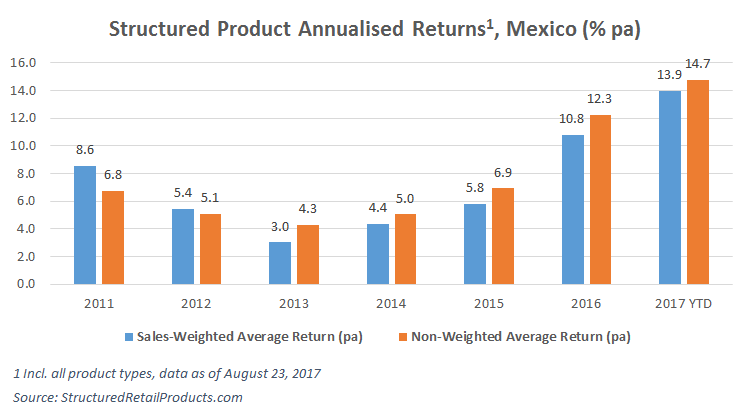

One of the most notable positive for the Mexican market in 2017, however, has been the significantly elevated levels of return generated by the industry, which is quite significant in the context of the prevailing product term being less than one year. The average pre-tax sales-weighted annualised return for products matured so far in 2017 has been 13.9%, well ahead of levels seen in recent years.

While this huge positive has yet to translate into higher sales, with a dominantly short-term product preference on the market, an upswing could come with short notice.

Picture source: download-wallpaper.net

Related stories:

Foreign exchange 2: Sales expected to increase by 50% due to new institutional clients

Trump effect on Mexico's dominant dual currency product lessened by bear trend