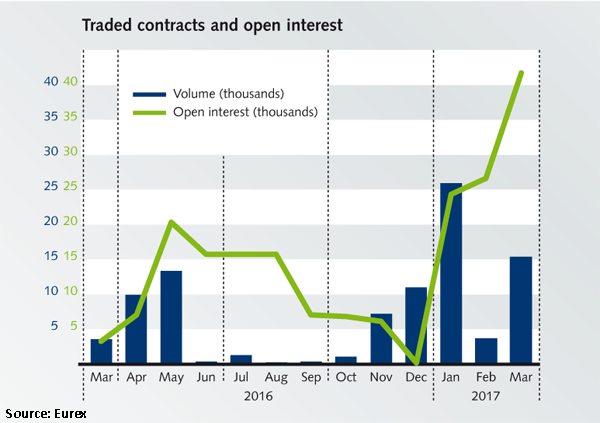

Open interest on Eurex's US dollar-denominated Quanto Futures on the Eurostoxx 50 Index, which were launched a year ago, reached a notional of US$1bn in March 2017. The Eurostoxx 50 Index Quanto Futures (FESQ) is a copy of the highly liquid Eurostoxx 50 Index Futures (FESX), with the exception that it trades in US dollars.

Structured products issuers frequently carry embedded quanto risks, according to Ralf Huesmann (pictured), senior vice president equity and index product research and development at Eurex Frankfurt. "These clients have become familiar and more comfortable with using our quanto futures as a robust, listed solution," said Huesmann. "A listed product mitigates counterparty risk and, additionally, may offer portfolio margin benefits."

Since the launch, more than 90,000 contracts have traded, corresponding to over US$2.7bn notional. In most cases, a trade in the same size in the FESX was done as a hedge, doubling the traded notional, according to a report by Huesmann. "Macro events generally drive volumes," said Huesmann. "After a good start in March 2016, activity decreased post the Brexit referendum, as the correlation, which prior to this was very negative, jumped back towards zero."

Volumes only picked up again with the US elections in November 2016, but "the market anticipates another pick up around the European elections in 2017, with French elections seen as the biggest driver," stated Huesmann,

"In the long term, we expect the first product application, ie. investing in European stocks, but avoiding exposure to the euro, to be the main driver behind the volume growth," said Huesmann. "However, the right macro environment (eg. expansionary monetary programs) and orderly liquidity are prerequisites for this growth."

According to Huesmann, another volume driver is the hedging of the 'quanto risk' done by banks via the inter-dealer market. "This is typically a market dominated by banks looking to transfer this quanto risk," said Huesmann. "An exchange-listed product like the FESQ opens up the market to investors seeking exposure to equity - FX correlation and volatility (eg. hedge funds, such as global macro funds, who might take an opposite view and want to speculate on the correlation), therefore balancing the market."

The new margin regime for non-cleared OTC traded derivatives and subsequent higher costs for banks to trade off exchange should make on-exchange listed product set up more cost effective and incentivise a shift from the OTC market, according to Huesmann. "A similar trend has been observed in the past with the dividend derivatives and is increasingly happening on Eurostoxx 50 Index Total Return Swaps and MSCI products," said Huesmann. To offer further hedging opportunities, since February 2017, Eurex introduced quarterly expiries in both FESX and FESQ out to two years (previously only nine months).

In addition, Eurex has introduced more granularity around trading in the 'quanto spread', by reducing the minimum block trade size for the FESQ and opening up the EFPI functionality to allow lower sizes to trade as a hedge in the FESX. "This means the 'quanto spread' can be entered not only in full ticks, but also in smaller price steps, as is the practice in the OTC market," said Huesmann.

In relation to product applications, Huesmann points that one of reasons to use the product is to separate equity and FX return, so investors can take positions in European markets without being exposed to the euro currency. "This is generally interesting for investors with a US dollar preference," said Huesmann. "This type of trade is particularly popular during pronounced monetary policy discrepancies, Quantitative Easing (QE) programmes and the consequent effect on equity markets and the exchange rates of the main currency pairs."

Although additional currencies could respond to market needs around options and futures, Eurex remains focused on its US quanto product. "The Quanto product in US dollars is the most active currency combination," he said. "We will focus on increasing liquidity in US dollars first, before considering additional currencies."

The other main application of the product is to hedge quanto risk of structured products, according to Huesmann. "Issuers of quanto structured products can use Eurex Quanto Futures to hedge their quanto risk," said Huesmann. "To extract the quanto spread, an issuer will typically trade FESQ against FESX in the same notional and maturity, ie. without the delta component. These structured products are often issued with longer maturities (up to 10 years), therefore FESQ hedging is done in expiries further out (eg. currently available December 2017 or December 2018)."

According to Huesmann, once the trading activity in the Eurostoxx 50 Quanto Index Futures has largely moved on exchange, Eurex could consider product extensions, offering options or futures in additional currencies.

The quanto futures update follows the approval of the US Commodity Futures Trading Commission (CFTC) which has given the green light for US investors to trade Total Return Futures linked to the EuroStoxx 50 - a move that could prove pivotal in building liquidity and cementing the Eurex-listed contracts as a viable alternative to over-the-counter equity swaps.

The instruments have already made their mark in Europe with more than 83,000 contracts traded since the December launch, representing €2.8bn notional. Volume has more than doubled in the last month as new users jumped on board, extending the market beyond the bank hedging activity that initially dominated trading. 'We have seen more buyside involvement and have been surprised to see a growing number of strategic trades such as calendar spreads,' said Stuart Heath, director of product R&D at Eurex, in a statement.

While the latest approval opens the door to the largest pool of global liquidity, the contribution of US investors to the success of European products depends on global macro views of European equity markets. Some early adoption by buyside companies has raised hopes around the long-term prospects for the product, according to Heath.

Through calendar spread trades, the contracts have enabled investors to gain exposure to implied equity repo - a measure of secured funding and a hidden parameter in any equity products including cash, futures, options and structured products, said Heath. Equity repo has suffered severe dislocations in recent years as a result of uncertainty surrounding the impact of tighter regulations, including the Basel 3 leverage ratio and net stable funding ratio, on bank balance sheets.

The new product and implied repo as an asset class in its own right represents an opportunity for US-based market players in the equity derivatives, according to Emmanuel Dray, head of equity derivative institutional sales & linear trading at BNP Paribas, which jointly developed the contracts.

Evidence from Eurex-listed VStoxx futures, which offer exposure to options-implied volatility on Eurostoxx 50, suggests that US approval can be integral for deepening liquidity in European products, said Dray. Trading in VStoxx contracts more than doubled within a year of the CFTC's 2012 approval, which opened the door for relative value trades against the CBOE's ultra-liquid Vix futures.

Relative value trades could be possible with the Eurex-listed TRF, but a rival US product offered by the CME carries a different pricing format, requiring an additional layer of calculations to trade the two instruments. The CME's Total Return Index Future linked to the S&P 500 is quoted in index points, similar to listed futures, while the Eurex TRF is more closely aligned with OTC conventions and quoted in basis points over Libor.

Related stories:

HSBC capitalises on quanto investing effect

Eurex bolsters equity index segment with new quanto instruments