Following the release of an investor update by UBS Global Wealth Management, announcing that volatility has returned to financial markets after an abnormally calm 2017, SRP spoke to Maximilian Kunkel (pictured), strategist at UBS Global Wealth Management's Chief Investment Office (CIO), about how investors can manage their risks by diversifying their portfolios beyond classic equity and bond indices aligning their portfolios with their financial goals, and risk appetite, while retaining exposure to equity market upside and offsetting this with some downside protection as well.

The main conclusion of the research report is that we live in a world of above-trend growth but with the return of more normal levels of volatility. In this environment, it is important for investors to look at the fundamentals but also to look for alternatives, including those that may not have been in focus over the last few years, characterised by the aforementioned above-trend growth coupled with very strong momentum and expanding monetary policy, according to Kunkel.

"What we are seeing is that many investors still rely too much on passive approaches in traditional markets," said Kunkel, adding that in many cases they are not managing equity downside risks appropriately, are too focused on higher yields while underestimating risks, particularly credit risk, and many have concentrated assets in familiar regions or industries, and their investments are not sufficiently long-term.

"We think that to address these issues investors need to start diversifying beyond classic equity and bond indices. If you look at the last few months, volatility levels and monetary policy have started to normalise so there is scope to use smart beta strategies, options strategies (buy-write) that are applied in a more systematic way, and the implementation of barrier reverse convertible (BRC) strategies."

The Swiss bank is also putting an emphasis on global diversification across sectors and countries as demand from investors increases. "Over the last few years, the focus for diversification has been the US, mainly because of fundamentals such as positive interest rates and stable inflation figures," said Kunkel. "However, since currently the whole world is experiencing growth, market valuations in other regions have become more appealing relative to cash and fixed income. This has resulted in increasing demand for allocations in other markets, such as Asia and Europe."

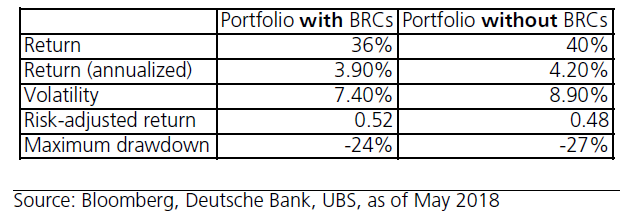

BRCs and put options

The UBS research points that barrier reverse convertibles (BRCs) can be useful in times of higher volatility since they can provide investors with greater "predictability" of returns. During periods of higher volatility, available yields and coupon rates on BRCs can improve, since implied volatility increases, while rising interest rates can also increase the coupon since investors require higher compensation for funding the issuer.

However, BRCs may not be suitable for investors looking to protect against large drawdowns (such as those seen during the 2008-09 financial crisis), although they can still deliver positive returns when underlying assets suffer smaller drawdowns.

"BRCs limit upside potential in return for a degree of downside protection," said Kunkel, noting that in the context of roaring bull markets over the last two years, a consistent and systematic application of these products could have limited upside potential quite significantly. "However, in the current context of investors' more muted long-term return expectations and more normal levels of volatility, a systematic introduction of BRCs to complement long-only exposure becomes more attractive. BRCs can provide stable returns whilst protecting investors against the short-term bouts of volatility."

The Swiss bank has developed a three-step BRC methodology for investors to identify which underlying stocks are suitable for these products. "First, we take the research provided by UBS single stock analysts which cover more than 2,000 stocks globally, and we only take buy-rated stocks," said Kunkel. "Second, we use a three-factor model to screen if a stock is statistically likely to touch a specified barrier: Altman-Z, modified Merton distance-to-default, cash-ratio. By removing 25% of the most "risky" stocks, we aim to reduce the probability of a barrier-event by 50%. Finally, we use our volatility screen to enhance returns compared to selling volatility randomly."

Another method of buying downside protection is to buy put options. According to the report, the price of insurance, as measured by the VIX index of implied equity market volatility, is currently running below its long-term median, so protection is relatively cheap. Investors can also further reduce the cost of hedging by taking out insurance on only part of their portfolio, or by choosing a strike price of around 10% out of the money, according to the report.

Since it is hard to predict when tail risks might push the market into correction territory, UBS is making a strong case for choosing relatively long-duration put options - around 12 months because although 'these are more expensive than shorter-duration options, they provide more lasting protection'.

Systematic hedging

For investors who want to maintain a diversified long only equity exposure, UBS recommends using a systematic hedging approach in order to lower the volatility of a portfolio, and improve the cost and effectiveness of hedging.

At present, UBS believes the best "bang for your buck" in terms of downside protection comes from three-month, 25 delta, put options on the Eurostoxx 50 index, the FTSE MIB (Italy) Index, and the Hang Seng China Enterprises Index.

"Most investors tend to buy insurance when it is already too late, typically when volatility has already picked up," said Kunkel. "Investors who focus on a more systematic approach often rely too much on a single market (such as the S&P 500), even at times when protection is expensive."

Kunkel believes that hedging a portfolio systematically to ensure that losses are reduced during a market sell-off need not entail an unacceptable drag on performance.

"Our systematic hedging methodology follows a three-step process," Kunkel said. "First, we avoid common hedging mistakes by selecting hedges from a broad universe of 18 different equity indices. Second, we seek out those indices that exhibit volatile and correlated drawdowns during market sell-offs. Third, our unemotional selection methodology systematically buys protection when it is "cheap" - we don't wait for a market sell-off. Each month, we purchase three-months put options, all at a delta of 25 for the three markets with the highest "bang-for-buck" score according to our methodology."

Low volatility in the past incentivised investors to take more concentrated risk, according to Kunkel. "Now is the time to diversify and make use of more normal levels of volatility," he said.

Related stories:

UBS eyes BRCs and buy-write strategies to navigate high vol environment

We want to provide an institutional quality and set of solutions to private clients, UBS

UBS and Solactive kickstart sustainable partnership via high-grade development bank debt series