Lloyds TSB Bank (which became Lloyds Banking Group following the HBOS merger) has agreed to redress thousands of customers who were mis-sold structured investments from 2000 onwards.

According to the Lloyds Trade Union (LTU), the bank sent out thousands of letters to customers last week saying that it had 'identified that we did not give you sufficient information to make an informed decision before you made your deposit.'

'We estimate that the total amount of compensation will be £66 million,' wrote Mark V Brown.

General Secretary of the LTU. 'In addition, Scottish Widows is also paying out £18 million to 3,500 customers who were mis-sold Protected Capital Solution Funds.'

The LTU expects that further product reviews will see more customers receiving compensation on the basis that the UK Financial Conduct Authority's (FCA) review only goes back to 2012 and not to 2000 when these products started to be sold to customers.

'We will be making this point to the FCA directly,' stated Brown. 'Equally, whilst many customers complained about the pressures they were put under to move their savings into these products, we will be making it clear to the FCA that individual members of staff should not be subjected to any disciplinary sanctions as a result of selling these products.'

Zak de Mariveles, chairman of the UK Structured Products Association (SPA) said that Lloyds are not a member of the association and is "unable to comment on their activity going back some 17 years".

"What is fact however is that, working closely with the FSA/FCA, the industry has been transformed over the last 10 years and shines as a beacon to other industries," said de Mariveles. "The UK structured products industry now leads the way with respect to regulatory issues such as product governance including analysis of product complexity and target market assessments, and furthermore UKSPA members sign up to a voluntary undertaking to observe specific standards with respect to the structuring, issuing, marketing and trading of structured products which are offered to individual investors in the UK."

According to Brown, the blame for the design, marketing and selling of these products 'rests squarely' with the bank's senior managers and ultimately the chief executive. Brown also said that the LTU will send a letter to the regulator 'asking what sanctions, if any, it is planning to take against these individuals'.

'A few years ago a number of staff in Commercial Banking were disciplined for selling similar products and many lost bonuses in spite of the fact the allegations against them were eventually thrown out,' stated Brown. 'Will the Bank/FCA seek to clawback bonuses from the senior individuals responsible for these 'dodgy' products?'

The LTU claims that the 'gullibility of customers and so-called asymmetry of information (where sellers know much more about the products than customers) will always be exploited in order to create profit opportunities' and 'so it was with structured financial products'.

According to the FCA Review, Lloyds' customers invested some £9bn in structured products sold by the bank while the LTU estimates that that up to £20bn of customers' savings have been invested in 'these fiendishly complicated products over the years'.

The FCA review (TR 15/2: Structured Products: Thematic Review of Product Development and Governance) included a number of products sold by Lloyds TSB Bank including Market Linked Deposit (MLD), Offshore Limited Deposit (OLED), Inflation Rate Bond (IRB), Capital Protected Fund (CPF), Protected Capital Solutions Fund (PCSF) and Guaranteed Investment Bond (GIB).

The LTU points that in respect of one Market Linked Product, called 'Acorn', which was sold by Lloyds TSB between 2008 and 2010, the UK regulator concluded the information provided to customers 'was in breach of the principle of providing fair, clear and not misleading promotions, because it provides the consumer with a misleading impression of the likely return'.

'.....we believe a typical customer expected the product to provide a return of up to 42% if the market rose,' stated the FCA. 'We have had a customer complain that the market did rise during this period, but they received a return of 0%, contrary to their understanding from the marketing literature'.

The structured products industry has made its position clear since the FCA review was released in early 2015 pointing that structured products are manufactured to deliver a return based on a certain market scenario and that to compare risk-free and risk-bearing products 'is comparing apples and pears'. The industry also responded to the UK regulator highlighting the fact that many of the findings and issues raised by FCA in Retail Product Development and Governance - Structured Product Review FG12-09 and TR15/2 are not unique to structured products but apply equally to other types of retail investment products.

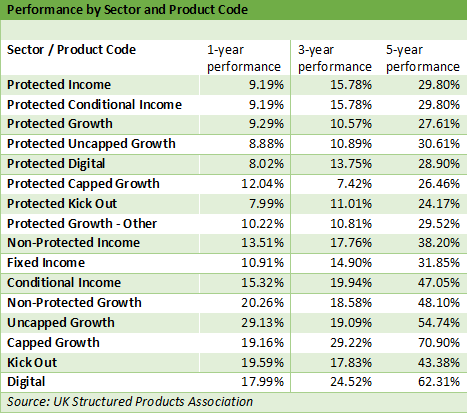

Market data shows that structured products continue to be 'consistent performers for many years' and continue to deliver positive returns to investors (see UK SPA monthly performance data for the month of April) .

According to a Lowes Financial Management (LFM) report, in the first quarter of this year, 174 structured products matured of which 161 delivered a gain for investors, six returned capital only and seven made a loss. The average annualised return of all the 174 products maturing in the first quarter was 6.71% over an average term of three and a half years. The top 25% made average annualised gains of 11.20% over an average term of two and a half years, while the bottom 25% made average annualised gains of 1.09% over an average term of five years and two months.

In addition, LFM reported earlier this year that almost all UK intermediary distributed products (89%) maturing in 2016 generated positive returns for investors, with 8.9% returning capital only and 2.1% (nine products) delivering a loss to investors' original capital.

Lloyds is the latest UK bank to make provisions to compensate investors in structured products.

The Royal Bank of Scotland (RBS) put aside £249m in 2016 to cover compensation payments for investment advice and mis-selling of structured deposit investments to retail investors. RBS marketed over 90 tranches of the Autopilot range in the UK market, of which 45 structures are still live, according to SRP data.

Lloyds has marketed over 460 structured products in the UK market since 1996 of which 10 are still live. The future of the bank's structured products business was questioned in 2014 after a year of marginal activity in the UK market. The bank has not marketed any products in the UK retail market since 2013.

A llloyds spokesperson said that Lloyds had recognised"that with some of our historic structured investment products we did not provide a small number of our customers with sufficient information before making their deposits.

"We apologise for these errors, which fall short of our aim to be the best bank for customers," said the Lloyds official. "We are proactively writing to all these customers to explain their options and will ensure that customers do not suffer any financial loss."

Calls to the FCA requesting comment were not returned by press time.

This update inlcudes a comment from a Lloyds spokesperson.

Related stories:

Majority of UK products maturing in 2016 deliver positive returns, funds stumble