Shinhan Investment created a series of products for investors equipped with a lizard feature to protect them against the downside that failed to find any buyers, primarily because the company chose to issue the three products denominated in Japanese yen, the first time the currency has been offered in South Korea since 2015.

All three products are linked to a combination of the most popular indices used in South Korea: the Kospi 200, Eurostoxx 50, Nikkei 225 as well as Hang Seng Index. The products also feature a relatively new type of autocall structure, called lizard, which has gained popularity over this year. The feature offers an extra layer of security to an equity-linked security (ELS) by including a second barrier that effectively provides a range in which that protection works.

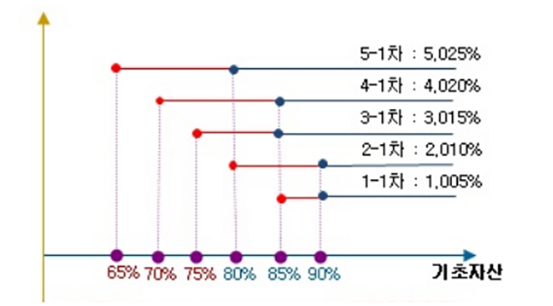

In Shinhan's three-year products, there are five knockouts available at each of the six-monthly observation dates with barriers at 90-90-85-85-80, while, at the same time, the added protection from the lizard comes in the form of barriers at 85-80-75-70-65 for the worst performing index for the two - ELS 14154 and ELS 14180. These also featured a rather low coupon of 2.01% pa compared to other Korean won-denominated equity-linked products issued by the same bank. The third of the products, the ELS 14158 also include a secondary knockout after the second observation date with a barrier of 70%. "Investors are expected to invest more in the early redemption products due to the increase in Kospi and Hong Kong indices", said an ELS-specialist in a Seoul-based bank.

The lizard condition was introduced to reduce the risk of loss of the ELS since this type of investment is known for its stability. After its introduction in 2016, the issuance of such products has increased to above 30%. This style ELS is considered to be safer, mid-to-low risk product that is safer than the traditional step-down and with higher yield than a principal-guaranteed ELS. According to a research by a local team, it can reduce average loss potential by about 75% over step-down ELSs.

The market has shown a distinct preference for riskier products, with 80% of the products issued this year including no capital protection. "I am not sure why people would really be interested in those notes, except if people have Japanese yen-denominated cash lying in their bank accounts and believe the yen will appreciate over the won," said a Seoul-based ELS specialist. While the yen may be a safe harbour for some, Korean investors chasing high returns at any cost were not interested in Shinhan's three yen-denominated products, which did not attract enough sales volume and were withdrawn.

While the yen is considered a safe-haven play and rallied even when Japan was a likely target as the North Korean tension escalated earlier this month, the won weakened to an almost four-week low on August 9, a day after ELS 14158 strike. While some analysts were certain that the flows in the yen were driven by tension on the Korean peninsula, others considered the moderate economic improvement and political troubles in the US as a more rational reason for the strengthening of the yen. Although central banks, including the US Federal Reserve and the European Central Bank, show signs of a retreat from monetary easing, the Bank of Japan plans to 'continue to steadily pursue powerful monetary easing under QQE and Yield Curve Control', according to Yukitoshi Funo, a member of the Policy Board at a meeting with business leaders in Sapporo.

Lizard feature

Source: Shinhan Investment

Relates stories:

Asian-in feature mitigates wrong way vote in UK referendum

Deutsche Bank clients cash in as memory coupons snowball

Product snapshot: Absa's risk lenses focus on risk premia