Sales and issuance of structured products in the Nordics were dramatically down in the first quarter of 2017 compared to the same period in 2016 which, in itself, was by no means a vintage year for structured products in the region, according to SRP data. Sales volumes in Sweden, Finland and Norway decreased by 31%, 60% and 44%, respectively, with only Denmark, where sales increased by 5%, bucking the trend. Issuance was down in all four markets, with Finland, where the number of new products during the quarter was 50% down on 1Q16, especially hard hit.

SRP reviews the data and the financial results of the top five Nordic structured products manufacturers.

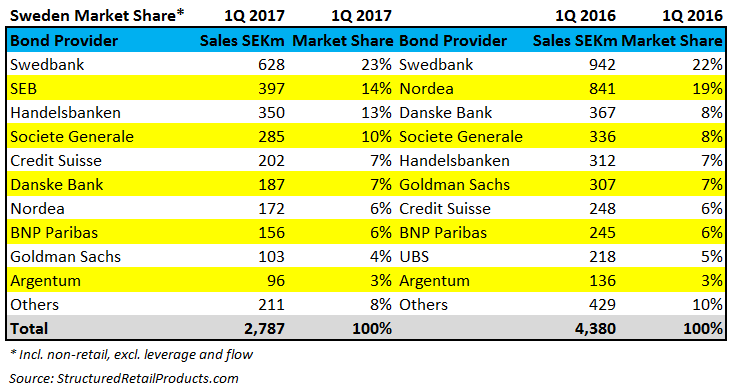

Swedbank restricted its structured products activity to Sweden, where it retained its position as the number one issuer, with a share of 23% of the market in the first quarter of 2017, according to SRP data. The bank sold 32 products worth SEK628m (€65m) between January 1 and March 31, 2017, down from 35 products with combined sales of SEK942m during the same period last year. The majority of Swedbank's products in the quarter were linked to equities (29), including 16 products linked to a share basket; 11 were linked to a single index; and three to an index basket. The remaining three products were linked to credit (two) and foreign exchange rates, respectively.

As at March 31, 2017, Swedbank had SEK975.9bn debt securities outstanding, including SEK15bn worth of structured retail bonds. The bank reported net commission income increased by 8% year-on-year to SEK1.7bn (against SEK1.6bn in teh first quarter of 2016). The increase was mainly due to higher asset management income and card commissions, which was partly offset by lower guarantee commissions and lower income from equity trading and structured products. Compared to the fourth quarter of 2016, net commission income rose by 17% to SEK580m (compared to SEK496m in the fourth quarter of 2016) due to increased income related to equities and bond issues, increased loan commitment commissions and lower sales commissions for structured products to Swedish banking and the savings banks.

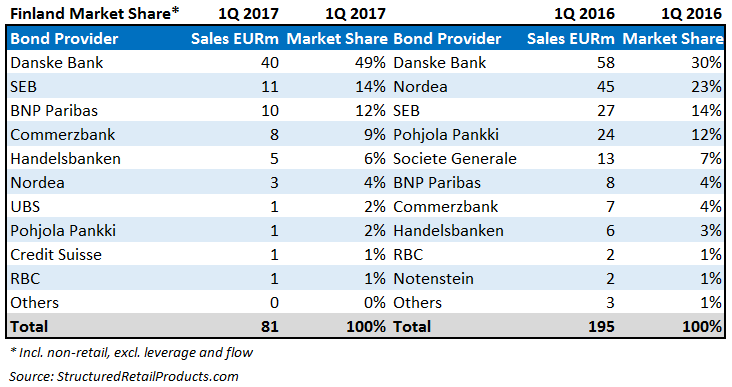

SEB was the second most active issuer - both in Sweden and Finland - during the first quarter 2017, although it refrained from issuing structured products in Denmark and Norway. In Sweden, the bank issued 20 structured products worth SEK397m (compared to 13 products and SEK89m in the first quarter of 2016), with the distributors including Erik Penser, Garantum, Skandia and Strukturinvest. In Finland, SEB sold six products via Alexandria and SP Kapitaali, which sold €11m over the quarter (against 15 products and €27m in the first quarter of 2016).

For the first quarter, the effect from structured products offered to the public was approximately SEK575m (compared to SEK535m in the fourth quarter and SEK-565m in the first quarter of 2016) in equity-linked derivatives with a corresponding effect on debt-related derivatives of minus SEK450m (against minus SEK355m in the fourth quarter and SEK560m in the first quarter of 2016), according to the bank.

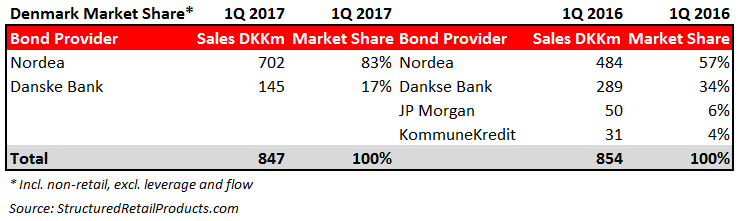

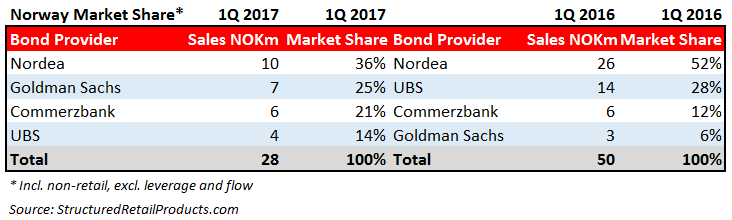

Nordea was the only provider active in all four Nordic markets. Year-on-year sales volumes took a hit, especially in Sweden and Finland, where sales fell by 80% and 93%, respectively, according to SRP data. Denmark, where the bank sold three structured products worth DKK702m (€93m) during the first quarter (against five products and DKK484m in the same quarter of 2016) was the only country providing a positive result for Nordea, while, in Norway, the bank remained top of the bond provider table, despite a 16% decrease in market share.

Nordea reported total assets on its balance sheet had increased by €34bn over the quarter and the asset values of derivatives were €14bn lower than in the previous period. The bank issued approximately €4.2bn in long-term funding in the first quarter, excluding covered bonds in Denmark, and subordinated notes, of which €3.2bn represented the issuance of Finnish, Swedish and Norwegian covered bonds in domestic and international markets. Nordea's long-term funding portion of total funding was 81% at the end of the fourth quarter.

'The low-intensive growth continued in the beginning of 2017, although we are now seeing good potential for a synchronised recovery with improving growth prospects,' said Casper von Koskull (pictured), president and group chief executive officer of Nordea, in a statement. 'Inflation is under control, and we are prepared for low rates for a long time.'

Handelsbanken was only active in Sweden and Finland during the first quarter. In Sweden, the bank issued 23 products worth SEK350m, which translated in a 13% share of the market (against 13 products and SEK312m in the first quarter of 2016), while, in Finland, year-on-year sales remained fairly stable, with €5m collected from four products (compared to two products and €6m in the first quarter of last year).

Handelsbanken reported total fund volume, including exchange-traded funds, increased by 5.6% from the beginning of the year to SEK449bn. Total assets under management in the group rose during the same period by 4.8% to SEK568bn. The bank's operating profit rose by 8% to SEK5.3bn (compared to SEK4.9bn in the first quarter of last year) while return on equity for total operations declined to 12.4%.

Danske Bank issued structured products in Denmark, its domestic market, and in Finland and Sweden. In Finland, the bank was the main provider of structured products in the first quarter, acquiring a 49% share of the market from 14 products (€40m), while, in Sweden, Danske had a 7% market share, also from 14 products (SEK187m). In Denmark, despite ranking behind Nordea, Danske's market share plummeted by 50% after selling just four structured products (DKK145m) in the first quarter.

Danske reported credit exposure from trading and investment activities amounted to DKK801bn at March 31, 2017, against DKK854bn at December 31, 2016. The bank made netting agreements with many of its counterparties concerning positive and negative market values of derivatives. The net exposure was DKK72.9bn, against DKK84.8bn at the end of 2016, and it was mostly secured through collateral management agreements, according to the bank.

Click the link to view the full first quarter results for Danske Bank, Handelsbanken, Nordea, SEB and Swedbank.

Related stories:

Danske Bank global head departs amid reorganisation

Structured products are moving out of an unruly adolescence into adulthood, Garantum

Finnish watchdog fines four firms for suitability failures

Norway's ETN market takes off, European sectoral indices in focus