The credit derivative market is a very standardised market with lots of chains and transactions, which, if there is a credit event, all tend to trigger at the same time, according to Simon Firth (pictured), derivatives and structured products partner at Linklaters.

"A party receiving a notice will need to serve its own notices on back-to-back transactions in a short timeframe," said Firth. "If you don't have any information about whether there has been a credit event, all you have is the notice and that is not a very satisfactory situation. Fundamentally, the credit derivatives market is a public market which depends on the information being generally available, so the whole market can do the same thing at the same time."

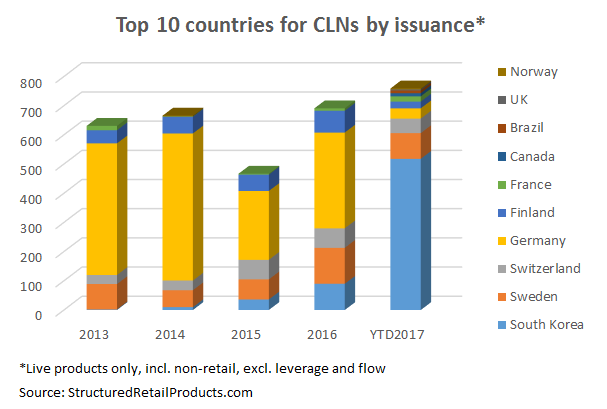

The SRP database lists more than 4,000 credit-linked notes (CLNs) including 780 products which have been issued this year. CLNs are products linked to the risk of default (credit risk) from a single entity, a basket of companies or reference entities contained in an index, for example the Market iTraxx Europe Crossover. In general, CLNs provide annual income, however, the size of the annual coupon and the return of capital at maturity depends on the number of credit events (if any) over the investment term.

Credit events are determined by the International Swaps and Derivatives Association (Isda) Credit Derivatives Determinations Committees (DCs), which each comprise 10 sell- and five buyside voting companies, alongside three consultative companies and central counterparty observer members. Their role is to apply the terms of market-standard credit derivatives contracts to specific cases, and make factual determinations on credit events, successor reference entities and other issues, based on information provided to the determinations committees by credit default swap (CDS) market participants.

"In terms of triggering a credit derivative, the traditional way, before the DCs were set up, was to serve a notice to each of your counterparties," said Firth. "You have to serve a credit event notice and a notice of publicly available information.

A credit event notice, according to Firth, is "an irrevocable notice that describes a credit event that occurred and contains a description in reasonable detail of the facts relevant to the determination that a credit event occurred".

At the same time, a notice of publicly available information has to be served, explained Firth. "This is a notice that cites publicly available information, so that's information obtained from the reference entity or has been published in various news sources, confirming the occurrence of a credit event, and a notice has to contain a copy or a description in reasonable detail of the relevant PAI," said Firth. "You don't have to have any information confirming that the grace period has been extended or the payment requirement; the amount of the default is above a certain level, so there are some exceptions," he said.

According to Firth, the issue is whether, for a notice of publicly available information to confirm the occurrence of the credit event, you have to confirm that each element of the relevant definition is satisfied. "You have to go through the definition and tick off all the requirements," he said.

"Alternatively, it is sufficient if the publicly available information confirms the relevant act that has occurred," said Firth. "There has been an extension of maturity, or there has been a payment default, without having to confirm what that extension or payment default has occurred in relation to."

The 780 CLNs with strike dates in 2017, which are worth an estimated US$6.5bn, were distributed across 15 jurisdictions, according to SRP data. South Korea, with 516 products from 16 different distributors, is the most active market. Sweden, with 88 products, is the main European market for CLNs, followed by Switzerland (50 products), Germany (36), Finland (23) and France (18). Stena and Korea Land & Housing Corp, seen in 33 and 30 products, respectively, were the most used single entities this year,while 33 products, including 17 in Sweden and nine in Finland were linked to the Markit iTraxx Europe Crossover index.

Related stories:

'Big bang' implementation of Apac OTC margin rules to stretch industry resources, Isda

Isda releases principles for US/EU trading platform recognition