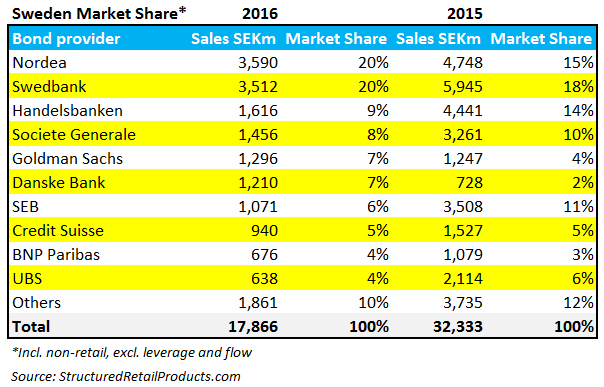

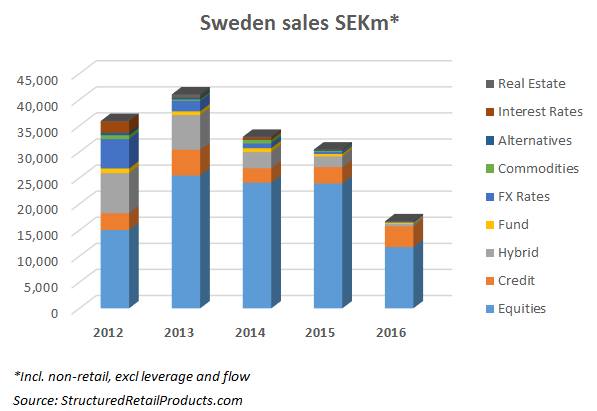

Nordea regained its position as market leader in the Swedish structured products market in 2016, by the smallest of margins, after losing out to Swedbank last year. Issuance of structured products, at 1,002 (incl. non-retail, excl. leverage and flow), was around 25% lower than in 2015, while sales volumes, at SEK16.6bn (€1.7bn), were down approximately 45%. SRP reviews the data and the financial results of the top five Nordic structured products manufacturers.

Nordea, which last topped the bond provider table in 2014, regained its position as the number one issuer in Sweden with a share of 20% of the Swedish structured products market in 2016, according to SRP data. The bank issued 80 structured products worth SEK3.6bn in 2016, against 100 products with a combined sales volume of SEK4.7bn the previous year.

Seven of Nordea's products made the top ten for best-selling products in Sweden in 2016. The list was topped by the bank's Kreditbevis USA High Yield Buffert B447, a five-year credit-linked note (CLN) linked to the Markit CDX North America High Yield index, which sold SEK406m during its subscription period.

Nordea reported total income was down 1% in local currencies (down 2% in EUR) from 2015 and operating profit was down 8% in local currencies (down 9% in EUR) from the prior year excluding non-recurring items. The bank issued approximately €2.3bn in long-term funding in the fourth quarter, excluding Danish covered bonds and subordinated notes, of which €1.5bn represented the issuance of Finnish, Swedish and Norwegian covered bonds in domestic and international markets. Nordea's long-term funding portion of total funding was 82% at the end of the fourth quarter.

"2016 was probably the most eventful year in the history of Nordea," said Casper von Koskull (pictured), president and Group CEO, Nordea, in a statement. "Continued negative rates, regulatory uncertainty and digital transformation have been in focus for the sector. The unexpected outcome of both the referendum in the UK and the US presidential elections created short term turmoil on financial markets, although it seems like investors have become accustomed to dealing with geopolitical uncertainties."

Swedbank, also with a market share of 20%, ran Nordea close, selling 134 structured products worth SEK3.5bn during the course of the year (2015: 135 products/SEK5.9bn).

Income from equity trading and structured products decreased but was partly offset by higher card and payment commissions resulting from higher volumes, according to the bank's full-year results for 2016. As of December 31, 2016, Swedbank had SEK14.9bn structured retail bonds in issue, up 3% from SEK14.6bn the previous year.

Profit for the period increased by 16% to SEK10.8bn due to higher net interest income and lower expenses and credit impairments. Net interest income increased by 10% to SEK14.7bn, mainly through higher lending volumes and mortgage margins, while net commission income decreased by 3% to SEK6.9bn.

Handelsbanken achieved a market share of 9% over the period, from 68 products worth SEK1.6bn (2015: 126 products/SEK4.4bn). Thirty of the bank's products, which, among other, were distributed via Carnegie, Erik Penser, Garantum, Skandia and Strukturinvest, were linked to a single index, including offerings linked to the OMX Stockholm 30, Solactive Global Ethical Low Volatility SEK Hedged Index and Ethical Europe Climate Care.

Handelsbanken reported assets under management (AUM) for structured products at the end of 2016 stood at SEK17bn (2015: SEK18bn). Operating profit rose by 1% to SEK20.6bn (2015: SEK20.5bn) while return on equity for total operations declined to 13.1% (2015: 13.5%). The common equity tier 1 ratio increased to 25.1% and the total capital ratio rose to 31.4%, according to the bank.

Danske Bank was the only issuer which saw both its issuance and sales volumes increase. The bank issued 65 structured products with a combined sales volume of SEK1.2bn in 2016, compared to 43 products worth SEK728m issued last year. Twenty-three of the bank's products were linked to credit including 12 products which used Stena as the underlying reference entity.

Danske Bank reported it made netting agreements with many of its counterparties concerning positive and negative market values of derivatives. The net exposure was DKK84.8bn (€11.4m), against DKK94bn at the end of 2015, and it was mostly secured through collateral management agreements, according to the bank.

SEB, with 109 structured products (2015: 126 products), was the third most active issuer in the Swedish market in 2016. However, the bank saw its sales drop by almost 70%, from SEK2.8bn in 2015 to SEK904m last year. SEBs products, which were distributed via Erik Penser, Garantum, Länsförsäkringar Bank, Skandia and Strukturinvest, included 47 products linked to a basket of stocks; 32 linked to a single index; 21 to credit; five to a hybrid basket; two to a basket of indices; and one each to a fund and a single stock.

SEB reported an operating income of SEK43.3bn (2015: SEK44.7bn) for the full year 2016. Operating expenses stood at SEK21.8bn, level from 2015, while the operating profit, at SEK20.3bn was slightly down on the prior year (SEK21.8bn).

For the fourth quarter the effect from structured products offered to the public was approximately SEK535m (Q3 2016: SEK510m, Q4 2015: SEK445m) in equity related derivatives and a corresponding effect in debt securities and related derivatives SEK-355m (Q3 2016: SEK-390m, Q4 2015: -SEK460m), according to the bank.

Click the link to view the full year 2016 results for Danske Bank, Handelsbanken, Nordea, SEB and Swedbank.

Related stories:

Sweden Market Review - January 2017

Swedish structured products sales falter in 9M2016

CLNs double market share in Sweden