Luzerner Kantonalbank (LUKB) is planning to set up a competence center for the development and issuance of structured products by the beginning of 2018. The Swiss bank is seeking to expand its earnings base further, and will mainly serve as a supplier to other banks and asset managers.

A LUKB spokesperson said it is really "too early" at this stage to give substantial answers around the initial offering and set up. "During the next weeks, we will initiate the project for building the new unit in order to have it operational in the beginning of 2018," said the LUKB official. Once fully developed, the new "Kompetenzzentrum für strukturierte Produkte" will consist of about 10 persons. Geographically, it will be based in the location of our Private Banking Office in Zurich."

The move to build a competence center for the development and emission of structured products is part of the bank's "2020 @ LUKB" strategy for the years 2016 to 2020. LUKB intends to start operation with the new division by 2018.

"We want to reduce our reliance on interest rates by rounding off our core business offer new products in the investment business," said LUKB's chief executive, Daniel Salzmann (pictured). "With the issuance of structured products, we can also achieve growth in the commission income business and, in the long term, optimize our procurement of passive money."

In the future, LUKB intends to act primarily as a supplier to other banks and external asset managers with its self-issued structured products. LUKB already offers structured products from other issuers to institutional clients as well as to other LUKB customers, provided that they have the corresponding risk profile as investors.

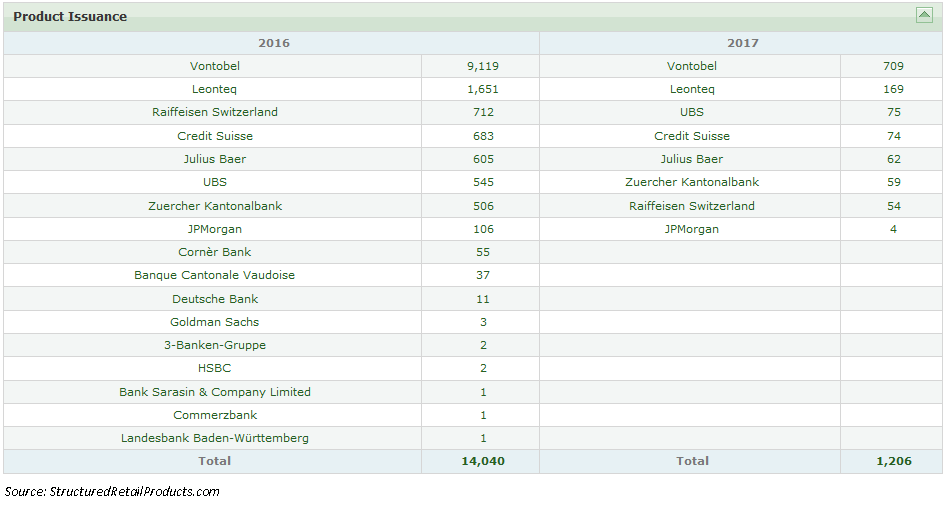

LUKB will become the 18 issuer of structured products in Switzerland in a market worth CHF20.3bn (€18.9bn).

LUKB's plans follow the latest report from the Swiss Structured Products Association (SSPA) which shows that in the fourth quarter of 2016, turnover of Swiss structured products reached CHF51.9bn. This means the value creation of the largest SSPA issuers fell by 5.9% relative to the previous year.

According to the trade body, demand for yield optimisation products remained strong, accounting for about 61% of the total. 45% of all products are based on equity products, followed by currencies at 43%. Fixed income increased by more than 109% relative to Q4 2015, boosting its relative share of the total to 10%. Unlisted products accounted for around 71% of output.

Year-on-year, total quarterly sales were 2% below the figure for the previous year of CHF231bn. In respect of the product groups, capital protection (+3%), yield enhancement (+3%) and leverage (+2%) recorded year-on-year gains, coming above all at the expense of participation (-7%). From an asset class perspective, there was a shift from equities (-6%) to currencies (+3%), while fixed income also doubled from 4% in 2015 to 8% in 2016.

The SSPA also reported total quarterly sales stood at CHF53.7bn, 5.9% below the figure for Q4 2015, and that there were shifts compared to the previous year in product groups as a percentage of the total: yield-optimisation products accounted for the lion's share at 61%, followed by leverage products (16%). Despite a relative year-on-year decline of 31%, participation products formed the third largest category with a share of 13%.

Also, compared to the previous year, capital protection products recorded relative growth of 89%, corresponding to a rise of 86% relative to Q3 2016. Equities and foreign currencies remain the most frequently used underlying assets. Equities now account for the largest share of asset classes at 45%, whereby the respective figure for the previous year was 47%. Relative to the previous year, the ratio of currency products fell from 43% to 40%. Fixed income increased by more than 109% relative to Q4 2015, boosting its relative share of the total to 10%.

Unlisted products accounted for 71%, representing a large majority of Swiss structured products which corresponds to a 1% decline relative to Q4 2015.

According to the SSPA, around two-thirds of sales (65%) are generated on the primary market, while transactions are once again almost exclusively executed on the secondary market (nearly 96%). CHF, EUR and USD were the main currencies in the market, comprising 85% of sales. Following a modest rise relative to the previous year (34%), the USD is now the principal currency, accounting for 36%. In year-on-year terms, EUR and CHF declined to 33% and 16% respectively.

Related stories:

Switzerland Market Review - January 2017

Vontobel cashes in on European expansion, UBS reports best full-year results since 2008

Numerix increases footprint in Switzerland, TR rolls out compliance solution