The best-selling product globally during September was sold in Japan by Mizuho Securities and raised a whopping JPY22.95bn (US$204m), in a market where the average ticket size is $14.7m, making up more than 25% of Mizuho Securities' $747m of sales this year. The five-year product (デジタル債/Digital TRY/JPY) is the ninth best seller in the Asia-Pacific region, and the sixth best seller and the most successful foreign exchange-linked product in Japan this year.

The income product is linked to the performance of Turkish lira against the Japanese yen and offers a fixed coupon of 8.45% pa for the first quarter and the same quarterly coupon if the lira/yen exchange rate is at or above the initial price on any valuation date; otherwise the coupon will be 0.1% per annum. The product is subject to early redemption if the exchange rate is at or above its initial level on the first two quarterly valuation dates and, thereafter, the early redemption level would drop semi-annually, in which case it offers 100% capital return together with a coupon.

At maturity, if the final spot rate rises above the valuation rate, it will offer the full return of capital in yen. Otherwise, it will return the initial capital less the fall of final spot rate with reference to its initial spot rate, also in yen.

Since late 2015, there has been a sharp decrease in the issuance and distribution of structured products in Japan. Partly due to the financial crisis in China, the dynamics among active distributors has changed rapidly with the bigger players in Japan losing market share.

FX rates have long been popular in the Japan market with assets linked to the asset class doubling in 2017 compared to 2016 (up from 8% to 16%), although the number of new issues remains the same, claiming an 8% market share. SRP data shows that 61 currency-linked products have been offered in Japan this year (up from 53 in the same period of 2016), raising US$1.79bn (up from US$761m in 2016).

The biggest local distributors by number of issues are Okasan Securities, Tokai Tokyo Securities and SBI Securities, while many of the bond providers in Japan are Scandinavian banks, including Kommunalbanken, Kommunekredit and Kommuninvest i Sverige. For this product, Mizuho partnered with HSBC as the derivative counterparty and Kommunalbanken as the bond provider, taking its bond issuing market share globally up 21.46% compared to the same period of 2016.

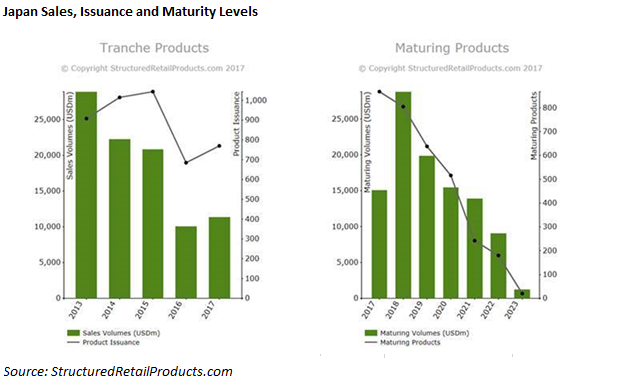

The Japanese structured products market is recovering after a large fall in 2016, when sales were half those of 2015. Considering the low level of maturities in the Japanese market and limited rollover opportunities, the higher sales volumes this year suggest a healthy uptake. Next year will see twice as much rollover cash ($28.8m) released into the Japanese market, according to SRP data.