Before the dotcom bubble burst, initial public offerings (IPO) were a daily event, with 371 in 1999, but only 20 in the US in 2016. But now there is Snap, an American multinational technology and social media company, known by the image messaging application Snapchat, which raised $3.4bn by selling 200 million new shares on March 1.

Commerzbank was among the first structured products providers to capitalise on the interest from investors, issuing seven call warrants on March 6 in France and Portugal. "The upcoming IPO of Snap was all over the news [...] so we expected demand for structured products based on Snap," said Jose da Silva Pires, product manager, public distribution at Commerzbank.

ETPs provided a way to be invested without investing directly in the shares, according to Da Silva Pires. But structured product providers face obstacles when issuing warrants based on IPO stocks, such as the lack of historical prices, liquidity and listed options. "At the beginning, we are usually confronted with the problem of a missing repo market," said Da Silva Pires. "This fact makes it impossible for us to hedge our corresponding risk", which makes it impossible to issue put warrants.

Besides that, with no listed options or historical volatility pricing, these underlyings are difficult. "We have to assume where the implied volatility is or will be and how the curve looks," said Da Silva Pires. To get the best possible approach, most investment banks look for underlyings on similar shares and estimate an expected correlation, according to Da Silva Pires.

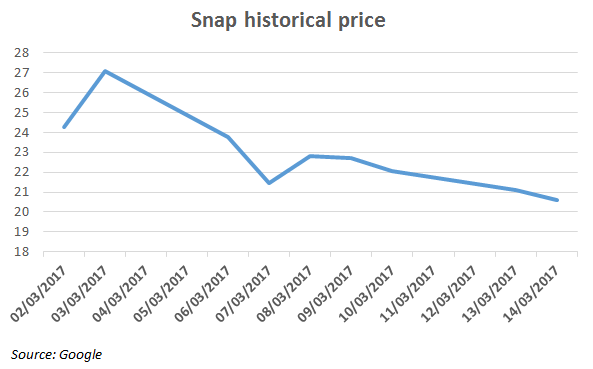

The stock, which was 12 times subscribed during the IPO, has dropped by 15% from its isue price since the listing on March 2, although the shares of similar companies, such as Facebook - which hit an all-time highs last week - only stabilised well after their IPOs.

Demand in the flow and leveraged market "always depends on how popular" the underlying is and the amount of media coverage, according Da Silva Pires.

Related stories:

Wedding cakes are perfect, Exane

Societe Generale moves to fill fixed income/interest rates gap in Germany

BMO racks up $310m with synthetic-linked structure in USA