ABN Amro has reported a net profit of €688m and a return on equity (ROE) of 13.5% for the second quarter of 2018, as the Dutch economy continued to flourish, according to the bank.

The bank announced plans to reduce the cost base of corporate & institutional banking (CIB) by €80m, reflecting a staff reduction of around 250 full-time employees. The ROE of the division, which covers loan products (structured finance and trade & commodity finance), flow products (global markets) and specialised products (clearing and private equity), does not meet the group ROE target, as income growth in certain activities has not offset risk-weighted assets growth, impairments and costs, according to Kees van Dijkhuizen (pictured), CEO.

'To improve profitability of CIB to deliver on our target, capital allocated to global sectors (mainly trade and commodity finance) and to highly cyclical sectors with high earnings volatility will be reduced,' said Dijkhuizen during the presentation of the bank's second quarter 2017 results.

There are 2,462 structured products (excluding leverage and flow) issued by ABN Amro listed across 11 SRP databases. Of these, only six products are still live, including five notes linked to the swap rate in the Netherlands and a Libor linked note in the US. Another 10 live products were offered by the bank in various jurisdictions of which NOC Juillet 2026, an eight-year autocallable linked to the Eurostoxx 50 - distributed by ABN Amro Private Banking France and issued via Goldman Sachs - is the most recent (strike date July 13, 2018).

The provision for project costs relating to interest rate swaps sold to small and medium-sized enterprises (SMEs) was raised by €37m in the second quarter of 2018. (2Q17 included a €54m addition to the provision for project costs and a €15m increase in the existing compensation provision).

In 2015, ABN Amro started a review at the request of both the Netherlands Authority for the Financial Markets (AFM) and the Dutch Ministry of Finance, to determine whether the bank had acted in accordance with its duty of care obligations with respect to the sale of interest rate derivatives to SME clients, as a result of which, eventually, ABN Amro started the reassessment of around 6,800 clients with some 9,000 interest rate derivatives in the first quarter of 2017. Later, the reassessment was slightly expanded, so that on May 31, 2018 the reassessment consisted of 7,079 clients with 10,638 interest rate derivatives.

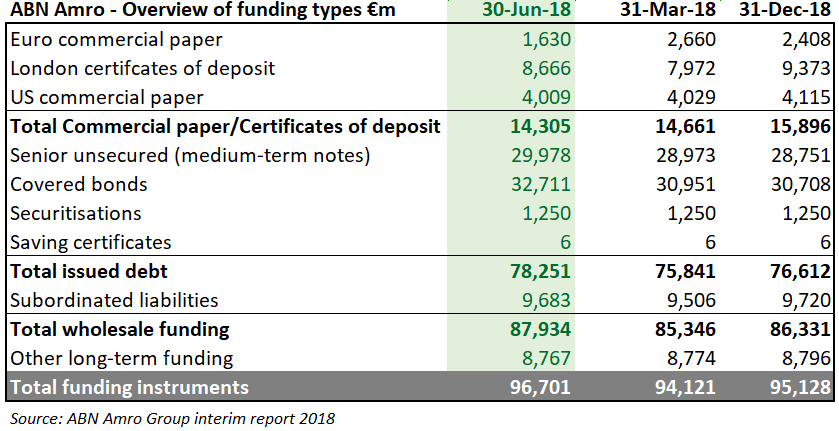

Issued debt securities went up by €2.4 billion quarter-on-quarter, totalling €78.3 billion due to a higher USD rate and increased long term funding, while the total wholesale funding (defined as issued debt plus subordinated liabilities) increased to €87.9 billion at June 30, 2018 (March 31, 2018: €85.3 billion), according to the bank.

The outstanding for senior unsecured medium-term notes stood at €29.9 billion as of June 30, up from €28.9 billion end-March. Long-term funding raised in 2Q18 amounted to €2.9 billion and consisted of €1.6 billion in covered bonds with long maturities, a green senior unsecured bond of €0.8 billion and a €0.5 billion senior unsecured GBP-denominated bond. The change for the period in fair value of the structured notes attributable to a change in credit risk amounted to a loss of €14m in the first half of 2018 (full-year 2017: €15m).

ABN Amro was re-established in 2009 in its current form, following the acquisition and break-up of the original ABN by a banking consortium led by Royal Bank of Scotland (RBS), which took on the bank's structured products book. In 2014, following a review of its markets division, which was selling structured products to clients worldwide, the bank decided it would stop selling its own structured products.

Click the link to view the full ABN Amro interim & quarterly report.

Related stories:

Natixis delivers solid half-year performance despite low equity derivatives activity in Asia

Societe Generale reports good level of structured products revenues despite lower demand

BNP Paribas reports YoY decrease in CIB revenues despite recovery in equity derivatives