Ten months ago, in August 2016, Bufferfund, an open-ended investment fund which invests in capped bonus certificates linked to the Eurostoxx 50, was launched in the Netherlands. Since the launch, the fund has yet to register a negative monthly performance while the size of the fund has increased by €9m to €25m.

SRP looked back on those first ten months with fund manager Marcel Tak (pictured), and spoke to him about the funds objectives, the market volatility, his experiences managing the fund, and his expectations for the months ahead.

"If you look at the size of the fund that's something we are certainly very happy with, especially because we haven't even started with a marketing campaign yet," says Tak. "We want to put down a track record first, to perform as a fund, and ultimately, based on the performance, we want to make the public more aware of the fund," says Tak who sees plenty of interest in the fund from investors. "We get a lot of calls from potential investors and based on the information we provide many are willing to participate. Hence the increase to €25m. I think you can safely say that we have already become a medium-sized fund."

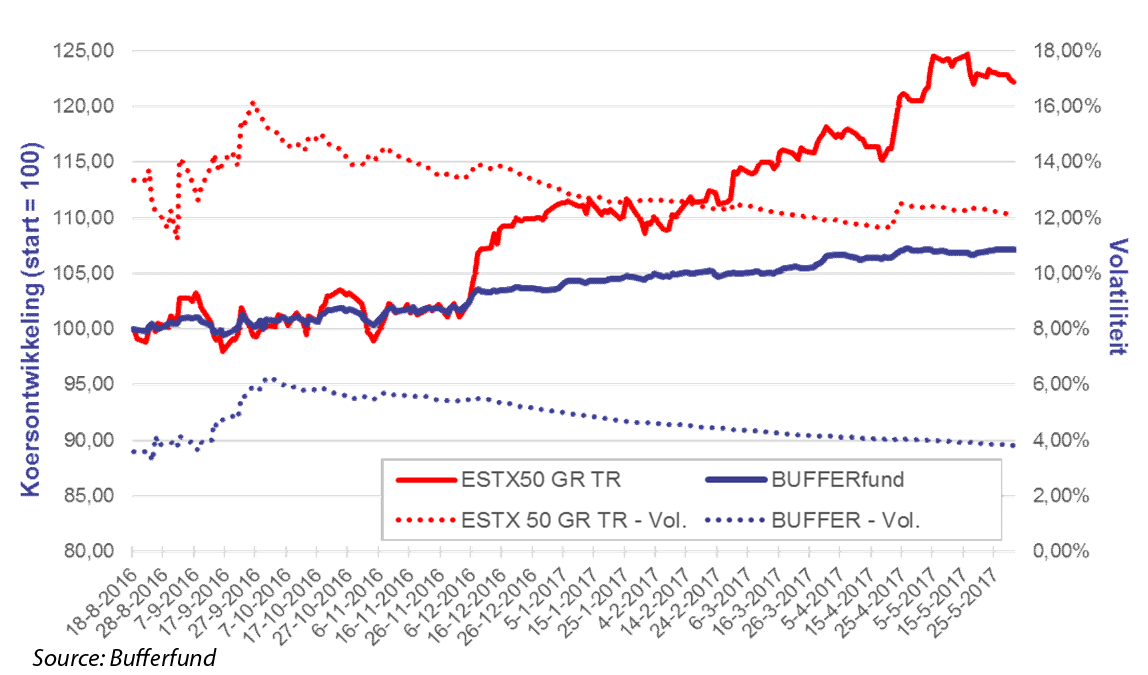

The performance of the fund since the start is 7.13% (3.54% in 2017) and every single monthly performance thus far has been positive. "Last month, at 0.06%, it was close, and we just managed, but indeed, until now we have had a positive score every month," says Tak. "What we really want is to achieve a smooth progression of the price and the return. That means in general that when the financial markets are rising, especially in fast growing markets, we will be somewhat behind the benchmark, the Eurostoxx 50," he says. "On the other hand, it is also true that when the markets are declining strongly, the fund should perform better, but of course we have not been able to test that in practice because the markets have been fairly stable until now."

The objective of the fund, in the longer term (three to five-years), is to perform just as good, if not better, than the benchmark, but with a much smoother progression, which, according to Tak, translates especially into volatility. "At the moment, you can see that the volatility of our fund, at 3.8% (as of May 31) is very low while at the same time the volatility of the Eurostoxx 50 is 12.1%," says Tak. "When it comes to yield, we are behind the index, however, we won't go all out to keep up with the index because our first priority is to minimise the risk. We want to make sure that when the markets become restless and are about to decrease that we keep the damage as limited as possible."

The fact that we are now in a period of very low volatility is not the most favourable situation for Bufferfund because it trades in capped bonus certificates for which typically the rule applies the higher the volatility the higher the return, according to Tak. "Back in August last year, the return on a bonus certificate with a 20% buffer would be around 11 to 12%. Now you can only achieve a return of between 7.5 and 8% on a product with the same 20% buffer," says Tak. "Of course, this is still quite a good return, but it does mean that if you take full positions in those bonus certificates, bearing in mind the current low volatility, and the markets would suddenly go down the volatility would increase, which would mean that the fund would be hit extra hard because the price of those bonus certificates would go down fast."

One of the reasons why in a rising market the fund is somewhat behind the index and in a falling market manages to keep the losses limited, is that the managers also use reverse capped bonus certificates, according to Tak. "Those certificates do exactly the opposite from what the regular capped bonus certificates do. They perform well if the market is stable or decreasing, but if the market is going up their performance is not so good," he says. "They are kind of short positions. We buy these certificates to keep the fund's performance as stable as possible."

Due to the low volatility and the fact that the fund managers want to control the risk, Bufferfund is not fully invested at the moment. "We are invested for two thirds and keep one third as liquidity. That's purely to ensure that when markets go down and the volatility increases we don't go down to fast too," says Tak.

Most people who invest in Bufferfund are not really familiar with structured products, according to Tak. "They are more interested in the fact that we have a policy to ensure that in bad circumstances we try to limit the damage and in case there is damage we can quickly recover via the bonus certificates without the markets having to recover themselves because you constantly work with premiums you are trying to collect," says Tak. "People are more interested in our goal of long term risk management then in the short term return we are trying to achieve."

Tak acknowledges it is difficult to predict how the fund will perform in the coming months. "With regards to the fund we always say that we do not have a vision. We do not take in positions based on the fact that we think the markets go up or down. Our only vision is the volatility," he says. "If the volatility is low and because of the low volatility we would suffer too much damage if the markets were to decline, we would take a relatively large position in liquidity, but that is not based on a vision."

According to Tak, "that's pure because 'when' the markets go down we want to make sure that the damage is not too big, but 'if' the markets go down we don't know".

"It wouldn't surprise me, but that's my personal vision, if at a certain moment there will be a break out, either up or down, and that the markets will start to move," says Tak who admits that the current situation is somehow unnatural. "The interest rates are very low, there are no alternatives for investors, shares are still being bought but valuations are quite high already and would of course become even higher, relatively, if the interest rates were about to go up," he says. "Essentially, a hike in the interest rates is needed to make the market realise that equities are expensive, but just the thought alone of a possible rise in the interest rates could lead to a serious reaction."

Tak expects to see "some serious movements" in the coming months. "However, there are many gurus in the market, each and every one with their own ideas, but the market is doing its own thing anyway," says Tak. "We have chosen to react what the market is doing and we are not going to predict what we think the market will do."

Click the link to view the latest factsheet.

Related stories:

The Netherlands Market Review - April 2017

SRP 3-minute Q&A: Marcel Tak, IFA, publicist, fund manager

Commerzbank continues product expansion in the Netherlands

Structured products can be very interesting but not many investors know how to deal with them